Best Free Credit Building Apps in 2026: What They Do and What They Cost

Free is a word that gets used loosely in the credit app space. Some apps are genuinely free. Others are free to download but charge for the features that actually matter. And some apps that cost money deliver enough value that the fee is worth understanding before you dismiss them. This breakdown covers the best credit building apps available in 2026, what each one actually does, and what it actually costs so you can make a clear-eyed decision about which one fits your situation. 1. Credit Genius Credit Genius is the most feature-complete credit building app on this list. It combines rent reporting with backdating, an AI-powered credit assistant, gamified financial education through Credit Games, and real-time Experian credit monitoring. The rent reporting with backdating feature is the standout. Renters can submit up to 24 months of prior payment history to Experian at once, turning payments they have already made into immediate credit history. A 2021 TransUnion study found that rent reporters saw an average score increase of 60 points. For someone with a thin file, that kind of improvement can happen within 30 to 60 days of enrollment. The AI credit assistant analyzes your specific Experian file and tells you exactly which actions will move your score the most, making it more useful than generic credit tips. What it costs: Visit credit-genius.com for current pricing. Core features are accessible without a large upfront commitment. Best for: Renters, people building credit from scratch, and anyone who wants personalized guidance on what to do next. 2. Experian Experian’s app is free to download and includes your Experian FICO score, your full Experian credit report, and Experian Boost. Boost lets you add on-time utility, phone, and select streaming service payments to your Experian file, which can produce a small score improvement for people with thin files. The free tier is genuinely useful. A paid subscription adds three-bureau monitoring, more detailed score breakdowns, and identity theft protection features. What it costs: Free for core features. Paid plans start at around 24.99 per month for premium features. Best for: People who want their real FICO score and the ability to add utility payment history to their Experian file. 3. Credit Karma Credit Karma is completely free and gives you access to your TransUnion and Equifax VantageScores, alerts when something on your report changes, and personalized product recommendations. It does not directly build your credit but it is a useful monitoring tool and the product marketplace can help you find accounts that are appropriate for your current score level. Credit Karma makes money through referral fees when users sign up for recommended financial products, which is how it keeps the core product free. What it costs: Completely free. Best for: People who want free two-bureau monitoring alongside product recommendations. 4. CreditWise by Capital One CreditWise is free and open to anyone, not just Capital One customers. It provides your TransUnion VantageScore, dark web monitoring, and a credit simulator that lets you model how different financial decisions might affect your score before you make them. The simulator is particularly useful for planning credit moves in advance. What it costs: Completely free. Best for: People who want free monitoring with a credit simulator tool for planning ahead. 5. Self Self offers a credit builder loan where monthly payments go into a locked savings account and the payments are reported to all three credit bureaus. At the end of the term you receive the money back minus fees. It is not free but it is structured so that you are essentially saving money while building credit history. The timeline is slower than rent reporting, typically six to twelve months before meaningful score improvement, but the savings component means the fees are partially offset by the money you get back. What it costs: Monthly payments range from around 25 to 150 depending on the plan. Fees are deducted from your final payout. Best for: People with no credit history who want to build a payment record while saving money at the same time. 6. Kikoff Kikoff offers a small credit account specifically designed for people with no credit history. You get a limited credit line to make purchases in the Kikoff store and on-time payments are reported to major credit bureaus. It is one of the simplest entry points available for credit invisible consumers. The credit line is small and the Kikoff store is limited, but the purpose is credit building rather than actual shopping. It does that job at a low cost. What it costs: Around 5 per month for the credit account. Best for: People with no credit history at all who want the simplest possible starting point. 7. Cleo Cleo is an AI-powered financial assistant with budgeting tools, spending tracking, and a credit builder option. The conversational interface makes it less intimidating for younger users who find traditional financial apps off-putting. Credit building is one feature within a broader personal finance platform rather than the primary focus. What it costs: Free tier available. Cleo Plus, which includes the credit builder feature, is around 14.99 per month. Best for: Younger users who want budgeting and basic credit building in a conversational, low-pressure format. How to choose between them The right app depends on where you are starting from and what you need most. If you are a renter with months or years of on-time payments that have never been recognized by the credit system, Credit Genius and its backdating feature is the fastest path to meaningful score improvement. If you want to add utility payment history quickly and for free, Experian Boost is worth trying alongside whatever else you are doing. If you have no credit history and want the simplest possible entry point without a monthly commitment, Kikoff is a low-friction starting place. If you want to build credit while also saving money over time, Self’s credit builder loan structure makes the cost feel less like a fee and more like a savings plan.Most people

What Makes Credit Genius Different From Other Credit Apps

There are dozens of credit apps available in 2026. Most of them do a version of the same thing: they show you a score, track changes, and send you alerts when something on your report shifts. That is useful. But it is not the same as actually helping you improve your credit. Credit Genius was built around a different premise entirely. The question it tries to answer is not what is your credit score right now, but what can we do to move it. Here is what that looks like in practice and why it matters. Most credit apps are monitoring tools. Credit Genius is a building tool. The majority of credit apps on the market are designed around passive awareness. They pull your score from a bureau, display it, and notify you of changes. The assumption built into most of them is that you already have a credit file worth monitoring. Credit Genius starts from a different assumption: that a significant portion of people who need credit help are renters, immigrants, young adults, or people recovering from setbacks who need to build or rebuild their file, not just watch it. The product is designed to serve that need rather than assume it does not exist. Rent reporting with backdating This is the feature that sets Credit Genius most distinctly apart from almost every other credit app available. Over 44 million renter households in the United States make their largest monthly payment every single month without receiving any credit recognition for it. Mortgage payments are automatically reported to the credit bureaus. Rent payments are not, unless someone actively reports them. Credit Genius reports rent payments to Experian, the bureau most commonly used by lenders for credit decisions. But it goes further than simple reporting. The backdating feature allows users to submit up to 24 months of prior rent payment history at once rather than starting from zero on the day they enroll. A renter who has been paying on time for two years and enrolls in Credit Genius can potentially enter the credit system with two years of clean payment history already established. A 2021 TransUnion study found that rent reporters saw an average credit score increase of 60 points. For someone with a thin or nonexistent credit file, that is not an incremental improvement. It is a transformation. AI-powered credit guidance that is actually personalized Generic credit advice tells everyone the same things. Pay on time. Keep utilization low. Do not open too many accounts. That advice is correct but it is not useful for the person who needs to know which card to pay down first, or whether disputing a specific item is worth their time, or what single action would move their score the most right now. Credit Genius includes an AI credit assistant that reads your specific Experian file and surfaces the actions most likely to improve your score based on your individual situation. The guidance is not the same for every user. It is built around the actual content of your credit file, which means the recommendations are relevant, prioritized, and actionable rather than generic. This is the difference between being told to exercise more and being told that 20 minutes of walking three times a week would address your specific health concern more effectively than anything else you could do. The personalization is what makes the advice useful. Credit Games: financial education that actually sticks Financial literacy content has a retention problem. Most people read an article about credit utilization and forget it by the following week. The information was accurate. The delivery was not designed to make it memorable or actionable. Credit Genius addresses this through Credit Games, gamified financial education modules that apply the same psychological principles that make games compelling to content that genuinely matters. Progress tracking, rewards, streaks, and challenges are built around credit concepts so that users engage with the material repeatedly and retain it. Users who complete Credit Games modules are more likely to take the recommended actions in their credit file because they understand why those actions matter, not just that they should take them. Understanding drives behavior. Behavior drives scores. Real-time Experian monitoring Credit Genius monitors Experian specifically, rather than TransUnion or Equifax, because Experian is the bureau most commonly pulled by lenders when making credit decisions. When something changes on your Experian file, you find out immediately. This matters for two reasons. First, catching errors early means disputing them before they have time to cause significant damage. Second, if something fraudulent appears on your Experian file, you want to know about it before you discover it on a loan application. Real-time monitoring turns your credit file from something you check occasionally into something you are always aware of. Who Credit Genius was built for Credit Genius is designed for people who are actively trying to get somewhere with their credit rather than just keep an eye on where they are. That includes renters who have been building payment history through rent that the credit system has never recognized. It includes immigrants and new US residents building a credit profile from zero. It includes young adults who have never had a reason to open credit and now need to. It includes people who went through something financially difficult and are working to rebuild. For all of these groups, the standard credit monitoring app was never designed with them in mind. Credit Genius was. The bottom line The credit app market is crowded with tools that do essentially the same thing. Credit Genius is different not because it has a better interface or a cleaner design but because it is trying to solve a different problem. Not how do I show you your score, but how do we actually improve it.For the tens of millions of Americans whose credit does not reflect their actual financial behavior, that difference matters more than anything else on the feature list.

9 Best Credit Karma Alternatives in 2026

Credit Karma is the most downloaded credit app in the US. It is free, it is easy to use, and it gives you a score. But it is not the only option, and for a lot of people it is not the best one. Whether you are looking for more bureau coverage, actual credit-building features, better identity protection, or just something different, here are nine alternatives worth knowing about in 2026. 1. Credit Genius If Credit Karma’s biggest limitation for you is that it monitors your score but does not help you improve it, Credit Genius is the most direct alternative. Where Credit Karma shows you your TransUnion and Equifax scores, Credit Genius focuses on Experian, the bureau most commonly pulled by lenders, and goes several steps further. Rent reporting with backdating lets renters submit up to 24 months of prior payment history to Experian at once, with an average score increase of 60 points reported in a 2021 TransUnion study. An AI-powered credit assistant analyzes your specific file and tells you exactly which actions will move your score the most. Credit Games make financial education engaging rather than passive. And real-time Experian monitoring keeps you informed the moment anything changes on your file. For anyone actively trying to build or improve their credit rather than just track it, Credit Genius does something Credit Karma was not designed to do. Best for:Renters, people building credit from scratch, and anyone who wants to actively improve their score rather than just monitor it. 2. Experian Experian’s own app is a strong alternative for people who want direct access to the bureau most lenders actually check. The free tier includes your Experian FICO score, your full Experian credit report, and the Experian Boost feature that lets you add utility, phone, and select streaming payments to your Experian file. The paid tier adds three-bureau monitoring, more detailed FICO score breakdowns, and identity theft protection. For anyone who wants to go deep on Experian specifically, this is the most direct tool available. Best for:People who want their actual FICO score and direct access to their Experian file. 3. myFICO myFICO is the only app that gives you the specific FICO score versions lenders use for different products, including FICO Score 2, 4, and 5 for mortgages, FICO Auto Score 8 for car loans, and FICO Bankcard Score 8 for credit cards. Most free apps show you a VantageScore, which is not what lenders check. It is the most expensive option on this list but for someone about to apply for a mortgage or major loan, the investment in knowing exactly what the lender will see is often worth it. Best for:People preparing for a significant credit application who need to see the exact scores lenders will use. 4. CreditWise by Capital One CreditWise is completely free and available to anyone, not just Capital One customers. It provides your TransUnion VantageScore, dark web monitoring, and a credit simulator that lets you model how different financial decisions might affect your score before you make them. The simulator is genuinely useful. Want to know how paying off a card or opening a new account might affect your score? CreditWise lets you explore that before committing. Best for:People who want free monitoring with a useful credit simulator tool. 5. Aura Aura goes beyond credit monitoring into full digital security. It combines three-bureau credit monitoring with identity theft protection, dark web monitoring, antivirus software, a VPN, and up to one million dollars in identity theft insurance per adult. It is more expensive than most credit apps but it covers ground that credit-only apps do not. For someone who has been a victim of identity theft or wants comprehensive protection, Aura covers the full picture. Best for:People who want credit monitoring bundled with serious identity theft and digital security protection. 6. Credit Sesame Credit Sesame has been around since 2010 and offers free TransUnion credit score monitoring with basic insights and debt management tools. The free tier covers the essentials and a premium plan adds more bureau coverage and identity protection features. It is a simpler, cleaner experience than Credit Karma for users who just want a score check and basic alerts without a lot of additional noise. Best for:People who want straightforward, free TransUnion monitoring without the product marketplace. 7. Chime Credit Builder The Chime Credit Builder is not a monitoring app but a secured credit card with no annual fee and no minimum deposit. It reports to all three major bureaus and is designed specifically for people who want to build credit through everyday spending. You need a Chime checking account to use it. For someone who is less interested in tracking their score and more interested in building it through daily purchases, this is a strong option. Best for:People who want to build credit through spending without fees or a large deposit requirement. 8. Self Self offers a credit builder loan where monthly payments go into a locked savings account. The payments are reported to the credit bureaus and at the end of the term you receive the money back minus fees. It is a slower credit-building method than rent reporting but useful for establishing a payment record without taking on traditional revolving debt. Best for:People with no credit history who want to build a record through a structured savings product. 9. Cleo Cleo is an AI-powered financial assistant with a conversational interface, budgeting tools, spending tracking, and a credit builder option. It is designed for younger users who find traditional financial apps intimidating or boring. The credit building feature is one component of a broader personal finance tool rather than the primary focus. Best for:Young adults who want budgeting and financial guidance alongside basic credit building in a conversational format. How to choose the right one The best alternative to Credit Karma depends on what Credit Karma isn’t giving you: If you want to actively build your credit rather than just monitor it, Credit Genius is

What Apps Can Help Boost Your Credit Score the Fastest

There are several different types of apps designed to help you understand your credit. Most apps will give you information about your current credit. There are some apps, however, designed to help you improve your credit over time. The list below outlines ten apps designed to assist in improving your credit, as well as rank them according to how much they positively affect your credit file. 1. Credit Genius Credit Genius is the most direct credit-building app on this list because it adds new positive data to your credit file rather than just displaying what is already there. Rent reporting with backdating is the best feature of this app. Credit Genius submits your monthly rent payments to Experian, including up to 24 months of prior history you have already built. A 2021 TransUnion study found that rent reporters saw an average credit score increase of 60 points. The platform also includes an AI-powered credit assistant that analyzes your credit profile and suggests the best actions for your situation, real-time Experian monitoring, and Credit Games for financial education. Best for: renters, People with no credit, and individuals looking for a tool to guide them based on their unique financial circumstances rather than general recommendations. 2. Experian Experian’s app features something called “Experian Boost” which allows consumers to add on-time payments from utilities, mobile phones, and certain digital streaming services into their experian credit report. Although results aren’t instant, it is one of the faster methods available for those with limited credit history. No additional loans or debts need to be established. Additionally, consumers will get instant access to both their FICO score and complete Experian credit reports. These are the versions most often checked by lenders when making lending decisions. Best for: consumers seeking to add historical evidence of on-time payment history for utility and/or streaming subscriptions into their experian credit file immediately. 3. Self The Self Credit Builder Loan allows you to make a fixed monthly payment into a locked, interest-bearing savings account. The monthly deposits are reported to all three major credit bureaus. Once the term ends, the funds are returned to you minus any fees. This is typically a slower process than Rent Reporting; however it does allow individuals to establish a payment history while also developing their savings habits through regular monthly contributions. Best for: Individuals with little or no credit history that wish to begin establishing a credit repayment history by making monthly payments as part of a new savings habit. 4. myFICO The myFICO platform provides consumers with the actual FICO scores used by lenders, as well as the exact version of each score used for different types of lending such as mortgage, auto loan, etc. Rather than guessing which areas to improve, knowing the exact FICO version(s) lenders are using enables you to tailor all subsequent credit-improvement activities towards those aspects of your credit profile that matter most to the next lender you apply with. Best for: Consumers planning to apply for a mortgage, automobile financing or other type of major credit applications wishing to know exactly which FICO scoring models and/or versions will be reviewed by prospective lenders. 5. Credit Karma Credit Karma is the most popular credit reporting service in the U.S., and it offers users free credit monitoring and alerts from both Transunion and Equifax (with VantageScore). While Credit Karma can help monitor your account for errors and alert you to any items needing your review, it does not directly enhance your creditworthiness. Best for: Those looking for free credit monitoring/alerts along side their other methods of building/repairing credit. 6. CreditWise by Capital One The best part about CreditWise is that it’s not limited to people who have accounts at Capital One; anyone can use it. This service offers you your TransUnion VantageScore and a “credit simulator” which will let you test out how different choices may affect your credit score. It also includes dark web monitoring. What makes the credit simulator so helpful is that you have the chance to plan what moves you’re going to make before you actually make them. Best for: Anyone interested in testing the effects of possible financial moves on your credit rating prior to making those moves, as well as anyone looking for free three bureau monitoring of their TransUnion report. 7. Aura Aura is an overall digital safety solution with identity theft protection, credit monitoring through all three credit reporting agencies, antivirus software, and a Virtual Private Network (VPN). While this product doesn’t help improve your credit score per se, the fact that Aura monitors all three major credit reporting agencies, has up to $1 Million in Identity Theft Insurance coverage if someone steals your identity, and also includes other forms of identity protection technology, makes it probably the safest protection tool available today. Best for: People who are seeking identity theft protection that includes three-bureau credit monitoring. 8. Chime Credit Builder The Chime Credit Builder is a secured credit card that has no annual fee, and you don’t need to make an initial security deposit in order to get it. Activity is reported to all three major credit bureaus, so making regular purchases with this card helps you build credit. To apply for a Chime Credit Builder Card you have to first open a Chime Checking Account. Best for: Those who would like to use their daily spending habits to establish some form of credit history with no fees, and are unable to put down a large security deposit upfront. 9. Credit Sesame Credit Sesame allows users to view their TransUnion Credit Score at no cost along with basic analysis, as well as tools to assist them in managing their debt. With both tiers of the service (basic and premium) users can monitor their TransUnion Credit Score for free; however, the premium version of the service will include additional information from other credit bureaus, such as Equifax and Experian, and identity theft services. In addition to being used as a monitoring tool, Credit Sesame also provides tools to help individuals build

Is Credit Genius a Better Alternative to Credit Karma in 2026?

Credit Karma has many different ways that it can be used. It is also likely the most-downloaded personal finance application available in the United States. So, when asked whether Credit Genius could be considered a viable alternative to Credit Karma, rather than simply listing the positive aspects of Credit Genius, this provides an objective comparison. Whether Credit Genius will be a better alternative than Credit Karma depends on what you want from a credit monitoring service. For some people, Credit Karma accomplishes everything they need. For others, however, Credit Genius is doing something fundamental that Credit Karma was never intended to do. Understanding this distinction is key to making the right decision. What Credit Karma actually is Credit Karma is primarily a free credit monitoring service. With Credit Karma, you will be able to view your scores from both TransUnion and Equifax (VantageScore), along with information about what is currently listed in your credit report, track changes in your credit report over time, and receive suggestions about various financial products you may be eligible for based on your credit profile. Credit Karma generates income through referrals. It receives a fee any time a user signs up for the credit cards, loans, and other financial products suggested to them via the app. Again, none of this is negative about Credit Karma. They created an extremely valuable product and provided it for free. Credit Karma provides all of the above functions for anyone interested in checking their credit score, viewing their credit report, and obtaining knowledge of the potential financial products they qualify for. What Credit Genius actually is Credit Genius is based on a different approach than Credit Karma. Not “What is your current credit score?” but rather “How can we best work together to move that number?” Rent reporting, combined with backdating; an AI-powered assistant for helping you make better credit decisions; a series of ‘credit games’ providing educational content about personal finance as well as how credit works, all delivered interactively; real-time Experian monitoring. All of this was created to add positive data to your credit report (either by paying bills on time, etc.), to get educated on where you stand financially, and to learn about how credit really works. The rent reporting difference The main functional difference between the two services is rent reporting. This will be the most important (and the biggest) functional difference to the majority of those underserved by the current credit system. Credit Genius offers rent reporting capabilities as well as a “backdate” feature which allows you to submit your rent payments to Experian from months or years ago all at once. There are over 44 million renter households in the United States alone that pay their rent each month and receive no credit recognition for doing so. This is a major function of Credit Genius, it is what makes the service worth using. By signing up for Credit Genius, an individual who has made timely rental payments for 2 years may be able to begin building credit immediately and have 2 years of payment history reported. Credit Karma cannot do the same. The AI guidance difference Credit Karma makes suggestions about which products you may qualify for. Credit Genius provides advice to help you personally improve your credit. Although these both may appear to offer similar benefits, they are different. Credit Karma’s product recommendations give you information regarding the type of financial products that you qualify for based on your current credit score. Credit Genius’ personalized credit guidance gives you actionable steps you can take to increase your score using data from your actual report. It seems one is a marketplace feature and the other is an advisory or coaching tool. For example, if a person wishes to improve their credit score, they would find the coaching tools more directly helpful. The bureau difference By using TransUnion and Equifax as primary data sources, Credit Karma will have access to information about your credit report that a lender may never see. In contrast, Credit Genius primarily uses Experian’s data; Experian is the bureau from which most lenders pull credit reports when they make lending decisions. This distinction matters. If you’re developing your credit history with Credit Genius and that history is being reported to Experian, then the improvements to your credit history are going to land on the bureau that has the highest likelihood of being reviewed by lenders when you apply for a credit card, a car loan, or a rental apartment. That means if there are changes to your credit history that appear in your TransUnion credit file but do not appear in Experian, they can be invisible to the lender who is evaluating your loan request. The business model difference Credit Karma uses a completely free model that relies on referral fees from financial products. If you are using Credit Karma and find yourself interested enough in a credit card offer that you decide to go there after clicking an ad, then Credit Karma will earn some money for sending you to those products. So, while this doesn’t necessarily indicate something about the quality of the product itself, it means that the app designers have a vested interest in bringing financial product offers to you. The product recommendation models and the credit building aspects of Credit Genius represent two very different goals for the way each service has been designed. Who Credit Karma is right for If you’ve built up some type of credit record, but don’t see yourself making any large-scale efforts to dramatically improve your scores and want a free tool to monitor your credit activity and receive alerts, Credit Karma may be a good fit. Who Credit Genius is right for The best candidate to use Credit Genius would be renters who do not have their rental payments included with their credit reporting; someone trying to build their first credit record; someone recovering from past financial errors; someone seeking help using AI to determine what steps to

How Does Credit Genius Compare to Credit Sesame? An Honest Breakdown

Both Credit Genius and Credit Sesame are credit apps. Both apps are free to start. Both apps will give you a credit score. But If you want to compare the two apps or just need to know how they work so you can make better decisions, this is a comparison of the main differences between the two in layman’s terms. What Credit Sesame does Credit Sesame is primarily a credit tracking app. Credit Sesame provides you with your VantageScore through TransUnion, monitors the data contained within your credit report for changes, and sends notifications when anything in your file changes. In addition, Credit Sesame makes basic suggestions about personal finance products that may be relevant to your credit profile. The features included in the free version include all of the standard credit monitoring features. The premium service includes additional detail, monitoring across multiple bureaus, and added identity theft prevention services. Credit Sesame was launched in 2010. It has been used by a large number of consumers. Therefore, if you’re looking for a straightforward and easy-to-use way to passively view your credit score, then Credit Sesame may meet those requirements. What Credit Genius does Credit Genius takes an alternative approach to how credit is managed. The primary focus of Credit Genius is not just tracking information currently in your report but also helping you improve it. The platform has four key characteristics. The Backdating feature allows users to submit historical rental payments to Experian, which can turn those payments into credit-enhancing assets. The AI-powered Credit Assistant analyzes each user’s credit profile and then identifies and provides personalized recommendations on the best course of action to take to increase their score. Credit Games makes financial literacy fun by using interactive educational tools in the form of games to help individuals understand real ways to improve their credit. Real-Time Experian Monitoring provides instant notifications when any changes occur to your Experian file. The core difference Credit Sesame shows you your score. Credit Genius is about changing it. Depending on your stage in your credit journey, that distinction will vary. For example, if you already possess a healthy credit profile and are simply seeking a way to track your file for any changes and potential fraud, a monitoring-based application may meet all of your needs. However, if you are building credit from scratch, attempting to recover from past financial issues or are searching for specific actions to perform to enhance your score, the features that provide the most value are those that create new positive credit activity in your file, not those that provide access to existing data. Bureau coverage Credit Sesame has a free version using TransUnion. Credit Genius monitors Experian. In the U.S., no other bureau is used by lenders more often than Experian for their credit decision-making. This matters. Not all positive credit activities report to all three bureaus. If your rent is reported to Experian and your file is monitored there, then your positive changes are going to be seen when you go to apply for an apartment, a car loan or a credit card. Rent reporting Rent reporting is not a core function offered with Credit Sesame. It is available with Credit Genius and includes backdating, allowing users to upload months or even years of prior rental payments to Experian at once, instead of having nothing but the date of enrollment. For renters, this is one of the biggest differentiators in functionality between Credit Genius and Credit Sesame. There is no way to convert past rent payments into current credit history through Credit Sesame. AI and personalization Credit Sesame recommends financial products that align with your credit profile; therefore, it generally recommends products where you may be qualified. Credit Genius extends the idea of personalization by offering an AI-powered Credit Assistant, which analyzes the data in your credit file and then tells you exactly what actions to take to increase your credit score based on your own set of circumstances. Credit advice is generic when everyone receives the same advice. Personalized advice is when the next step is based on what is contained within your credit file. Financial education Credit Sesame does have some education content. Education is built into the user experience in Credit Genius through Credit Games, which are interactive, gamified learning modules based on the idea that consumers learn and retain financial concepts much better if they are engaged rather than passively. Who each app is built for Credit Sesame is a good option for individuals who already have an existing credit file, are not trying to make substantial improvements to their credit score, and want a free tool to monitor their credit activity and receive alerts. Credit Genius is designed for those who want to build or improve their credit. This can include renters who would like to see their payments included in their credit history, individuals with very little or no credit history, and anyone seeking to get personalized and actionable AI-based direction regarding what steps should be taken next. The bottom line Credit Sesame and Credit Genius both fall into the same category. However, they have distinct functions. Credit Sesame is a credit monitoring app. Credit Genius is an app designed for building credit, with monitoring included. Both can be used if you want to monitor your scores. However, if you want to improve them, this makes a significant difference.

Why Your Credit Score Is Different on Every App You Check

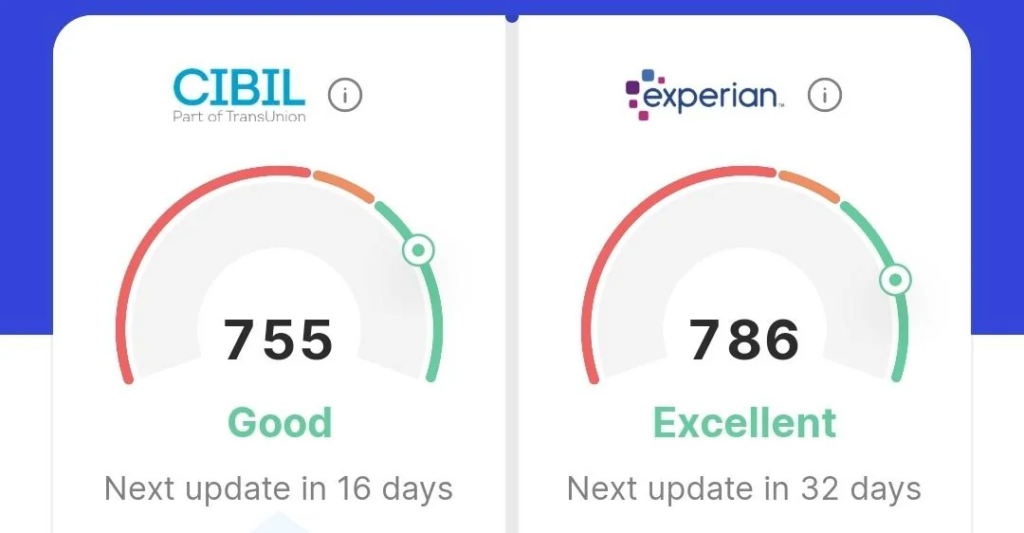

Your credit score is 712 when you check it on one app; 698 on another; 724 at your bank; 681 when you apply for a car loan at a dealer. This creates confusion. “Is the system messed up? Are they lying to me?” Nobody is misleading you. However, the system does create confusion. Once you understand how this happens, you will have less stress and fewer poor financial decisions. There is no single credit score The surprise for many people is that there is no one credit score that all lenders use. In addition to the FICO score, there are dozens of active credit scoring models in the U.S. and each lender uses a different model based on what they are assessing you for. The FICO score is the best-known credit scoring model. Developed by the Fair Isaac Corporation, it also has multiple versions. FICO Score 8 is the most commonly applied version of the FICO score. However, there is a newer version called FICO Score 9 which has been adopted by some of the larger lenders. Industry-specific versions include FICO Auto Score 8 (auto loan) and FICO Bankcard Score 8 (credit card). Mortgage lenders use FICO Score 2, 4 and 5. VantageScore is another model developed by the three major credit bureaus. VantageScore 3.0 and 4.0 are the versions of VantageScore used by many of the free credit monitoring apps and services. Each of the above models evaluates the same credit data differently. Therefore, even if you are using the exact same credit file, you could receive a different number as a result of the different models used. Three bureaus, three different files Another reason you may have different credit scores is because there are three separate credit bureaus (Experian, TransUnion, and Equifax) and each maintains its own independent credit file on you. They do not share information automatically. When a lender or credit card company reports your payment history, they may report to all three credit bureaus, two of them, or just one. Accounts on your credit file may show up on one of your credit bureau reports, but not on the others. For example, an account opened in January may show up on Experian before it appears on TransUnion. Since the underlying data is different at each of the three credit bureaus, and since each of the credit models evaluate the data differently, the resulting credit score at each credit bureau will typically differ. And, in some cases, the difference will be very significant (i.e., a 30-point or 40-point difference). Why free apps often show you a different score than lenders see Most of the free credit monitoring apps use VantageScore 3.0. VantageScore 3.0 is a perfectly good credit scoring model and is very useful for tracking your overall credit health. Most major lenders do not use VantageScore to make lending decisions. Instead, when an applicant applies for a home mortgage, they will usually obtain FICO Score 2 from Experian, FICO Score 4 from TransUnion and FICO Score 5 from Equifax. When making the decision on whether to lend, they will frequently take the middle score. None of those are the scores that were shown to you on your free app. This is why people are often shocked when they apply for a loan and the lender uses a significantly different credit score than the one they thought would be used. The number shown on your app was legitimate. It was simply not the same number that the lender saw. Which score should you actually care about? That depends. If you are simply tracking your credit health over time, any consistently scored model is sufficient. Trends are more important than actual numbers. If your VantageScore increases from 640 to 700 over a period of 6 months, it is safe to say that your FICO scores are improving as well. If you are planning to apply for a mortgage, then check your FICO scores. You can view your FICO scores at MyFICO.com. Knowing which FICO versions the mortgage lenders use and viewing the specific FICO scores prior to applying will give you a much better idea of what the lender will see. FICO Auto Score versions are used for auto loans. FICO Bankcard scores are used for credit cards. FICO 8 is the most widely used across lenders for general purposes. How Credit Genius approaches this Credit Genius uses real-time Experian credit monitoring. This will give you access to an Experian report (one of the three major reporting agencies) and an Experian credit score. The AI-based credit assistant within Credit Genius allows you to see both your current Experian score as well as the actions most likely to impact that score, based on what is reported in your Experian file. Understand that different versions of your score are caused by different models and different reporting bureaus. The next step is to identify the factors affecting your score across all bureaus. Credit Genius offers this understanding. The bottom line Your scores are not manipulated by the creditors or the bureaus. Instead, your scores vary because there is no single standard. There are multiple scoring models, three separate bureaus, and multiple creditors using their own selection of bureau data. Your responsibility is not to memorize all of the various scoring models. Your responsibility is to determine which version of your score is relevant to the creditor’s decision regarding lending to you. Additionally, your responsibility is to develop the habits and behaviors that positively impact all versions of your credit score. Pay your bills on time. Maintain low utilization. Avoid opening unnecessary accounts. Document your rental payments. These actions positively affect every version of your credit score because they positively affect the common data upon which every version of your credit score is calculated.