Does Owing the IRS Affect Your Credit Score?

Tax season leaves a lot of people with an unexpected bill from the IRS. Whether it is a few hundred dollars or several thousand, owing the IRS is stressful on its own. The worry that it might also damage your credit score adds another layer of concern. The short answer is more nuanced than most people expect. Here is exactly how IRS debt interacts with your credit score, what has changed in recent years, and what you should do if you owe. Does simply owing the IRS hurt your credit score? No. Owing money to the IRS does not automatically appear on your credit report or affect your credit score. The IRS does not report tax debts to the credit bureaus the way that lenders and creditors do. Simply having an unpaid tax balance, even a large one, does not create a negative entry on your credit file. This surprises many people who assume that any significant debt to a government agency would show up on their credit report. Tax debt is treated differently from consumer debt in the credit reporting system. What about tax liens? This is where it used to get complicated. Historically, the biggest credit concern around IRS debt was the federal tax lien. When a taxpayer failed to pay a significant tax debt after the IRS made a formal demand for payment, the IRS could file a Notice of Federal Tax Lien, which was a public record claiming the government’s interest in your assets. These liens used to appear on credit reports and could significantly damage credit scores. That changed significantly in 2017. In April of that year, Equifax, Experian, and TransUnion announced that they would no longer include tax liens on consumer credit reports as part of a broader initiative to improve the accuracy of credit reporting. This change went into effect in July 2017. As a result, federal tax liens no longer appear on consumer credit reports from the three major bureaus. If you had a tax lien on your credit report before 2017 it should have been removed. If a tax lien is currently appearing on your report from any of the three major bureaus, it is likely an error and should be disputed. Can IRS debt ever affect your credit? There are indirect ways that unresolved IRS debt can create credit complications, even without appearing directly on your credit report. Even though tax liens no longer appear on consumer credit reports, a federal tax lien is still a public record that affects your ability to sell property or refinance a mortgage. Title searches conducted during real estate transactions will reveal existing tax liens, which must typically be resolved before closing. If the IRS escalates collection efforts, it can levy your bank accounts or garnish your wages. A bank account levy that drains funds you were using to pay other obligations can lead to missed payments on credit accounts, which would damage your credit score. The IRS debt itself does not appear on your credit report but the consequences of unresolved IRS debt can cascade into credit-damaging events. For very large tax debts, the IRS can certify the debt to the State Department, which can deny passport applications or revoke existing passports. This does not affect credit directly but it is a significant consequence of large unresolved tax debt. What to do if you owe the IRS The good news is that the IRS offers several options for taxpayers who cannot pay their full balance immediately, and engaging with these options prevents the escalation that can lead to indirect credit damage. Installment agreement. You can set up a payment plan with the IRS to pay your balance over time. If you owe less than 50,000 dollars and have filed all required returns, you can often set up an online payment plan without speaking to an IRS agent. Installment agreements are not reported to credit bureaus and do not affect your credit score. Offer in Compromise. If you cannot pay the full amount owed and it would create financial hardship, you may qualify for an Offer in Compromise, which allows you to settle your tax debt for less than the full amount. Qualification depends on your income, expenses, and asset equity. Currently Not Collectible status. If paying your tax debt would prevent you from covering basic living expenses, the IRS can place your account in Currently Not Collectible status, temporarily suspending collection activity. Interest and penalties continue to accrue but active collection stops. The worst approach to IRS debt is ignoring it. Ignoring it leads to escalating penalties, interest, and eventually the levies and liens that can create indirect credit damage even if they no longer appear directly on credit reports. Protect your credit while resolving IRS debt While working through an IRS debt situation, protect your credit score by maintaining all other payment obligations. Set up autopay on all credit accounts so that the stress and distraction of dealing with the IRS does not result in missed payments elsewhere. Monitor your credit file during this period as well. Real-time monitoring through a tool like Credit Genius alerts you immediately if anything unexpected appears on your Experian file, giving you the earliest possible warning if any IRS-related record shows up or if another issue emerges while your attention is elsewhere. The bottom line Owing the IRS does not directly damage your credit score. Tax liens were removed from consumer credit reports in 2017 and the IRS does not report tax debts to the credit bureaus. However, ignoring a tax debt can lead to IRS collection actions that create indirect credit damage through missed payments or bank levies. The practical advice is straightforward: engage with the IRS, set up a payment plan if you cannot pay in full, and protect your credit obligations while you work through it. The IRS is one of the more accommodating creditors when it comes to payment arrangements. Use that to your advantage.

What Is Credit Seasoning and Why Do Lenders Care?

If you have ever applied for a mortgage or a significant loan and been told your credit history is too new or that you need more seasoned accounts, you have encountered the concept of credit seasoning without necessarily being told what it means. It is a term used by lenders and credit professionals that most consumers have never heard, yet it affects loan approvals and interest rates in real ways. Here is a clear explanation of what credit seasoning is, why lenders care about it, and what you can do to build it. What credit seasoning means Credit seasoning refers to the age and established history of credit accounts on your credit report. A seasoned account is one that has been open for a meaningful period of time, typically at least twelve to twenty-four months, and has a demonstrated track record of on-time payments during that period. The term comes from the idea that like seasoned wood or seasoned cast iron, a credit account becomes more valuable with age and use. A brand new account tells a lender very little about how you will manage it long-term. An account with three years of consistent payment history tells a much more complete story. Credit seasoning applies to individual accounts as well as to your credit file overall. A lender might look at the age of your oldest account, your newest account, and the average age of all accounts when evaluating your application. Why lenders care about seasoning Lenders use credit history as a predictor of future behavior. The core question they are trying to answer is: based on what this person has done with credit in the past, how likely are they to repay this loan on time? A credit file full of new accounts opened in the last six months provides limited predictive information. The accounts have not had time to demonstrate how they will be managed through different financial circumstances. A credit file with accounts that have been consistently managed for three, five, or ten years provides much stronger evidence of reliable credit behavior. This is particularly true for mortgage lending. Mortgage lenders are evaluating your ability to make consistent payments over fifteen or thirty years. They want to see evidence that you have managed credit responsibly over a meaningful period, not just that you opened several accounts recently. How seasoning affects your credit score Length of credit history accounts for 15% of your FICO score. This factor includes the age of your oldest account, the age of your newest account, and the average age of all accounts. The longer these ages, the better this factor contributes to your score. This is why opening multiple new accounts in a short period can temporarily lower your score. Each new account is unseasoned, it pulls down your average account age and your newest account age. The impact is temporary because the accounts gain age over time, but it is real in the short term. It is also why closing old accounts is generally a bad idea from a credit perspective. A ten-year-old account that you close removes valuable seasoning from your file. Even if you stop using the card, keeping it open preserves that account age. Minimum seasoning requirements in mortgage lending Mortgage lenders often have explicit seasoning requirements that go beyond credit score thresholds. These are minimum periods of time that must have passed since certain credit events before an applicant can qualify. After bankruptcy: Most conventional loan programs require two to four years of seasoning after a Chapter 7 bankruptcy discharge before an applicant qualifies. FHA loans require two years. VA loans may be as short as two years depending on the lender. After foreclosure: Conventional loans typically require seven years of seasoning after a foreclosure. FHA loans require three years. VA loans require two years. After short sale: Conventional loans generally require four years of seasoning after a short sale. FHA loans require three years. These waiting periods exist because lenders want to see evidence of financial rehabilitation after a serious credit event before extending a large, long-term loan. How to build seasoning faster The frustrating reality of credit seasoning is that time is the primary variable. You cannot manufacture seasoning the way you can reduce utilization or dispute errors. Accounts simply need to age. That said, there are strategies that help. Becoming an authorized user on a long-standing account with good history can add seasoning to your file immediately. If a family member adds you to an account they have had for eight years, that account’s history can appear on your report and contribute to your average account age. Rent reporting with backdating is another way to add historical payment data to your file quickly. When Credit Genius reports rent payment history to Experian with backdating of up to 24 months, it adds two years of established payment history to your file. While this affects payment history rather than account age specifically, it contributes to the overall picture of an established, reliable credit profile that lenders associate with seasoning. Opening accounts earlier rather than later is the most fundamental strategy. Every month you delay starting to build credit is a month of seasoning you cannot recover. For young people especially, opening a first credit account at 18 or 19 rather than 25 means six or seven additional years of credit history by the time major financial decisions arrive. What not to do Do not close old accounts in an attempt to simplify your credit profile. Closing old accounts removes seasoning from your file and reduces your available credit. Both outcomes are negative. Do not open multiple new accounts in a short period if you are approaching a major loan application. New accounts signal unseasoned credit and temporarily lower your average account age. Do not confuse credit score with credit seasoning. A person can have a credit score in the 700s but still face seasoning-related questions from mortgage lenders if their accounts are all relatively new. Score

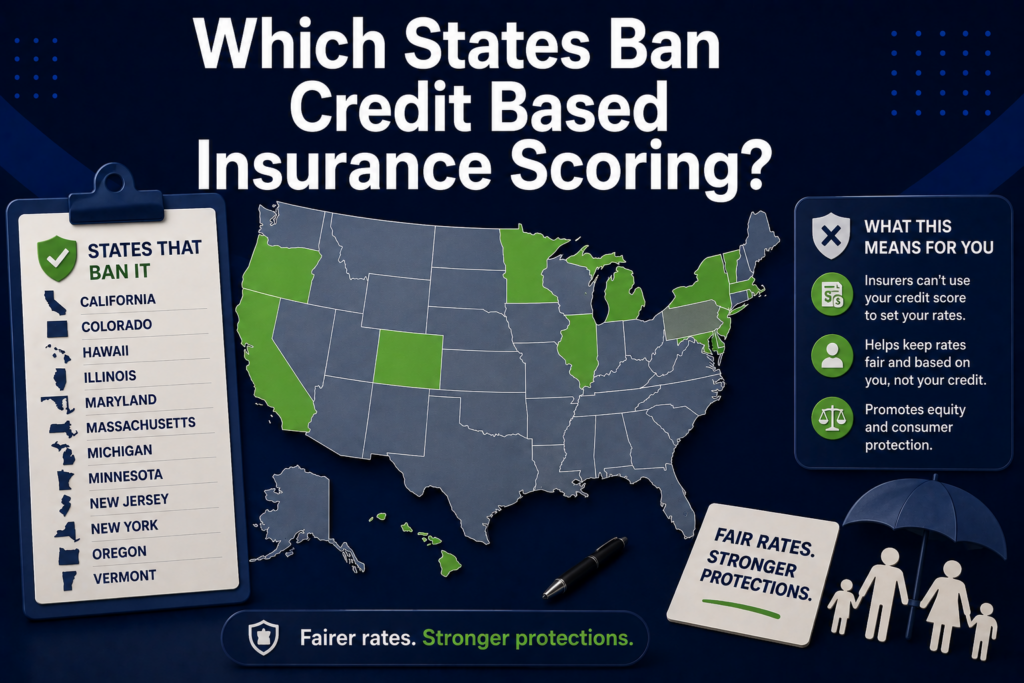

Which States Ban Credit Based Insurance Scoring?

Most Americans do not know that their credit score affects how much they pay for car insurance. In the majority of US states, insurance companies use a credit-based insurance score, which is derived from credit report data, to help set premiums. Drivers with lower credit scores often pay significantly more for the same coverage than drivers with excellent credit, regardless of their actual driving record. But not everywhere. A handful of states have banned or significantly restricted the use of credit in insurance pricing. Here is what you need to know about which states those are, why the practice exists, and what it means for your wallet. What is credit based insurance scoring? A credit-based insurance score is not the same as your FICO credit score. It is a separate score calculated from similar credit report data, including payment history, outstanding debt, credit history length, and types of credit, but weighted differently to predict the likelihood of filing an insurance claim rather than defaulting on a loan. Insurance companies and researchers have found a statistical correlation between credit behavior and insurance claim frequency. People with lower credit-based insurance scores file more claims on average than people with higher scores. Insurers use this correlation to price risk, resulting in higher premiums for policyholders with poor credit even if they have never filed a claim. Critics argue that this correlation reflects socioeconomic factors rather than individual risk, and that using credit data in insurance pricing disproportionately harms lower-income communities and communities of color who tend to have lower credit scores for structural reasons unrelated to their actual insurance risk. States that ban credit based insurance scoring Three states currently ban the use of credit information in auto insurance pricing entirely: California, Hawaii, and Massachusetts. These states prohibit insurers from using credit scores or credit-based insurance scores as a factor in setting premiums, determining eligibility, or renewing policies. In these states, your credit score has no bearing on your auto insurance premium. Rates are set based on other factors including driving record, vehicle type, age, location, and annual mileage. Michigan also has restrictions on the use of credit in insurance pricing, though the rules are more nuanced and have evolved through legislative changes in recent years. For homeowners insurance, the picture is similar. California, Maryland, and a few other states have restrictions or bans on using credit in homeowners insurance pricing, though the specifics vary by state and by the type of restriction in place. What about the other 47 states? In the majority of US states, credit-based insurance scoring is permitted and widely used. The financial impact can be significant. According to research by the Consumer Federation of America, drivers with poor credit can pay 50 to 100% more for auto insurance than drivers with excellent credit for identical coverage in the same location. On a 1,500 dollar annual auto insurance premium, that represents an additional 750 to 1,500 dollars per year purely from the credit score factor. Over five years, that is 3,750 to 7,500 dollars in additional premium costs attributable to credit alone. The impact on homeowners insurance varies by insurer and state but can also be significant. Some studies have found premium differences of 20 to 50% or more between policyholders with excellent and poor credit in states where credit scoring is permitted. Legislative trends The COVID-19 pandemic sparked renewed scrutiny of credit-based insurance scoring after research showed that communities hardest hit economically by the pandemic, many of which were communities of color, would face insurance premium increases tied to credit score declines caused by the pandemic rather than by any change in their actual risk profile. Several states considered or passed temporary restrictions on using pandemic-related credit changes in insurance pricing. The broader debate over whether credit-based insurance scoring should be restricted or banned entirely has continued in state legislatures across the country, with consumer advocates pushing for expansion of the California, Hawaii, and Massachusetts model. The regulatory landscape in this area is evolving. Consumers in states currently permitting credit-based insurance scoring should monitor legislative developments that could affect their premiums. What you can do if you live in a state that allows credit based insurance scoring The most direct action available is improving your credit score, which improves your credit-based insurance score along with it. The same behaviors that build a strong FICO score, paying on time, keeping utilization low, and maintaining a clean credit history, also improve the credit-based insurance score insurers use. When your credit score improves meaningfully, ask your insurer to re-run your credit-based insurance score. Many insurers will do this at renewal or upon request. A significant improvement in your credit profile can result in a lower premium without changing your coverage. Shopping your insurance policy when your credit has improved is also worthwhile. Different insurers weight credit differently in their scoring models. Getting quotes from multiple insurers after a credit improvement can surface premium differences of hundreds of dollars per year. Tools like Credit Genius that provide real-time Experian monitoring and personalized guidance on the actions most likely to improve your score help you work toward the credit improvements that reduce costs across multiple financial products simultaneously, including insurance premiums in states where credit scoring is permitted. The bottom line Credit-based insurance scoring is banned in California, Hawaii, and Massachusetts for auto insurance and restricted in a few additional states. In the remaining states, your credit score affects what you pay for insurance and the financial impact can be substantial. If you live in a state where credit scoring is permitted, improving your credit score reduces your insurance costs alongside every other financial benefit a stronger score provides. The insurance premium reduction is one more reason why credit building pays off in real, measurable dollars.

What Is a Store Credit Card and Should You Ever Open One?

You are at checkout and the cashier offers you 20% off today’s purchase if you open a store credit card. It happens at clothing stores, furniture retailers, electronics chains, and department stores across the country. The offer sounds appealing in the moment. But the question of whether you should actually say yes is more complicated than the discount makes it seem. Here is a clear-eyed look at what store credit cards are, how they affect your credit, and when they are and are not worth opening. What a store credit card actually is Store credit cards come in two varieties. A closed-loop store card can only be used at the specific retailer or family of retailers that issued it. An open-loop store card, sometimes called a co-branded card, carries a Visa, Mastercard, or similar network logo and can be used anywhere that network is accepted. Both types are issued by banks or financial institutions on behalf of the retailer. Both report to the credit bureaus and function as revolving credit accounts for credit scoring purposes. The main difference is where you can use them and the rewards structure around them. How store cards affect your credit score The application causes a hard inquiry. Every store card application results in a hard inquiry on your credit report. Hard inquiries have a small temporary negative impact on your score, typically a few points, and remain on your report for two years. If you are opening one card the impact is minor. If you open several cards across different stores in a short period the cumulative effect is more significant. It lowers your average account age. Every new account you open lowers your average account age, which is a factor in your credit score. If you have been building credit for five years and open a new store card, your average account age drops. The impact depends on how many other accounts you have and how old they are. It adds available credit and potentially lowers utilization. A new card adds to your total available credit. If your existing balances stay the same, your overall utilization ratio drops, which is positive for your score. However, store cards typically come with low credit limits, so the utilization benefit may be modest. High utilization on the store card itself is a risk. Store cards often have low credit limits, sometimes as low as 500 dollars. If you use the card for a significant purchase and carry a balance, the utilization on that specific card can be very high even if your overall utilization is fine. Per-card utilization is a factor in scoring models as well as total utilization. Interest rates are typically very high. Store credit cards carry some of the highest interest rates in the consumer credit market, frequently 28% to 32% or above. If you carry a balance for even a month or two, the interest cost often exceeds any discount you received for opening the card. When opening a store card makes sense You are making a large purchase and will pay it off immediately. If you are buying 800 dollars of furniture and a store card gives you 20% off that purchase, you save 160 dollars. If you pay the balance in full before the statement closes, you pay no interest. The hard inquiry costs a few points temporarily. For a large purchase you were going to make anyway, this math can work in your favor. You shop at that retailer frequently enough to use the rewards. Co-branded store cards often offer meaningful ongoing rewards at their partner retailer, sometimes 5% back or more. If you consistently spend significant amounts at a specific store, the rewards can accumulate to real value over time. Store cards often have lower approval requirements than mainstream credit cards. For someone with a thin or fair credit file who cannot yet qualify for a better card, a store card can be a stepping stone. The key is to use it minimally, pay it in full every month, and treat it as a temporary tool while building toward better products. When opening a store card does not make sense You are about to apply for a major loan. If you are planning to apply for a mortgage, car loan, or any major credit product in the next six to twelve months, do not open any new credit accounts including store cards. The hard inquiry and the reduction in average account age are exactly what you do not want on your file before an important application. You might carry a balance. If there is any chance you will not pay the full balance immediately, the interest rate on a store card will almost certainly cost you more than the discount you received. Store card interest rates are among the highest in the consumer credit market. You already have multiple credit cards. If you already have several well-managed credit cards with good terms, a store card adds complexity and risk without meaningful credit benefit. A better card with broader acceptance and stronger rewards is almost always preferable. You are opening it purely for the discount. Opening a card for a one-time discount on a small purchase, then never using it again, is rarely worth it. The hard inquiry, the account management overhead, and the risk of forgetting to pay the first statement on time make the discount a poor trade in most cases. What to do if you already have store cards If you have store cards you opened in the past and never use, do not rush to close them. Closing accounts reduces your available credit and can shorten your average account age. Leave them open, put a small recurring charge on them if possible to keep them active, and pay the balance in full each month. If a store card has an annual fee you do not want to pay, call the issuer and ask whether they can waive it or convert the account to a

What the CFPB Credit Card Late Fee Cap Means for Your Credit

In 2024 the Consumer Financial Protection Bureau finalized a rule that would cap credit card late fees at eight dollars for most credit card issuers, down from the typical 30 to 41 dollar fees that had become standard. The rule was immediately challenged in court by the banking industry and its implementation has been tied up in legal proceedings. Regardless of where the legal battle ultimately lands, the rule and the debate around it have significant implications for how Americans think about late fees, credit card costs, and credit building. Here is what you need to know. What the rule actually says The CFPB’s rule, issued under authority granted by the Credit Card Accountability Responsibility and Disclosure Act of 2009, known as the CARD Act, would limit late fees to eight dollars for a first missed payment and the same amount for subsequent missed payments. Current rules allow fees up to 30 dollars for a first late payment and up to 41 dollars for additional late payments within six months. The CFPB estimated that the rule would save American consumers approximately 10 billion dollars per year in late fees. The banking industry contested this, arguing that the fees serve as a deterrent against late payments and that reducing them would lead issuers to raise interest rates or reduce credit access to offset the lost revenue. The rule applies to larger credit card issuers and exempts smaller institutions with fewer than one million open accounts. What the rule does not change This is the most important thing to understand about the late fee rule from a credit perspective: it does not change how late payments are reported to the credit bureaus or how they affect your credit score. A payment reported as 30 days late damages your credit score the same amount whether the late fee was 8 dollars or 41 dollars. The fee is a financial penalty charged by the lender. The credit report mark is a separate event reported to the bureaus. Reducing the fee does not reduce the credit score impact. If the rule leads some consumers to be less concerned about missing a payment because the fee is smaller, that would be the wrong conclusion to draw. The fee is one cost of a late payment. The credit score damage is a separate and often much larger cost. The potential unintended consequences The banking industry’s argument that reduced late fees would lead to higher interest rates or tighter credit access is not without basis. Credit card issuers need to price risk into their products. If one revenue source is capped, they may adjust elsewhere. Some analysis has suggested that the primary beneficiaries of late fees are the issuers themselves, since the fees often exceed the actual cost to the issuer of a late payment. Other analysis suggests that consumers who miss payments regularly are higher-risk borrowers and that higher fees serve a legitimate deterrence function. What is clear is that the net effect on consumers depends on how issuers respond. If they raise interest rates to compensate, consumers who carry balances may pay more overall even with lower late fees. If they tighten credit access, some consumers may find it harder to get approved. What this means for credit building For consumers actively building or protecting their credit score, the late fee cap changes very little in practical terms. The single most important credit principle remains unchanged: pay on time, every time. A missed payment costs 50 to 100 points or more on your credit score and stays on your report for seven years. That is a cost that dwarfs any late fee, capped or uncapped. The fee reduction does not change the calculus around the importance of on-time payments. Set up autopay for the minimum payment on every account. This ensures you never miss a payment due to forgetfulness regardless of what the late fee happens to be. The fee is the least of the consequences of a missed payment. The broader CFPB credit reform agenda The late fee rule is one piece of a broader CFPB agenda that has significant implications for how credit works in America. Other major actions have included the removal of medical debt from credit reports, guidance on Buy Now Pay Later regulation, and ongoing scrutiny of credit reporting accuracy. The removal of medical collections under 500 dollars from credit reports in 2023 was a significant change that directly improved scores for millions of Americans who had medical debt on their files. This is an example of a regulatory change that had a real and immediate credit score impact, unlike the late fee cap which leaves the credit reporting system unchanged. Staying informed about regulatory changes affecting the credit system is worth doing. Tools like Credit Genius that provide real-time Experian monitoring and AI-powered guidance will reflect these changes as they take effect and help users understand how their own credit profile is affected. The bottom line The CFPB credit card late fee cap is a significant consumer finance development that could save Americans billions of dollars in fees if implemented as written. Its legal future remains uncertain as of 2026.For your credit score, the rule changes nothing. Late payments damage your credit regardless of the fee size. The most important thing you can do remains the same: pay on time, every time, on every account. No regulatory change makes that less true.

Will Buy Now Pay Later Eventually Replace Credit Cards?

Buy Now Pay Later has grown from a niche checkout option to one of the most widely used payment methods in the United States. Tens of millions of Americans now use it regularly. The companies behind it are valued in the billions. And a growing number of younger consumers appear to prefer it over traditional credit cards. So will Buy Now Pay Later eventually replace credit cards? The short answer is no, at least not in any complete or near-term sense. But the longer answer reveals something more interesting about how the two products are evolving and what that means for your credit. What Buy Now Pay Later does well Buy Now Pay Later solves a specific problem elegantly: it lets consumers spread the cost of a purchase over a short period, typically four installments over six weeks, without the complexity of a credit card application, a credit limit, or revolving debt. For many consumers, particularly younger ones who are skeptical of credit card debt or who have been excluded from traditional credit products, Buy Now Pay Later is more accessible and feels more transparent. You know exactly what you will pay and when. There is no revolving balance that can grow if you only pay the minimum. The frictionless checkout experience has also driven rapid adoption. Adding a Buy Now Pay Later option at checkout takes seconds. It does not require an existing account or a credit check in most cases. For retailers, it increases conversion and average order value. For consumers, it feels less like debt and more like a payment schedule. What Buy Now Pay Later does not do Despite its growth, Buy Now Pay Later has significant limitations that prevent it from replacing credit cards for most consumers and use cases. It does not build credit reliably. Credit cards with consistent on-time payments build a strong credit history. Buy Now Pay Later reporting to credit bureaus is inconsistent across providers and still evolving. For consumers who need to build or maintain a credit score for housing, auto loans, or mortgages, credit cards remain the more reliable credit-building tool. It does not offer the same consumer protections. Credit cards come with robust federal protections including the ability to dispute charges, chargeback rights, and zero liability for fraudulent purchases. Buy Now Pay Later protections vary significantly by provider and are generally weaker. The CFPB has noted this gap and has signaled interest in extending credit card-style protections to Buy Now Pay Later products. It does not offer rewards. The rewards ecosystem built around credit cards, including cash back, travel points, and sign-up bonuses, represents significant value for cardholders who pay their balance in full. Buy Now Pay Later products generally offer no equivalent. It does not work everywhere. Credit cards are universally accepted. Buy Now Pay Later is available only at participating merchants. For everyday spending like groceries, gas, and utilities, credit cards remain the only option. It does not handle large or ongoing expenses. Buy Now Pay Later is designed for discrete purchases. It does not work for recurring bills, subscriptions, or large ongoing expenses in the way that a credit card with a revolving limit does. How credit cards are responding The credit card industry has not ignored Buy Now Pay Later’s growth. Major card issuers have responded by adding installment plan features directly to existing cards. American Express, Chase, Citi, and others now offer their own versions of pay-over-time options for large purchases. This hybrid approach combines the credit-building benefits, consumer protections, and universal acceptance of credit cards with the installment payment structure that makes Buy Now Pay Later appealing. For many consumers, this may be the best of both worlds. The regulatory picture The CFPB has taken an increasing interest in Buy Now Pay Later and in 2024 issued guidance clarifying that many Buy Now Pay Later products should be treated as credit cards under existing law, which would subject them to the same disclosure requirements, dispute rights, and consumer protections. This regulatory pressure is pushing the industry in two directions simultaneously: toward more consumer-friendly terms that look more like credit cards, and toward more consistent credit bureau reporting. Both developments will change the credit implications of Buy Now Pay Later over the next several years. What this means for your credit As Buy Now Pay Later reporting to credit bureaus becomes more common, the credit implications of these products will become more significant in both directions. On-time payments may begin building credit more reliably. Missed payments will increasingly damage credit scores. For anyone actively building or managing their credit, the practical implication is to treat Buy Now Pay Later obligations with the same discipline as credit card payments. Missed payments are increasingly likely to show up on your credit report, and the informal feeling of the product should not obscure that reality. For credit building specifically, traditional tools like credit cards, credit builder loans, and rent reporting through services like Credit Genius remain more reliable than Buy Now Pay Later because their reporting relationships with credit bureaus are established and consistent. The bottom line Buy Now Pay Later will not replace credit cards. It will continue to grow as a complement to credit cards for specific purchase types and specific consumer segments. The two products are converging in some ways, with credit cards adding installment features and Buy Now Pay Later products facing pressure to add consumer protections and credit reporting.For consumers, the takeaway is straightforward. Use Buy Now Pay Later where it genuinely helps you manage a purchase. Treat every payment obligation seriously regardless of how informal the product feels. And if building or maintaining your credit score is a priority, make sure the financial behaviors you are relying on to do that are connected to products with reliable, consistent bureau reporting.

How Credit Scores Differ by Race and Income in America

Credit scores are presented as objective measures of individual financial behavior. In practice, the data shows persistent and significant gaps in credit scores across racial and income lines. Understanding those gaps, where they come from, and what they mean for the people affected by them is important context for anyone trying to build or improve their credit in America. This article covers what the data actually shows, the structural reasons behind it, and what individuals can do to build credit despite systemic disadvantages. What the data shows The credit score gaps between racial groups in the United States are well documented. Research from the Urban Institute and other policy organizations consistently finds that Black and Hispanic Americans have significantly lower average credit scores than white and Asian Americans. A 2022 analysis found that the average credit score for Black Americans was approximately 100 points lower than for white Americans. Income correlates with credit scores as well, though the relationship is more nuanced than it might appear. Higher income households tend to have higher average credit scores, but the correlation is not one-to-one. Lower income households are more likely to be credit invisible, meaning they have no credit file at all, or to have thin files with limited history. The Consumer Financial Protection Bureau has estimated that approximately 26 million Americans are credit invisible and another 19 million have files too thin or stale to generate a reliable score. These populations are disproportionately Black, Hispanic, and lower income. Why these gaps exist: the structural factors The credit score gaps between racial and income groups did not emerge from individual behavior alone. They are the product of structural factors that have shaped access to credit building opportunities across generations. Historical exclusion from credit. Redlining, discriminatory lending practices, and explicit exclusion of Black Americans from FHA-backed mortgages and conventional credit products through much of the twentieth century meant that generations of Black families were prevented from building the credit history and home equity that wealth and credit scores are built on. These exclusions were not individual failures. They were policy. The homeownership gap. Mortgage payments are automatically reported to the credit bureaus and contribute directly to credit scores. Homeownership rates among Black Americans are significantly lower than among white Americans, a gap that traces directly to historical exclusion and continues to compound. Renters, who are disproportionately Black and Hispanic, make their largest monthly payment without receiving credit recognition for it unless they actively report it. Lower income creates direct credit challenges: higher likelihood of carrying high utilization, greater vulnerability to missed payments during financial shocks, and less ability to maintain the savings buffer that protects credit during emergencies. The racial wealth gap, estimated at roughly ten to one between white and Black households by the Federal Reserve, means these income-related credit challenges fall disproportionately on communities of color. Predatory lending. Communities of color have been disproportionately targeted by high-interest payday lenders, predatory auto dealers, and subprime mortgage products. These products often create credit damage rather than building credit, leaving borrowers with derogatory marks from products that were designed to extract rather than support. Credit invisibility. Communities with lower homeownership rates, less access to mainstream banking, and less generational wealth to pass on credit-building knowledge and authorized user access are more likely to be credit invisible. Credit invisibility is not a reflection of financial irresponsibility. It is a reflection of which financial behaviors the credit system was designed to recognize. Does the credit scoring system itself contribute to the gaps? This is a legitimately debated question among researchers and policy advocates. The credit scoring system does not use race as a factor and is prohibited from doing so. But critics argue that factors like the exclusion of rent and utility payments from traditional scoring, the emphasis on account age which disadvantages those who were historically excluded from credit, and the reliance on data from a system that has historically underserved communities of color means the system encodes historical inequity even without explicitly using race. Defenders of the current system argue that credit scores are accurate predictors of repayment behavior across all demographic groups and that the solution to the gap is expanding access to credit rather than changing the scoring methodology. Both arguments contain truth. The gaps in credit scores reflect real differences in credit behavior that are themselves produced by structural inequity. Addressing the gaps requires both expanding what counts as credit-worthy behavior and addressing the underlying conditions that create unequal credit outcomes. What is being done to address the gaps Several policy and industry developments in recent years are directly aimed at reducing credit score disparities. The expansion of rent reporting is one of the most significant. Legislation in several states now requires landlords to offer rent reporting to tenants. The CFPB has encouraged broader use of alternative data including rent and utility payments in credit underwriting. Companies like Credit Genius that report rent to Experian are part of an industry-wide movement to make the credit system recognize the financial behaviors of renters, who are disproportionately people of color. The removal of medical debt from credit reports, completed for collections under 500 dollars in 2023 and expanded further, disproportionately benefits communities of color who are more likely to carry medical debt due to lower rates of insurance coverage. Alternative credit scoring models that incorporate rent, utility, and other non-traditional payment data are gaining traction among some lenders, particularly for mortgage underwriting. What individuals can do Structural problems require structural solutions and individual action alone cannot close gaps that were produced by decades of policy. But understanding the system and using the tools available to work within it remains the most practical path forward for individuals navigating it right now. Report your rent. If you are paying rent on time, that payment should be on your credit file. Credit Genius reports to Experian with backdating, giving you credit for the financial behavior you are already demonstrating. Dispute errors. Research suggests that errors

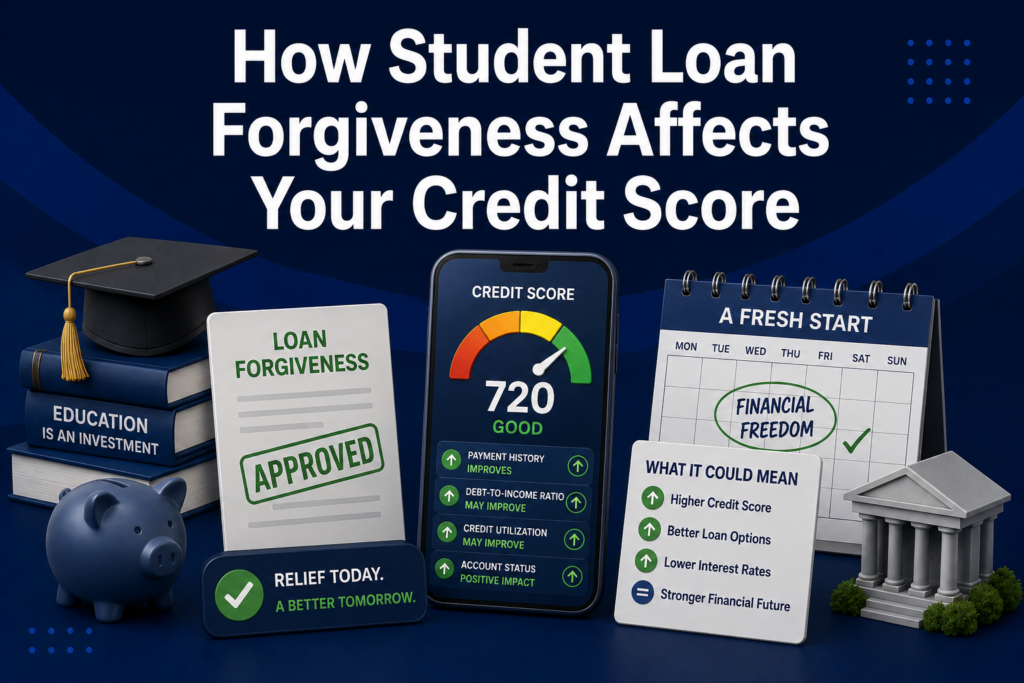

How Student Loan Forgiveness Affects Your Credit Score

Student loan forgiveness sounds like an unambiguous win. Your debt is wiped out and you never have to pay it back. But when it comes to your credit score, the reality is more nuanced. Loan forgiveness can affect your credit in ways that are positive, neutral, or occasionally temporarily negative depending on how your loans were structured and what your credit file looks like before forgiveness. Here is a clear breakdown of what actually happens to your credit when student loans are forgiven. The good news first For most borrowers, student loan forgiveness is either neutral or mildly positive for their credit score. The forgiven loan shows up on your credit report as paid in full or closed with a zero balance. A loan that is paid in full is a positive credit event, and it removes what may have been a significant balance from your total debt load. If your forgiven loans had been in good standing throughout repayment, the account history, including all those years of on-time payments, remains on your credit report for up to ten years after the account closes. That positive payment history continues to benefit your score for years after the loan is gone. The potential temporary downside The reason some borrowers see a temporary score dip after loan forgiveness comes down to two factors: credit mix and account age. Having a mix of revolving accounts like credit cards and installment accounts like loans contributes positively to credit mix, which accounts for 10% of your FICO score. When an installment account is closed, your mix becomes less diverse. If student loans were your only installment accounts, their forgiveness and closure can slightly reduce this factor. Average account age. The length of your credit history accounts for 15% of your score, including the average age of all open accounts. When a long-standing loan account closes, it no longer contributes to your average account age calculation for open accounts. If your student loans were among your oldest accounts, their closure can lower your average account age slightly. Both of these effects tend to be modest, often just a few points, and temporary. The closed account remains on your report for up to ten years and its positive history continues to count during that time. What about debt-to-income ratio? Debt-to-income ratio does not appear on your credit report and is not a factor in your credit score. However, it matters significantly to lenders when you apply for mortgages and other major loans. Having student loan debt forgiven reduces your monthly debt obligations and therefore improves your DTI. This can be a significant benefit if you were previously unable to qualify for a mortgage because your student loan payments were pushing your DTI above lender thresholds. Forgiveness may open the door to homeownership that the debt was blocking. What about loans that were in default before forgiveness? This is where it gets more complicated. If your student loans were in default before being forgiven, the negative marks associated with that default, including late payment records and the default notation itself, do not automatically disappear when the loan is forgiven. A loan forgiven through Public Service Loan Forgiveness or income-driven repayment forgiveness programs, where the borrower was in good standing throughout, closes as paid in full with no negative history attached. A loan forgiven after a period of default may still carry the derogatory marks from that period on the credit report, even though the balance is now zero. If your loans had negative marks before forgiveness and those marks are still showing on your report, you can dispute any inaccuracies but accurately reported derogatory information from a default period remains on your report for seven years from the original delinquency date regardless of forgiveness. The income tax question This is not a credit question but it is an important one. Depending on the type of forgiveness and current tax law, forgiven student loan balances may be treated as taxable income in the year of forgiveness. This does not affect your credit score but it can affect your financial situation in that year. Federal student loan forgiveness under income-driven repayment plans was tax-free through 2025 under temporary provisions. The tax treatment beyond that period depends on legislation in effect at the time of forgiveness. If you are approaching forgiveness, it is worth understanding the potential tax implications in advance. How to protect your credit around loan forgiveness In the months leading up to expected loan forgiveness, avoid opening new credit accounts that would lower your average account age further. If you have other installment accounts in good standing, maintain them to preserve your credit mix. After forgiveness, monitor your credit file closely to make sure the loan is reported correctly as paid in full or closed with zero balance. If anything is reported inaccurately, dispute it promptly. If the closure of your student loans reduces your credit mix and you want to add a new installment account to maintain diversity, a credit builder loan is a low-risk option. It adds an installment account without taking on significant debt. And if you are a renter, this is a good moment to ensure your rent payments are being reported to the credit bureaus through a service like Credit Genius. Adding verified rent payment history to your Experian file provides ongoing positive payment data that supports your score as your credit profile adjusts to the closure of your student loans. The bottom line Student loan forgiveness is generally neutral to mildly positive for your credit score when the loans were in good standing. You may see a small temporary dip from credit mix and account age effects, but the positive payment history from years of on-time payments remains on your report and continues to benefit you.The financial benefit of eliminating the debt and improving your debt-to-income ratio almost always outweighs any minor credit score adjustment. For most borrowers, forgiveness is unambiguously good news, credit included.

How Your Credit Score Affects Every Major Purchase You Make

Most people think about their credit score when they are applying for something specific, a loan, a credit card, an apartment. But the impact of your credit score is broader and more constant than that. It quietly shapes the cost of almost every significant financial transaction in your life, often in ways you never see directly. Here is a complete picture of how your credit score affects the major purchases and financial decisions you will make throughout your life, with real numbers where available. Renting an apartment Your credit score is one of the first things most landlords and property management companies check. In competitive rental markets, a score below 620 can result in outright rejection. A score in the Fair range often means being asked for a larger security deposit, sometimes two or three months of rent rather than one. On a 1,500 dollar per month apartment, the difference between a one-month and a two-month deposit is 1,500 dollars of your money sitting tied up rather than available to you. Over the course of several rentals across your 20s and 30s, the cumulative deposit cost of a low credit score can run into thousands of dollars. Beyond deposits, a low score may also limit which apartments you can qualify for, pushing you toward less competitive housing in less desirable locations. The real cost of poor credit on housing is not just financial. It affects where you can live. Buying a home This is where the credit score impact is most dramatic in absolute dollar terms. Mortgage interest rates vary significantly by credit score tier, and on a large, long-term loan those rate differences translate into tens of thousands of dollars. On a 350,000 dollar 30-year mortgage, the difference between a 680 credit score and a 760 credit score can be approximately 0.75 to 1.25 percentage points in interest rate. At a 1 percentage point difference, that translates to roughly 200 dollars more per month in mortgage payments and approximately 72,000 dollars more in total interest paid over the life of the loan. That is not a small number. It is the cost of a car, a significant portion of a college education, or years of retirement savings. All determined by a three-digit number. Buying a car Auto loan interest rates vary significantly by credit score. According to Experian’s State of the Automotive Finance Market report, borrowers with excellent credit scores in the 781 to 850 range received average new car loan rates of around 5% in recent years. Borrowers in the subprime range of 501 to 600 paid average rates above 14%. On a 30,000 dollar 60-month auto loan, the difference between 5% and 14% interest is approximately 150 dollars per month and roughly 9,000 dollars in total interest paid over the life of the loan. That is an amount that would easily cover the cost of a significantly better vehicle if your credit score had been higher. People with very poor credit may also be pushed toward buy-here-pay-here dealerships with even higher rates and less favorable terms, compounding the cost further. Car insurance This one surprises most people. In most US states, auto insurers use credit-based insurance scores to help determine your premium. These scores are similar but not identical to credit scores and they reflect the statistical correlation between credit behavior and insurance claim frequency. The impact is significant. According to a study by the Consumer Federation of America, drivers with poor credit can pay 50 to 100% more for auto insurance than drivers with excellent credit for the same coverage. On a 1,500 dollar annual premium, that is an additional 750 to 1,500 dollars per year, or 60 to 125 dollars per month, purely because of credit score. Three states, California, Hawaii, and Massachusetts, ban the use of credit in auto insurance pricing. In all other states, your credit score is a factor in what you pay to drive. Home insurance Home insurance premiums are also affected by credit-based insurance scores in most states. The same principle applies: insurers use credit data as a predictor of claim likelihood. Poor credit can result in meaningfully higher home insurance premiums, adding to the ongoing cost of homeownership for people who are already paying more on their mortgage because of a lower score. Personal loans Personal loans are used for everything from medical expenses to home improvements to consolidating debt. The interest rate on a personal loan is heavily determined by your credit score. Rates for borrowers with excellent credit can be as low as 6 to 8%. Borrowers with poor credit may face rates of 25 to 36% or higher, if they can get approved at all. On a 10,000 dollar personal loan over three years, the difference between 8% and 25% interest is approximately 2,500 dollars in additional interest. For someone using a personal loan to cover a medical emergency or essential repair, that difference is felt immediately and significantly. Credit cards Credit card interest rates, known as APR, vary dramatically based on creditworthiness. Premium rewards cards with the best benefits are generally only available to people with good or excellent credit. Borrowers with fair or poor credit are often limited to cards with higher rates, lower limits, and annual fees. For people who carry a balance, the interest rate difference compounds quickly. A 3,000 dollar balance at 16% APR costs about 480 dollars per year in interest. The same balance at 28% costs about 840 dollars per year. That 360 dollar annual difference is real money that goes directly to the card issuer rather than toward the balance. Employment Some employers, particularly those in financial services, government, and positions requiring security clearances, run credit checks as part of the background screening process. Poor credit does not automatically disqualify a candidate in most cases, but it can raise questions and in some industries it can affect hiring decisions. Employers must obtain your permission before running a credit check and in some states credit checks for employment

Why Being Rich Does Not Mean Having Good Credit

There is a persistent assumption that wealth and good credit go hand in hand. That if someone earns a high income, has significant savings, or comes from money, their credit score must reflect that. It does not work that way. Credit scores and wealth are measuring completely different things, and the confusion between the two causes real problems for people on both ends of the income spectrum. Here is why financial wealth and a strong credit score are not the same thing and what that means practically. Your income is not on your credit report This is the foundational fact that most people do not know. Your salary, your investment income, your savings account balance, and your net worth do not appear anywhere on your credit report. A credit report contains information about credit accounts and debt obligations only: payment history, balances, account ages, inquiries, and public records. The credit bureaus, Experian, TransUnion, and Equifax, collect data from lenders and creditors. They do not collect data from employers, banks, or investment firms about how much money you have or earn. Your credit score is calculated entirely from the data in your credit file, none of which reflects your financial resources. How wealthy people end up with bad credit They pay for everything in cash. This is more common among high earners than most people realize. Someone who has always earned enough to buy cars outright, pay rent in cash, and never need a credit card may have a thin or nonexistent credit file. The credit system has no data on them. No data means no score, and no score is treated similarly to bad credit by most lenders and landlords. They have missed payments despite having money. High income does not prevent forgetfulness. A busy executive who forgets to pay a credit card bill, a wealthy landlord who lets an old debt slip through the cracks, or an entrepreneur who deprioritizes personal finance while building a business can all end up with derogatory marks that have nothing to do with their ability to pay. They have high utilization despite high income. Credit utilization is based on how much of your available credit you are using, not on how much you earn. Someone with a 50,000 dollar credit limit who regularly carries a 40,000 dollar balance has 80% utilization regardless of their income. High utilization is one of the fastest ways to damage a credit score. Wealthy young adults who have relied on family money or high starting salaries without building any credit history can have thin files despite significant financial resources. Length of credit history is a scoring factor that money cannot buy. It only comes with time. They have been through financial disruption. Business failures, divorce, legal judgments, and other financial disruptions can damage credit regardless of wealth. Someone who was wealthy and then went through a messy business bankruptcy may carry significant negative marks even if they have rebuilt their finances substantially. How people with modest incomes build excellent credit The inverse is equally true and equally instructive. People with modest incomes can and do achieve excellent credit scores, sometimes well above 800, by managing their credit behavior consistently over time. The formula is simple: pay every obligation on time, keep credit card balances low relative to the limit, keep accounts open over a long period, and avoid opening new accounts unnecessarily. None of these behaviors require high income. They require discipline and consistency, which are independent of how much money someone earns. A renter earning 35,000 dollars a year who has paid rent on time for five years, uses a secured card with low utilization, and has never missed a payment can have a higher credit score than a lawyer earning 250,000 dollars who pays cash for everything and has no credit history. What credit actually measures Credit scores measure one thing: the statistical likelihood that you will repay borrowed money on time based on your past behavior with borrowed money. That is it. They do not measure wealth. They do not measure character. They do not measure your financial stability in any holistic sense. This is why the system produces results that seem counterintuitive when you think about it from a wealth perspective. The system is not measuring wealth. It is measuring a specific kind of financial behavior, and that behavior is largely independent of income. Why this matters for renters and cash-paid workers The flip side of the wealth-credit disconnect is equally important. People who feel financially stable but have thin credit files are not being judged on their actual financial reliability. They are being judged on a system that has no data on them. A renter who has paid 1,200 dollars a month reliably for three years is demonstrating exactly the kind of financial behavior credit scores are supposed to capture. But if that rent is not being reported to the credit bureaus, the system sees nothing. The person is penalized not for bad behavior but for invisible behavior. This is precisely the problem that rent reporting through Credit Genius is designed to address. By submitting rent payment history to Experian, including backdated history of up to 24 months, Credit Genius makes visible the financial behavior that the credit system was otherwise ignoring. The renter’s actual reliability finally shows up where it matters. The practical implications If you have significant income or assets but a thin or poor credit file, the solution is not to wait for the credit system to recognize your wealth. It never will. The solution is to build a credit history deliberately, just like someone starting from scratch. Open a credit card if you do not have one. Use it for small purchases and pay it off monthly. Report your rent if you are renting. Keep any existing accounts in good standing. Over twelve to twenty-four months of consistent positive behavior, your credit file will catch up to your actual financial reliability. The credit system is indifferent to your