How to Build an Emergency Fund and Good Credit at the Same Time

Most personal finance advice treats emergency funds and credit building as separate goals that you tackle one at a time. Build your emergency fund first, then work on credit. Or get your credit sorted, then focus on savings. In practice, most people do not have the luxury of addressing one before the other. They need both, and they need to be building both simultaneously. The good news is that these two goals are not in conflict. With the right approach they reinforce each other. Here is how to build both at the same time without feeling like you are being pulled in two directions. Why you need both and why they are connected An emergency fund and good credit serve similar purposes from different directions. An emergency fund is liquid cash you can access immediately when something goes wrong. Good credit is the ability to access borrowed money quickly and cheaply when something goes wrong. Together they give you two layers of financial resilience. The connection goes deeper. One of the most common ways people damage their credit is by missing payments during financial emergencies. A job loss, medical bill, or car repair that wipes out available cash can lead to missed minimum payments, which are among the most damaging credit events you can experience. An emergency fund prevents that cascade. It protects your payment history, the most important factor in your credit score, from being disrupted by events outside your control. Building both simultaneously is not just possible. It is strategically smarter than doing one at a time. Start with a minimum viable emergency fund The conventional advice is to build three to six months of expenses as an emergency fund. For most people starting from scratch, that is an overwhelming target that can feel paralyzing. Do not start there. Start with one month of essential expenses. Rent, utilities, minimum debt payments, and basic groceries. That number is smaller and more achievable. And one month of runway is enough to absorb most common financial emergencies without missing credit payments. Once you have one month saved, you can begin directing more attention to credit building while continuing to grow the fund toward two and then three months over time. The one-month mark is the threshold that provides meaningful credit protection. Use a credit builder loan to save and build credit simultaneously This is one of the most elegant solutions to the save-and-build-credit challenge. A credit builder loan works by making fixed monthly payments into a locked savings account. The lender reports those payments to the credit bureaus while you build savings. At the end of the loan term you receive the accumulated balance back minus fees. Every dollar you put into a credit builder loan is simultaneously building your emergency fund and your credit history. At the end of a 12-month term on a modest loan, you have a year of positive payment history on your credit file and a lump sum of savings returned to you. That savings can then go directly into your emergency fund. The fixed monthly payment is also behaviorally useful. It automates the savings habit without requiring ongoing willpower decisions about whether to save this month. Report your rent to build credit without touching your savings One of the most powerful aspects of rent reporting is that it builds credit from payments you are already making. You are not redirecting money away from savings. You are not taking on new debt. You are simply getting credit recognition for a financial obligation you are already meeting. Credit Genius reports rent payments to Experian with backdating of up to 24 months. This means you can add significant positive payment history to your credit file without any change to your monthly budget. Every dollar of your income continues flowing toward savings or debt reduction while your credit file grows simultaneously. For someone trying to build both an emergency fund and good credit on a tight budget, rent reporting is the closest thing to a free credit-building move available. Use a secured credit card with a small deposit A secured credit card requires a deposit that becomes your credit limit. The deposit sits in your account, functioning similarly to a small emergency reserve while also enabling credit building. When you eventually close the card or graduate to an unsecured product, the deposit is returned to you. The key is to use the card for one or two small recurring purchases, like a streaming subscription or a gas fill-up, and pay the full balance every month. This builds payment history and keeps utilization low without adding any meaningful debt to your financial picture. Think of the deposit not as money spent but as money working double duty: it is securing your credit-building tool while remaining yours to reclaim. Automate both goals The most reliable way to build both an emergency fund and good credit simultaneously is to automate both so neither requires an active decision every month. Set up autopay for the minimum payment on every credit account. Set up an automatic transfer to your savings account on payday. Enroll in rent reporting so your monthly payment goes to the bureau without any action on your part. With these three automations in place, you are building your emergency fund and your credit profile every month without having to think about it. Automation removes the willpower requirement from both goals. And behavioral research is clear that habits sustained by automation are far more durable than those that depend on consistent conscious decisions. How to split your extra money between the two goals If you have extra money each month after covering essentials and minimum debt payments, a simple allocation framework is helpful. Until you have one month of essential expenses saved, direct 70% of extra money toward the emergency fund and 30% toward credit building activities like paying down high-utilization cards. Once you hit one month saved, shift to 50/50. Once you hit three months saved, you can direct more

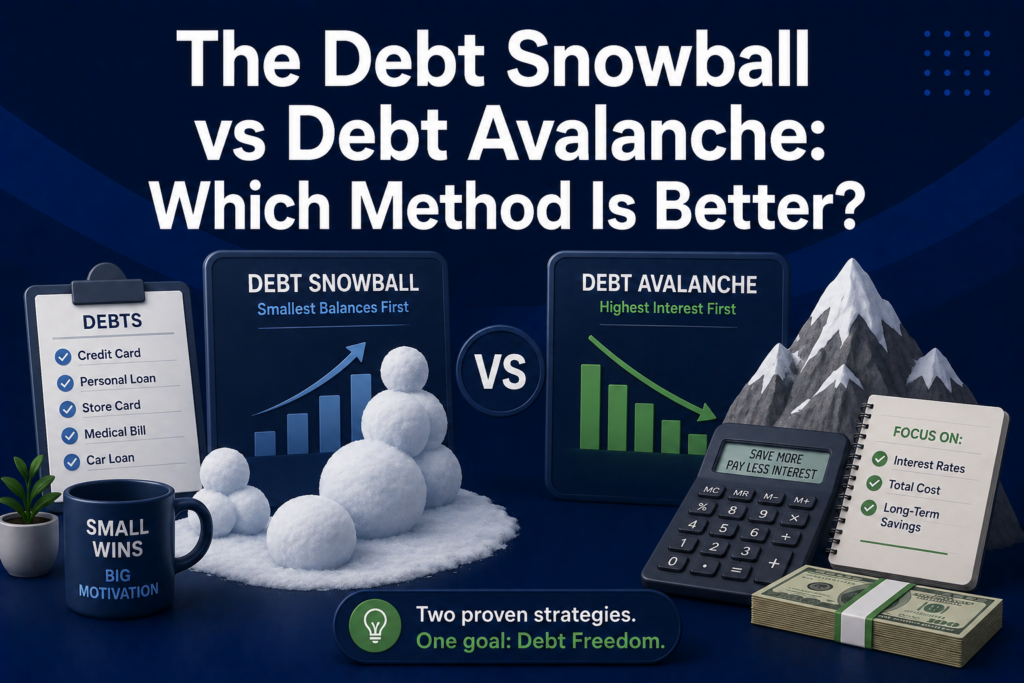

The Debt Snowball vs Debt Avalanche: Which Method Is Better?

If you are trying to pay off multiple debts, two methods come up more than any others: the debt snowball and the debt avalanche. Both work. Both have legitimate advantages. The debate between them has been going on for years and the honest answer is that the better one depends on who you are, not just what the math says. Here is a clear breakdown of how each method works, what the research says, and how to decide which one is right for your situation. How the debt snowball works The debt snowball method, popularized by personal finance commentator Dave Ramsey, works by paying off your smallest debt first regardless of interest rate. You make minimum payments on all your debts and put every extra dollar toward the smallest balance. When that debt is gone, you roll that payment amount onto the next smallest balance, and so on. The name comes from the momentum that builds as you eliminate accounts. Each payoff frees up more cash to attack the next debt, and the payments compound like a rolling snowball gaining size. Example: You have three debts. A 500 dollar medical bill, a 3,000 dollar credit card, and an 8,000 dollar car loan. Under the snowball method, you attack the 500 dollar bill first regardless of what interest rate any of them carry. How the debt avalanche works The debt avalanche method focuses on interest rates rather than balances. You make minimum payments on all your debts and put every extra dollar toward the debt with the highest interest rate. When that debt is paid off, you roll the payment to the next highest rate. The logic is straightforward: high-interest debt costs more money over time. Eliminating it first reduces the total interest you pay across all your debts. Example: Using the same three debts. If the 3,000 dollar credit card carries 24% interest, the 500 dollar medical bill carries 0%, and the car loan carries 7%, the avalanche method attacks the credit card first regardless of its balance being larger than the medical bill. What the math says The debt avalanche wins on math. Period. If you pay the same amount every month toward your debts, the avalanche method will cost you less money in total interest and get you debt-free faster in most scenarios. The higher the interest rates on your debts, the bigger the mathematical advantage of the avalanche. The difference can be significant. Depending on your debt mix and interest rates, the avalanche method can save hundreds or even thousands of dollars in interest compared to the snowball. What the research says about behavior Here is where it gets interesting. A study published in the Journal of Marketing Research found that people who focused on paying off individual accounts entirely, which aligns with the snowball approach, were more likely to eliminate their overall debt than those who spread payments based on balances or rates. The reason is psychological. Paying off a debt completely produces a sense of accomplishment that motivates continued effort. Mathematically optimal strategies do not help you if you abandon them three months in because the progress feels invisible. If you have tried to pay off debt before and given up, the snowball method’s quick wins may be more valuable to your long-term outcome than the avalanche’s mathematical efficiency. How each method affects your credit score Both methods improve your credit score over time by reducing your total debt. But they affect your score differently in the short term. Debt snowball and credit score: Paying off small balances quickly eliminates accounts, which can slightly affect your credit mix and account age. However, eliminating small balances also reduces overall utilization. If those small debts are revolving accounts like credit cards, paying them off reduces your utilization ratio and can produce noticeable score improvement quickly. Paying down high-interest revolving debt reduces utilization on those accounts, which can improve your score faster in many cases. If your highest-rate debt is a credit card with a high balance relative to its limit, the avalanche method can produce meaningful score improvement earlier than the snowball in some scenarios. For people who are building credit alongside paying off debt, the general principle is to prioritize paying down revolving credit card balances over installment debts when possible, since utilization is the second biggest factor in your credit score. Which method should you choose? Choose the debt snowball if: you have struggled to stay motivated with debt payoff in the past, you have several small debts that are making the situation feel overwhelming, you need quick wins to build momentum, or the interest rate differences between your debts are relatively small. Choose the debt avalanche if: you are highly motivated and confident you will stick with the plan regardless of early progress, you have significant high-interest debt where the math advantage is substantial, or you are focused on minimizing total interest paid over time. Consider a hybrid approach if: you have one or two very small debts you can eliminate quickly for a psychological win, then switch to the avalanche method for the remaining balances. This captures some motivational benefit of the snowball while shifting to the mathematically superior approach once momentum is established. What both methods have in common Regardless of which method you choose, the same fundamentals apply. Make minimum payments on all accounts every single month without exception. A missed payment damages your credit score far more than any debt payoff method can help it. Set up autopay on minimums so this never happens accidentally. And while you are paying off debt, continue building positive credit history where possible. If you are renting and your payments are not being reported to the credit bureaus, adding rent reporting through Credit Genius runs in parallel with your debt payoff without requiring any additional money. It adds positive data to your Experian file while you work through your debt, so your credit profile is stronger on the other side. The bottom line The

Is It Better to Pay Off Debt or Save Money First?

This is one of the most searched personal finance questions and one of the most genuinely nuanced ones. The honest answer is that it depends on the type of debt, the interest rate, your savings situation, and where your credit score is right now. Anyone who gives you a simple universal answer is leaving out important context. Here is how to think through it for your specific situation, including how your decision affects your credit score. The case for paying off debt first From a pure math perspective, paying off high-interest debt is almost always the better financial move. If you are carrying credit card debt at 22% interest and your savings account earns 5%, every dollar you put into savings is costing you 17 cents in net interest every year. The debt is growing faster than the savings. Paying off revolving debt like credit cards also directly improves your credit score by reducing your credit utilization ratio, the second most important factor in your FICO score at 30% of the total. If you have a card with a 5,000 dollar limit and a 4,000 dollar balance, your utilization on that card is 80%. Paying it down to 1,000 drops utilization to 20% and will likely produce a noticeable score improvement at your next statement close date. The credit score benefit of paying down revolving debt is one of the fastest credit improvements available to anyone who is carrying balances. It is measurable, it happens quickly, and it does not require opening any new accounts. The case for saving first The math of paying down high-interest debt is compelling, but math is not the only variable. Life is unpredictable. If you put every spare dollar toward debt and then face an unexpected car repair, medical bill, or job disruption, you have two choices: go back into debt at high interest rates or miss payments. Either outcome hurts your credit and your finances. This is why most financial guidance suggests building a small emergency fund before aggressively paying down debt. The standard recommendation is one to three months of essential expenses. This reserve protects your payment history, the most important factor in your credit score, from being disrupted by unexpected events. Missing a payment on a credit card because you used all your cash for debt payoff is a worse outcome than carrying a balance for a few more months while you build a buffer. Payment history is 35% of your FICO score. Protecting it matters more than optimizing the math on your debt paydown in most circumstances. The type of debt matters enormously High-interest revolving debt (credit cards at 15% or above): Pay this down aggressively after building a small emergency fund. The interest cost is high, the credit score benefit of reducing utilization is significant, and there is no good reason to carry these balances longer than necessary. Moderate interest installment debt (car loans, personal loans at 6 to 12%): Make your scheduled payments on time. Paying these off early has a smaller credit benefit than paying down revolving debt and the interest cost is more manageable. Directing extra cash to an emergency fund or high-interest debt paydown is usually the better move. Low interest debt (student loans, mortgages at 3 to 6%): Make scheduled payments and do not rush to pay these off at the expense of savings or investing. The interest cost is low and the credit benefit of paying them off early is minimal. Money directed toward savings or investments may generate better returns over time. How this connects to your credit score The debt-versus-savings decision intersects with your credit score in three specific ways. Utilization. Paying down credit card balances reduces your utilization ratio and improves your score. This is the most direct credit benefit of debt paydown and it shows up quickly, often within one to two billing cycles. Payment history protection. Maintaining a savings buffer protects your ability to make all minimum payments on time, preserving your payment history. A missed payment can cost 50 to 100 points and stays on your report for seven years. A few months of emergency savings prevents that outcome. Paying off and closing an installment loan can slightly reduce your credit mix, which accounts for 10% of your score. This is a minor factor but worth knowing if you are close to a score threshold for a major loan application. The practical framework Here is a simple decision framework that works for most situations. Build one month of essential expenses as an emergency fund before doing anything aggressive with debt. This protects your payment history from unexpected disruptions. Step two: Pay the minimum on all accounts on time, every month, without exception. This is non-negotiable regardless of what else you are doing. Step three: Direct any extra money toward high-interest revolving debt, starting with the highest rate or the account closest to its limit. This produces the fastest credit score improvement and the highest interest savings simultaneously. Step four: Once high-interest debt is cleared, build your emergency fund to three months of expenses before aggressively paying down lower-interest installment debt. Step five: Continue building credit in parallel. If you are renting and your rent is not being reported to the credit bureaus, adding rent reporting through a service like Credit Genius runs alongside this process without requiring you to redirect any debt paydown money. The bottom line The question of whether to pay off debt or save first does not have a single right answer. But for most people carrying high-interest revolving debt with little savings, the order is: small emergency fund first, then aggressive debt paydown, then savings expansion. The credit score implications reinforce this order. High-interest debt paydown reduces utilization and improves your score. A small emergency fund protects your payment history from disruption. Both outcomes serve your credit and your financial health simultaneously.The worst financial decision is not choosing one over the other. It is ignoring both because the question feels too complicated