Does Owing the IRS Affect Your Credit Score?

Tax season leaves a lot of people with an unexpected bill from the IRS. Whether it is a few hundred dollars or several thousand, owing the IRS is stressful on its own. The worry that it might also damage your credit score adds another layer of concern. The short answer is more nuanced than most people expect. Here is exactly how IRS debt interacts with your credit score, what has changed in recent years, and what you should do if you owe. Does simply owing the IRS hurt your credit score? No. Owing money to the IRS does not automatically appear on your credit report or affect your credit score. The IRS does not report tax debts to the credit bureaus the way that lenders and creditors do. Simply having an unpaid tax balance, even a large one, does not create a negative entry on your credit file. This surprises many people who assume that any significant debt to a government agency would show up on their credit report. Tax debt is treated differently from consumer debt in the credit reporting system. What about tax liens? This is where it used to get complicated. Historically, the biggest credit concern around IRS debt was the federal tax lien. When a taxpayer failed to pay a significant tax debt after the IRS made a formal demand for payment, the IRS could file a Notice of Federal Tax Lien, which was a public record claiming the government’s interest in your assets. These liens used to appear on credit reports and could significantly damage credit scores. That changed significantly in 2017. In April of that year, Equifax, Experian, and TransUnion announced that they would no longer include tax liens on consumer credit reports as part of a broader initiative to improve the accuracy of credit reporting. This change went into effect in July 2017. As a result, federal tax liens no longer appear on consumer credit reports from the three major bureaus. If you had a tax lien on your credit report before 2017 it should have been removed. If a tax lien is currently appearing on your report from any of the three major bureaus, it is likely an error and should be disputed. Can IRS debt ever affect your credit? There are indirect ways that unresolved IRS debt can create credit complications, even without appearing directly on your credit report. Even though tax liens no longer appear on consumer credit reports, a federal tax lien is still a public record that affects your ability to sell property or refinance a mortgage. Title searches conducted during real estate transactions will reveal existing tax liens, which must typically be resolved before closing. If the IRS escalates collection efforts, it can levy your bank accounts or garnish your wages. A bank account levy that drains funds you were using to pay other obligations can lead to missed payments on credit accounts, which would damage your credit score. The IRS debt itself does not appear on your credit report but the consequences of unresolved IRS debt can cascade into credit-damaging events. For very large tax debts, the IRS can certify the debt to the State Department, which can deny passport applications or revoke existing passports. This does not affect credit directly but it is a significant consequence of large unresolved tax debt. What to do if you owe the IRS The good news is that the IRS offers several options for taxpayers who cannot pay their full balance immediately, and engaging with these options prevents the escalation that can lead to indirect credit damage. Installment agreement. You can set up a payment plan with the IRS to pay your balance over time. If you owe less than 50,000 dollars and have filed all required returns, you can often set up an online payment plan without speaking to an IRS agent. Installment agreements are not reported to credit bureaus and do not affect your credit score. Offer in Compromise. If you cannot pay the full amount owed and it would create financial hardship, you may qualify for an Offer in Compromise, which allows you to settle your tax debt for less than the full amount. Qualification depends on your income, expenses, and asset equity. Currently Not Collectible status. If paying your tax debt would prevent you from covering basic living expenses, the IRS can place your account in Currently Not Collectible status, temporarily suspending collection activity. Interest and penalties continue to accrue but active collection stops. The worst approach to IRS debt is ignoring it. Ignoring it leads to escalating penalties, interest, and eventually the levies and liens that can create indirect credit damage even if they no longer appear directly on credit reports. Protect your credit while resolving IRS debt While working through an IRS debt situation, protect your credit score by maintaining all other payment obligations. Set up autopay on all credit accounts so that the stress and distraction of dealing with the IRS does not result in missed payments elsewhere. Monitor your credit file during this period as well. Real-time monitoring through a tool like Credit Genius alerts you immediately if anything unexpected appears on your Experian file, giving you the earliest possible warning if any IRS-related record shows up or if another issue emerges while your attention is elsewhere. The bottom line Owing the IRS does not directly damage your credit score. Tax liens were removed from consumer credit reports in 2017 and the IRS does not report tax debts to the credit bureaus. However, ignoring a tax debt can lead to IRS collection actions that create indirect credit damage through missed payments or bank levies. The practical advice is straightforward: engage with the IRS, set up a payment plan if you cannot pay in full, and protect your credit obligations while you work through it. The IRS is one of the more accommodating creditors when it comes to payment arrangements. Use that to your advantage.

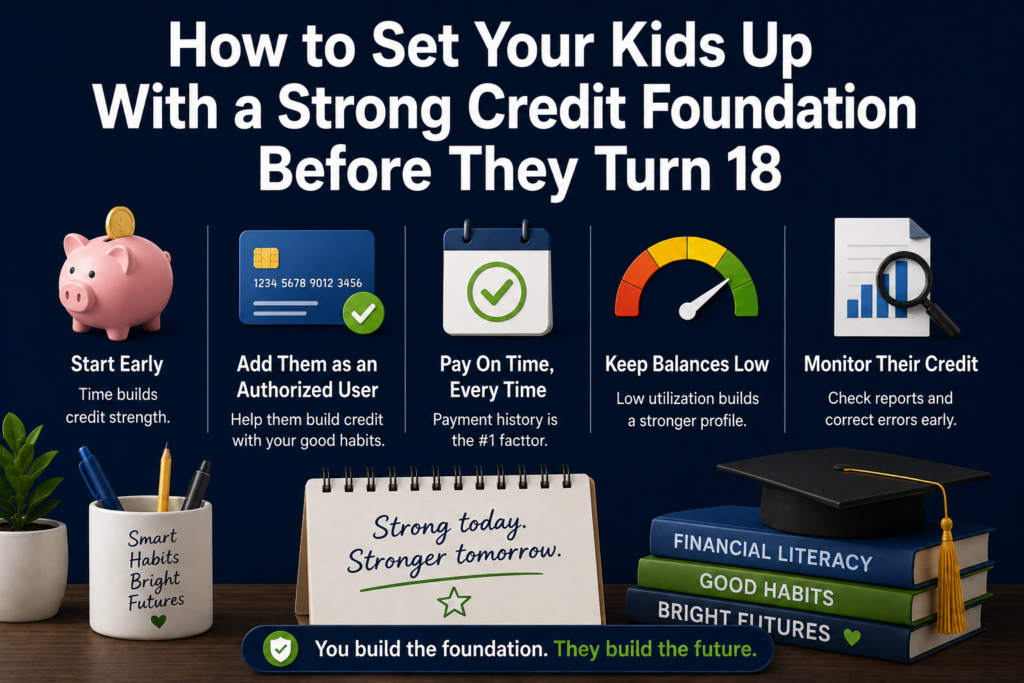

How to Set Your Kids Up With a Strong Credit Foundation Before They Turn 18

Most Americans turn 18 with no credit history whatsoever. They enter adulthood invisible to the credit system, which means their first apartment application, first car loan, and first major financial decision are all made at a disadvantage. It does not have to work that way. Parents who understand how credit works can give their children a meaningful head start by taking a few deliberate steps before their kids reach adulthood. Here is what you can do and when. Why starting before 18 matters Credit scoring rewards length of history. The longer a positive account has been open, the more value it adds to a credit profile. A child added as an authorized user on a parent’s credit card at age 13 has five years of established credit history by the time they turn 18. A young adult who opens their first account at 18 starts from zero. That five-year difference in account age matters when an 18-year-old applies for their first apartment or a 21-year-old applies for a car loan. The person with five years of established history in good standing is in a fundamentally different position than the person with six months. Add your child as an authorized user This is the most powerful credit-building tool available to parents for their children. When you add a child as an authorized user on your credit card, your payment history and account age on that card can appear on their credit report. You do not need to give your child the physical card or allow them to use it. The credit benefit comes from the account appearing on their report, not from their usage. Many parents add a child as an authorized user, keep the card, and never let the child use it. The child still receives the credit history benefit. The account you choose matters. Add your child to an account with a long history, a clean payment record, and low utilization. If your oldest card has a few late payments on it, consider whether a newer card with a cleaner record might be the better choice to put on your child’s report. Different card issuers have different policies on authorized user age minimums. Some allow authorized users as young as 13. Others require 15 or 16. Check your card issuer’s policy before adding your child. Freeze your child’s credit file Children’s credit files are attractive targets for identity thieves because the fraud often goes undetected for years. A child whose Social Security Number is used to open fraudulent accounts may not discover the damage until they apply for their first credit card at 18 or their first apartment at 21. Parents can place a credit freeze on their child’s file at all three bureaus. This prevents any new accounts from being opened in the child’s name. The freeze costs nothing and can be lifted when the child is ready to start using their credit. The process requires submitting documentation proving your identity and your relationship to the child, including a birth certificate and your own ID. It takes a bit more effort than freezing an adult file but the protection is significant. Teach the fundamentals before they need them A credit foundation is most valuable when paired with understanding. A teenager who becomes an authorized user on your card but does not understand what credit is, how scores work, or why payment history matters is less equipped to manage credit independently than one who understands the system. Walk your child through how credit scores are calculated. Explain what payment history is and why missing a payment is such a significant event. Show them what a credit report looks like. Explain what utilization means and why carrying high balances hurts your score even if you eventually pay them off. Financial education tools like the Credit Games feature inside Credit Genius can make this more engaging for teenagers who find the subject dry when explained as a lecture. Gamified financial education builds knowledge retention in a way that passive content consumption typically does not. When your child turns 16 to 18: prepare for independence In the two years before your child turns 18, start preparing them to manage credit independently. Pull their credit report to see what is on it, confirm the authorized user account is reporting correctly, and check for any unexpected entries. If you want your teenager to have their own credit account before 18, some credit card issuers offer student cards to 17-year-olds with a parent co-signer. A secured card with a small deposit is another option for older teenagers who are demonstrating financial responsibility. Have a direct conversation about the plan for when they turn 18. Will they keep the authorized user account? Will you remove them? Will they open their own card? Knowing the plan in advance prevents the scenario where a newly independent adult is suddenly starting from scratch with their credit because the authorized user account was closed. What not to do Do not add your child to an account with a poor payment history or high utilization. The negative information transfers along with the positive. A card with a few missed payments in its history can hurt your child’s credit file rather than help it. Do not give a teenager unrestricted access to a credit card before they understand how it works. The goal is to build a credit foundation, not to create an opportunity for spending that damages the very file you are trying to build. Do not neglect the freeze. A child’s Social Security Number is a valuable identity theft target. Placing a freeze on their credit file is one of the most protective actions a parent can take. The bottom line The credit foundation you build for your child before they turn 18 is one of the most practical financial gifts you can give them. Adding them as an authorized user on a well-managed account, freezing their credit file to protect against identity theft, and teaching them how credit

What Is Credit Seasoning and Why Do Lenders Care?

If you have ever applied for a mortgage or a significant loan and been told your credit history is too new or that you need more seasoned accounts, you have encountered the concept of credit seasoning without necessarily being told what it means. It is a term used by lenders and credit professionals that most consumers have never heard, yet it affects loan approvals and interest rates in real ways. Here is a clear explanation of what credit seasoning is, why lenders care about it, and what you can do to build it. What credit seasoning means Credit seasoning refers to the age and established history of credit accounts on your credit report. A seasoned account is one that has been open for a meaningful period of time, typically at least twelve to twenty-four months, and has a demonstrated track record of on-time payments during that period. The term comes from the idea that like seasoned wood or seasoned cast iron, a credit account becomes more valuable with age and use. A brand new account tells a lender very little about how you will manage it long-term. An account with three years of consistent payment history tells a much more complete story. Credit seasoning applies to individual accounts as well as to your credit file overall. A lender might look at the age of your oldest account, your newest account, and the average age of all accounts when evaluating your application. Why lenders care about seasoning Lenders use credit history as a predictor of future behavior. The core question they are trying to answer is: based on what this person has done with credit in the past, how likely are they to repay this loan on time? A credit file full of new accounts opened in the last six months provides limited predictive information. The accounts have not had time to demonstrate how they will be managed through different financial circumstances. A credit file with accounts that have been consistently managed for three, five, or ten years provides much stronger evidence of reliable credit behavior. This is particularly true for mortgage lending. Mortgage lenders are evaluating your ability to make consistent payments over fifteen or thirty years. They want to see evidence that you have managed credit responsibly over a meaningful period, not just that you opened several accounts recently. How seasoning affects your credit score Length of credit history accounts for 15% of your FICO score. This factor includes the age of your oldest account, the age of your newest account, and the average age of all accounts. The longer these ages, the better this factor contributes to your score. This is why opening multiple new accounts in a short period can temporarily lower your score. Each new account is unseasoned, it pulls down your average account age and your newest account age. The impact is temporary because the accounts gain age over time, but it is real in the short term. It is also why closing old accounts is generally a bad idea from a credit perspective. A ten-year-old account that you close removes valuable seasoning from your file. Even if you stop using the card, keeping it open preserves that account age. Minimum seasoning requirements in mortgage lending Mortgage lenders often have explicit seasoning requirements that go beyond credit score thresholds. These are minimum periods of time that must have passed since certain credit events before an applicant can qualify. After bankruptcy: Most conventional loan programs require two to four years of seasoning after a Chapter 7 bankruptcy discharge before an applicant qualifies. FHA loans require two years. VA loans may be as short as two years depending on the lender. After foreclosure: Conventional loans typically require seven years of seasoning after a foreclosure. FHA loans require three years. VA loans require two years. After short sale: Conventional loans generally require four years of seasoning after a short sale. FHA loans require three years. These waiting periods exist because lenders want to see evidence of financial rehabilitation after a serious credit event before extending a large, long-term loan. How to build seasoning faster The frustrating reality of credit seasoning is that time is the primary variable. You cannot manufacture seasoning the way you can reduce utilization or dispute errors. Accounts simply need to age. That said, there are strategies that help. Becoming an authorized user on a long-standing account with good history can add seasoning to your file immediately. If a family member adds you to an account they have had for eight years, that account’s history can appear on your report and contribute to your average account age. Rent reporting with backdating is another way to add historical payment data to your file quickly. When Credit Genius reports rent payment history to Experian with backdating of up to 24 months, it adds two years of established payment history to your file. While this affects payment history rather than account age specifically, it contributes to the overall picture of an established, reliable credit profile that lenders associate with seasoning. Opening accounts earlier rather than later is the most fundamental strategy. Every month you delay starting to build credit is a month of seasoning you cannot recover. For young people especially, opening a first credit account at 18 or 19 rather than 25 means six or seven additional years of credit history by the time major financial decisions arrive. What not to do Do not close old accounts in an attempt to simplify your credit profile. Closing old accounts removes seasoning from your file and reduces your available credit. Both outcomes are negative. Do not open multiple new accounts in a short period if you are approaching a major loan application. New accounts signal unseasoned credit and temporarily lower your average account age. Do not confuse credit score with credit seasoning. A person can have a credit score in the 700s but still face seasoning-related questions from mortgage lenders if their accounts are all relatively new. Score

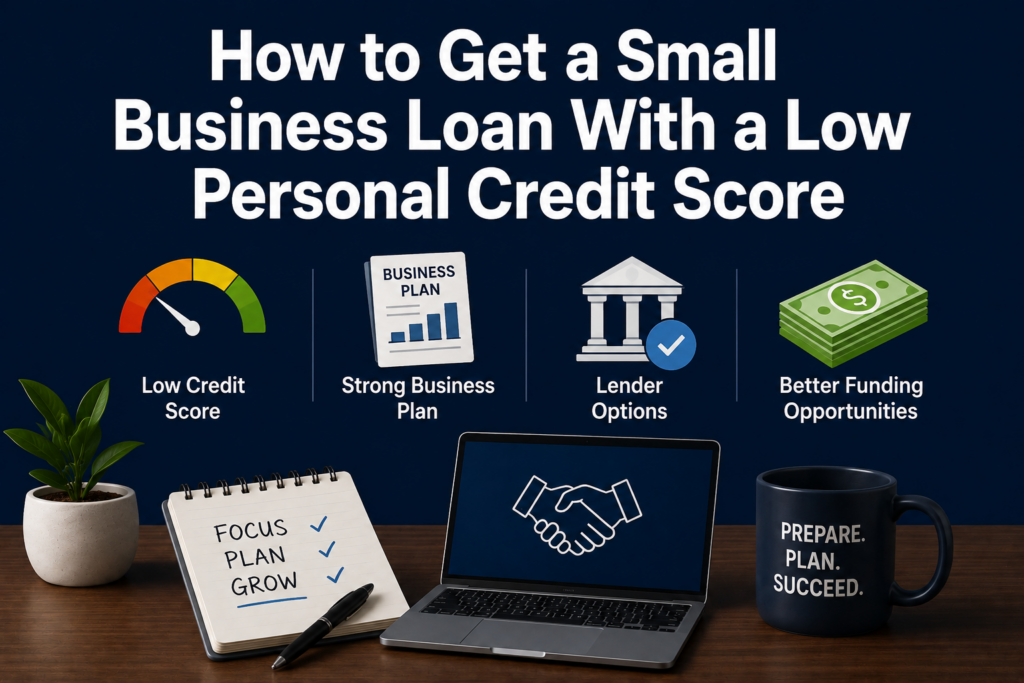

How to Get a Small Business Loan With a Low Personal Credit Score

Starting or growing a business with a low personal credit score is genuinely harder than doing it with good credit. Most small business lenders, particularly traditional banks, rely heavily on the owner’s personal credit score when evaluating a loan application, especially for newer businesses that do not yet have an established business credit profile. But low personal credit does not make small business financing impossible. It changes which options are available, what they cost, and what documentation you need to make a compelling case. Here is a practical guide to navigating small business lending with a low personal credit score. Why personal credit matters for business loans Most small business lenders, particularly banks and SBA-backed lenders, check the owner’s personal credit score as part of the application process. For businesses with less than two to three years of operating history, the owner’s personal credit is often the primary indicator of financial reliability because the business itself does not have a long enough track record to evaluate independently. Traditional bank loans and SBA 7a loans typically require a personal credit score of 680 or above. Some lenders set the bar at 700 or higher. Below those thresholds, the application becomes significantly harder and the available options shift toward alternative lenders who accept lower scores but charge higher rates. Know your minimum score requirements by loan type The SBA does not set a minimum credit score requirement but most SBA-approved lenders require at least 650 to 680. The SBA microloan program, which offers loans up to 50,000 dollars through nonprofit intermediary lenders, generally has more flexible credit requirements and is worth exploring for smaller funding needs. Online business lenders: Alternative online lenders like Kabbage, OnDeck, and Fundbox have lower minimum credit score requirements, sometimes accepting scores as low as 500 to 550. The tradeoff is significantly higher interest rates and shorter repayment terms. These are viable for short-term needs but expensive for long-term financing. Nonprofit lenders and Community Development Financial Institutions, known as CDFIs, offer microloans specifically designed for underserved business owners including those with limited or poor credit history. Accion Opportunity Fund, Kiva US, and local CDFI networks are worth researching. These lenders often look at the full picture of your business rather than relying primarily on credit score. Equipment financing: If you need funding specifically to purchase equipment, equipment financing uses the equipment itself as collateral, which reduces the lender’s reliance on your personal credit score. Approval requirements can be more flexible than for unsecured business loans. If your business has outstanding invoices from clients, invoice financing allows you to borrow against those receivables. The creditworthiness of your clients matters more than your personal score in many of these arrangements. Strengthen your application beyond the credit score A low personal credit score makes the application harder. A strong application in every other dimension can partially offset that disadvantage. Business revenue and cash flow. Strong business bank statements showing consistent revenue and healthy cash flow are compelling evidence of creditworthiness that your personal score cannot provide. Many alternative lenders weight revenue-based metrics heavily alongside or even above personal credit. Time in business. The longer your business has been operating successfully, the more evidence you have of its viability. Even two years of solid operating history can significantly improve your chances with many lenders. Collateral. Offering collateral, whether business assets, equipment, or in some cases personal assets, reduces the lender’s risk and can overcome credit score concerns. Secured loans are generally more accessible than unsecured ones for borrowers with lower scores. For newer businesses with limited revenue history, a detailed, credible business plan that demonstrates market understanding, realistic financial projections, and a clear repayment strategy can make a meaningful difference, particularly with CDFI and microloan lenders who evaluate applications more holistically. Build business credit separately Business credit, tracked by Dun and Bradstreet, Experian Business, and Equifax Business, is separate from personal credit. Building a business credit profile reduces your reliance on personal credit for future financing. Start by incorporating your business or forming an LLC, opening a dedicated business bank account, and getting an EIN from the IRS. Then open trade credit accounts with suppliers who report to business credit bureaus. Net-30 accounts with vendors who report payment history are a common starting point. A business credit profile with even six to twelve months of positive payment history makes future lending conversations significantly easier and reduces the weight placed on your personal score. Work on your personal credit in parallel If your personal credit score is genuinely a barrier to the financing you need, improving it should be a parallel priority alongside running your business. The most impactful short-term actions are paying down credit card balances to reduce utilization, disputing any errors on your credit report, and ensuring all payments are made on time going forward. If you are renting your home or business space, rent reporting through Credit Genius adds positive payment history to your Experian file without requiring any new debt or significant time investment. Every point gained on your personal score opens more business financing options at better rates. The bottom line A low personal credit score narrows your small business lending options and increases your cost of capital. It does not eliminate your options entirely. Alternative lenders, microloans, CDFIs, equipment financing, and invoice financing all offer paths to business capital with lower credit requirements.The best strategy combines pursuing the financing options available to you now with actively improving your personal credit and building a business credit profile in parallel. Better credit means better options and lower costs for every future financing need your business has.

How to Rebuild Credit After a Natural Disaster

Natural disasters upend everything simultaneously. Housing, employment, transportation, access to basic services, and the financial systems people depend on for daily life can all be disrupted at once. In the chaos of rebuilding a life after a hurricane, wildfire, flood, or tornado, credit is often the last thing on anyone’s mind. But the credit damage that can accumulate during and after a disaster is real, and it can make the financial recovery significantly harder. Understanding your options, your rights, and the steps available to you is an important part of the full recovery process. How disasters damage credit Natural disasters damage credit through a chain of financial disruptions rather than a single event. Income is disrupted when businesses are destroyed or employees cannot get to work. Housing costs spike when people are displaced and need temporary accommodation on top of ongoing rent or mortgage obligations. Insurance reimbursements take time while immediate costs arrive immediately. Banks and payment systems may be inaccessible in affected areas. The result is that people who were managing their finances responsibly before the disaster find themselves unable to make payments they would normally make without difficulty. Missed payments, high utilization from emergency expenses charged to credit cards, and potential collections from bills that fell through the cracks during displacement are all common outcomes. Contact your lenders immediately This is the most important step and the one most people skip because they are overwhelmed. Contact every lender you have, credit cards, auto loans, mortgage or rent, utilities, and any other financial obligation, and explain that you have been affected by a declared disaster. Most major lenders have disaster relief programs that can defer payments, waive late fees, and suspend negative reporting to the credit bureaus for a defined period. These programs exist specifically for situations like this. They are not guaranteed and not every lender participates but many do, and the relief can be substantial. The key is to call before you miss a payment if possible. Lenders are more accommodating when you reach out proactively than when you have already missed several payments and the account is in collections. Know your rights under FCRA disaster provisions The Fair Credit Reporting Act contains provisions relevant to natural disasters. If you notify a credit bureau that you have been affected by a natural disaster and your address is in a federally declared disaster area, the bureau is required to flag your file. This notation can affect how lenders and others interpret negative marks that appear during the disaster period. Additionally, if a lender agrees to defer payments or modify your account terms during the disaster period, they are generally required to report your account status accurately, meaning a deferred payment should not be reported as a missed payment if the deferral was formally agreed. Document every agreement you make with lenders in writing. If you call and agree to a three-month payment deferral, follow up with an email confirming the terms. This documentation protects you if the account is later reported incorrectly. Check FEMA and government assistance programs Federal Emergency Management Agency assistance, SBA disaster loans, and state-level programs can provide financial support that reduces the need to rely on credit during a disaster recovery period. FEMA assistance for declared disasters can cover temporary housing, home repair, and other essential needs. SBA disaster loans are available to homeowners, renters, and businesses in declared disaster areas at low interest rates. For credit rebuilding purposes, an SBA disaster loan that helps you stabilize your financial situation can prevent the credit damage that would otherwise accumulate from missed payments and emergency credit card charges. Register with FEMA at disasterassistance.gov as early as possible after a declared disaster. Deadlines for assistance applications are real and missing them can mean losing access to programs that would have helped. Pull your credit reports and dispute disaster-related errors Once the immediate crisis has stabilized, pull your credit reports from all three bureaus at annualcreditreport.com and review them carefully. Look specifically for accounts that show missed payments during the disaster period that should have been covered by a deferral agreement, accounts that were sent to collections despite a hardship arrangement, and any other entries that do not accurately reflect what actually happened. If you find errors, dispute them with documentation. Your written agreements with lenders are your evidence. A lender who agreed to defer payments and then reported them as missed has made an error that can and should be disputed. Start rebuilding systematically Once the emergency phase is over and you have a stable housing and income situation, begin rebuilding your credit profile deliberately. Set up autopay on all accounts that are current so that as your life normalizes, your payment history is automatically protected. If you are renting in your recovery location, enroll in rent reporting through Credit Genius. Adding verified rent payment history to your Experian file creates positive data that begins to counterbalance any negative marks from the disaster period. If you had to open new credit accounts during the disaster, manage them carefully. Emergency credit card balances should be paid down as insurance reimbursements and assistance arrive to reduce utilization. The timeline for recovery The credit recovery timeline after a natural disaster depends heavily on how much damage accumulated during the event and how quickly you were able to contact lenders and access assistance. For someone who caught the situation early, contacted lenders immediately, and secured deferral agreements, the credit damage may be minimal and recovery relatively quick. For someone whose credit took significant hits through missed payments and collections during an extended displacement, the recovery timeline is similar to other credit rebuilding scenarios: twelve to twenty-four months of consistent positive behavior to meaningfully improve a damaged score, with the most severe marks fading over time even as they remain on the report for up to seven years. The bottom line Credit damage after a natural disaster is real but it is also one of the most preventable forms of

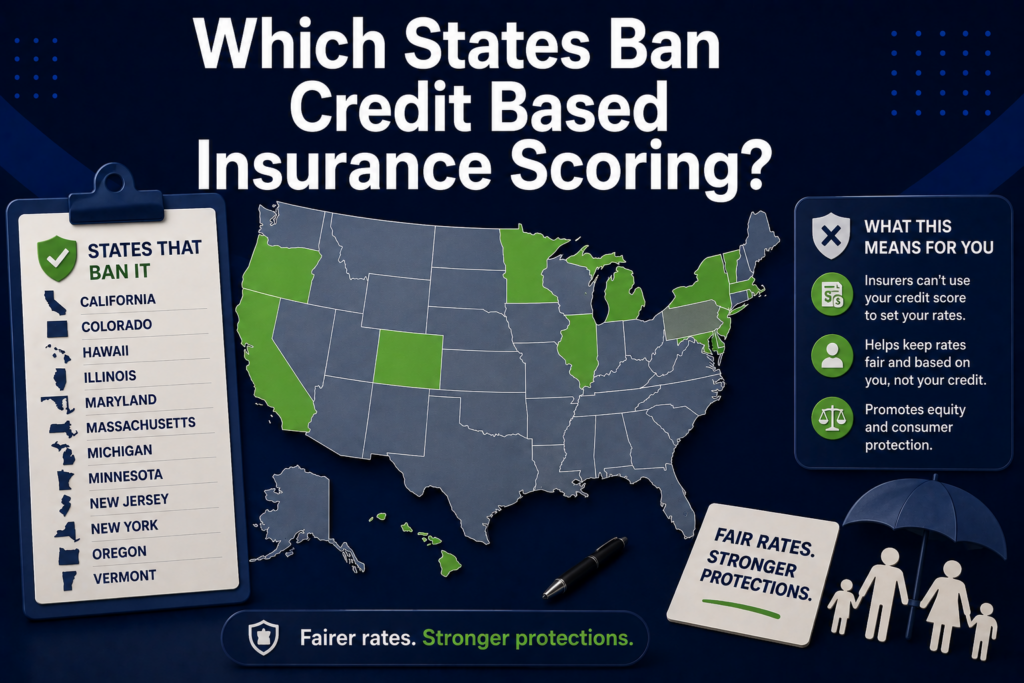

Which States Ban Credit Based Insurance Scoring?

Most Americans do not know that their credit score affects how much they pay for car insurance. In the majority of US states, insurance companies use a credit-based insurance score, which is derived from credit report data, to help set premiums. Drivers with lower credit scores often pay significantly more for the same coverage than drivers with excellent credit, regardless of their actual driving record. But not everywhere. A handful of states have banned or significantly restricted the use of credit in insurance pricing. Here is what you need to know about which states those are, why the practice exists, and what it means for your wallet. What is credit based insurance scoring? A credit-based insurance score is not the same as your FICO credit score. It is a separate score calculated from similar credit report data, including payment history, outstanding debt, credit history length, and types of credit, but weighted differently to predict the likelihood of filing an insurance claim rather than defaulting on a loan. Insurance companies and researchers have found a statistical correlation between credit behavior and insurance claim frequency. People with lower credit-based insurance scores file more claims on average than people with higher scores. Insurers use this correlation to price risk, resulting in higher premiums for policyholders with poor credit even if they have never filed a claim. Critics argue that this correlation reflects socioeconomic factors rather than individual risk, and that using credit data in insurance pricing disproportionately harms lower-income communities and communities of color who tend to have lower credit scores for structural reasons unrelated to their actual insurance risk. States that ban credit based insurance scoring Three states currently ban the use of credit information in auto insurance pricing entirely: California, Hawaii, and Massachusetts. These states prohibit insurers from using credit scores or credit-based insurance scores as a factor in setting premiums, determining eligibility, or renewing policies. In these states, your credit score has no bearing on your auto insurance premium. Rates are set based on other factors including driving record, vehicle type, age, location, and annual mileage. Michigan also has restrictions on the use of credit in insurance pricing, though the rules are more nuanced and have evolved through legislative changes in recent years. For homeowners insurance, the picture is similar. California, Maryland, and a few other states have restrictions or bans on using credit in homeowners insurance pricing, though the specifics vary by state and by the type of restriction in place. What about the other 47 states? In the majority of US states, credit-based insurance scoring is permitted and widely used. The financial impact can be significant. According to research by the Consumer Federation of America, drivers with poor credit can pay 50 to 100% more for auto insurance than drivers with excellent credit for identical coverage in the same location. On a 1,500 dollar annual auto insurance premium, that represents an additional 750 to 1,500 dollars per year purely from the credit score factor. Over five years, that is 3,750 to 7,500 dollars in additional premium costs attributable to credit alone. The impact on homeowners insurance varies by insurer and state but can also be significant. Some studies have found premium differences of 20 to 50% or more between policyholders with excellent and poor credit in states where credit scoring is permitted. Legislative trends The COVID-19 pandemic sparked renewed scrutiny of credit-based insurance scoring after research showed that communities hardest hit economically by the pandemic, many of which were communities of color, would face insurance premium increases tied to credit score declines caused by the pandemic rather than by any change in their actual risk profile. Several states considered or passed temporary restrictions on using pandemic-related credit changes in insurance pricing. The broader debate over whether credit-based insurance scoring should be restricted or banned entirely has continued in state legislatures across the country, with consumer advocates pushing for expansion of the California, Hawaii, and Massachusetts model. The regulatory landscape in this area is evolving. Consumers in states currently permitting credit-based insurance scoring should monitor legislative developments that could affect their premiums. What you can do if you live in a state that allows credit based insurance scoring The most direct action available is improving your credit score, which improves your credit-based insurance score along with it. The same behaviors that build a strong FICO score, paying on time, keeping utilization low, and maintaining a clean credit history, also improve the credit-based insurance score insurers use. When your credit score improves meaningfully, ask your insurer to re-run your credit-based insurance score. Many insurers will do this at renewal or upon request. A significant improvement in your credit profile can result in a lower premium without changing your coverage. Shopping your insurance policy when your credit has improved is also worthwhile. Different insurers weight credit differently in their scoring models. Getting quotes from multiple insurers after a credit improvement can surface premium differences of hundreds of dollars per year. Tools like Credit Genius that provide real-time Experian monitoring and personalized guidance on the actions most likely to improve your score help you work toward the credit improvements that reduce costs across multiple financial products simultaneously, including insurance premiums in states where credit scoring is permitted. The bottom line Credit-based insurance scoring is banned in California, Hawaii, and Massachusetts for auto insurance and restricted in a few additional states. In the remaining states, your credit score affects what you pay for insurance and the financial impact can be substantial. If you live in a state where credit scoring is permitted, improving your credit score reduces your insurance costs alongside every other financial benefit a stronger score provides. The insurance premium reduction is one more reason why credit building pays off in real, measurable dollars.

How to Build Credit as a Single Parent on One Income

Single parents manage one of the most financially demanding situations in American life. One income covering housing, childcare, groceries, healthcare, transportation, and everything else a family needs. The margin for error is small and the competing demands on every dollar are relentless. Building credit in this environment is not impossible but it requires a different approach than the generic advice written for people with more financial breathing room. Here is a practical, honest guide to building credit when you are doing it all on one income. Why credit matters more for single parents For single parents, a strong credit score is not just a financial metric. It is a practical tool that determines the quality of housing you can access, the cost of the car loan you need to get to work, the insurance premiums you pay, and your ability to access emergency credit when something goes wrong and there is no second income to fall back on. A weak credit profile in a single-income household means higher costs across every major financial category at exactly the moment when keeping costs down matters most. The return on investing time and attention in your credit is higher for single parents than for almost any other demographic. Protect payment history above everything else Payment history is 35% of your FICO score and the most important factor. For a single parent managing multiple financial obligations on one income, protecting this factor is the highest priority credit action available. Set up autopay for the minimum payment on every credit account right now. The minimum is enough to protect your payment history even if you cannot pay the full balance. A missed payment from a month when childcare costs spiked or a medical bill arrived unexpectedly stays on your report for seven years. Autopay prevents that outcome automatically. If you are facing a month where you genuinely cannot make a minimum payment, call the lender before the due date. Many have hardship programs that can defer or reduce a payment temporarily without reporting a negative event to the bureaus. The key is to call before you miss, not after. Report your rent Most single parents are renters. That monthly rent payment is almost certainly the largest financial commitment you make every month and it is not helping your credit unless someone is reporting it. Most landlords do not. Rent reporting services submit your payment history to credit bureaus. Credit Genius reports to Experian with backdating of up to 24 months, meaning months of on-time payments you have already made can be added to your credit file at once. For a single parent with a thin or fair credit file, this is one of the most impactful credit moves available because it requires no new debt, no new accounts, and no change to your monthly budget. Build a small emergency fund specifically for credit protection Single-income households are more vulnerable to financial shocks than two-income households. A sick child, a car breakdown, or an unexpected expense that a two-income household absorbs without crisis can destabilize a single-income budget completely. Build a dedicated credit protection reserve, separate from your general emergency fund, that covers minimum payments on all credit accounts for two to three months. This specific reserve ensures that even during a financial crisis your payment history, the most valuable credit asset you have, remains intact. Even 200 to 300 dollars set aside specifically for this purpose can be the difference between a credit score that survives a difficult month and one that takes a serious hit. Use a secured card strategically A secured credit card with a small deposit, even 200 dollars, used for one recurring purchase per month and paid in full each billing cycle, builds payment history and keeps utilization low without adding meaningful debt or financial risk. Choose a no-fee secured card so the only cost is the opportunity cost of the deposit. Use it for something predictable like a streaming subscription or a small monthly grocery run. Pay it in full before the statement closes. This single habit, maintained consistently, builds a meaningful credit track record over twelve to twenty-four months. Explore government and nonprofit assistance programs Single parents often qualify for assistance programs that can reduce financial pressure on the monthly budget, freeing up resources for credit building and emergency savings. SNAP, WIC, CHIP for children’s health coverage, childcare subsidy programs, and housing assistance all reduce fixed expenses that consume income. Reduced financial pressure directly benefits your credit because it lowers the likelihood of the missed payments and high utilization that damage scores. Accessing assistance you qualify for is not a compromise. It is a practical financial strategy. Monitor your credit file closely Single parents are more likely to be targeted by certain types of financial fraud and predatory offers. Identity theft in particular can cause serious credit damage that takes significant time and effort to resolve. Real-time credit monitoring through a tool like Credit Genius alerts you immediately when anything changes on your Experian file. Catching an unauthorized account or a fraudulent inquiry within days rather than months limits the damage and makes the dispute process simpler. Be realistic about the timeline Building credit as a single parent on one income is a slower process than it would be with two incomes and more financial flexibility. That is not a failure. It is a reflection of the reality you are working within. Consistent on-time payments over twelve to twenty-four months, combined with rent reporting and a secured card, will produce a meaningful and improving credit profile. The score may not move as fast as you want. But every month of on-time payments is a month of positive history that compounds over time. The bottom line Building credit as a single parent requires prioritizing the highest-impact, lowest-cost credit moves: protecting payment history through autopay, reporting rent through a service like Credit Genius, building a small credit protection reserve, and using a secured card consistently.The financial environment of single parenthood

How to Build Credit as a Seasonal Worker

Seasonal work is one of the most common employment patterns in the United States. Ski resort workers, agricultural workers, construction crews, retail holiday staff, summer tourism workers, tax preparers, and countless others work intensively for part of the year and differently or not at all for the rest. The credit system was built around a paycheck that arrives every two weeks, all year long. Seasonal workers do not fit that mold and the credit challenges that result are real. The good news is that seasonal workers can build strong credit. It requires more deliberate planning than it does for year-round employees but the path is clear. Here is how to do it. Understanding the seasonal worker credit challenge Your credit score itself is not affected by whether your income is seasonal. Employment status and income do not appear on your credit report. The score is calculated entirely from your credit behavior: payment history, utilization, account age, credit mix, and inquiries. The challenge shows up in two places. First, applying for credit products that require income documentation during the off-season when your income may be zero or minimal. Second, managing credit obligations through a period of reduced or no income without missing payments, which would damage your credit score. Both challenges are manageable with the right approach. Time your credit applications strategically The single most practical credit tip specific to seasonal workers is this: apply for credit products during your peak earning season, not during the off-season. When you apply for a credit card, personal loan, or other credit product that requires income documentation, apply while you are actively working and can show strong recent income. Lenders evaluate your income at the time of application. An application submitted in October by a resort worker earning 5,000 dollars a month through the ski season looks very different from the same application submitted in April when that person has minimal income. The credit score may be identical but the approval odds and the terms offered can differ significantly. Build your credit product portfolio during high-earning months. Avoid new applications during the off-season unless necessary. Build an off-season credit reserve The biggest credit risk for seasonal workers is missing payments during the off-season when income is low or absent. A missed payment is one of the most damaging credit events you can experience and it stays on your report for seven years. During your high-earning season, set aside enough money to cover minimum payments on all your credit accounts for the duration of your off-season. If you have a credit card with a 35 dollar minimum payment and a 25 dollar credit builder loan payment and your off-season runs six months, you need 360 dollars set aside specifically for those payments. This is a small amount relative to seasonal earnings but it provides complete protection for your payment history, which is the most important factor in your credit score, during the period when your income is most vulnerable. Set up autopay before the off-season starts Set up autopay for the minimum payment on every credit account before your season ends. This ensures payments are made automatically even if your attention shifts during a transitional period. The minimum is enough to protect your payment history. Combined with the off-season reserve described above, autopay for minimums means your credit score is protected from income variability entirely passively. You do not have to think about it every month during the off-season. Report your rent Many seasonal workers rent housing, often in resort towns, agricultural areas, or other seasonal employment centers. That monthly rent payment is an opportunity to add verified payment history to your credit file regardless of how your income is structured. Credit Genius reports rent payments to Experian with backdating of up to 24 months. For a seasonal worker with a thin credit file, this can create an immediate foundation of positive payment history without any change to your monthly budget or any requirement to document your employment type or income seasonality. Even short-term or seasonal housing arrangements, if they involve a formal lease or rental agreement, can be eligible for rent reporting. Check the requirements when enrolling. Document your income across the full year When applying for credit products, lenders want to assess your ability to repay. For seasonal workers, this means documenting income in a way that reflects the reality of your annual earnings rather than just your current month. Tax returns are the most credible form of income documentation for seasonal workers. A tax return showing 45,000 dollars of income for the year tells a more complete story than a recent pay stub showing zero because you are between seasons. File your taxes accurately and on time every year. Keep the last two years of returns accessible when applying for credit. Bank statements showing the pattern of high deposits during peak season followed by lower activity in the off-season can also help lenders understand your income cycle. Some lenders, particularly credit unions familiar with agricultural or resort communities, are more comfortable with seasonal income documentation than large national banks. Keep utilization low during the off-season The off-season is when credit card utilization is most likely to creep up. With lower income and existing expenses, it is tempting to rely on available credit to bridge the gap. This is understandable but it has a direct negative impact on your credit score. Try to enter the off-season with credit card balances as low as possible. Pay down balances aggressively at the end of peak season so you have maximum available credit and minimum utilization going into the period when you are least likely to be able to pay them down. Think of it like winterizing a house. Prepare your credit profile for the lean months before they arrive rather than trying to manage it reactively once income has stopped. Consider a credit builder loan timed to your season A credit builder loan with monthly payments that align with your peak earning season is

What Is a Store Credit Card and Should You Ever Open One?

You are at checkout and the cashier offers you 20% off today’s purchase if you open a store credit card. It happens at clothing stores, furniture retailers, electronics chains, and department stores across the country. The offer sounds appealing in the moment. But the question of whether you should actually say yes is more complicated than the discount makes it seem. Here is a clear-eyed look at what store credit cards are, how they affect your credit, and when they are and are not worth opening. What a store credit card actually is Store credit cards come in two varieties. A closed-loop store card can only be used at the specific retailer or family of retailers that issued it. An open-loop store card, sometimes called a co-branded card, carries a Visa, Mastercard, or similar network logo and can be used anywhere that network is accepted. Both types are issued by banks or financial institutions on behalf of the retailer. Both report to the credit bureaus and function as revolving credit accounts for credit scoring purposes. The main difference is where you can use them and the rewards structure around them. How store cards affect your credit score The application causes a hard inquiry. Every store card application results in a hard inquiry on your credit report. Hard inquiries have a small temporary negative impact on your score, typically a few points, and remain on your report for two years. If you are opening one card the impact is minor. If you open several cards across different stores in a short period the cumulative effect is more significant. It lowers your average account age. Every new account you open lowers your average account age, which is a factor in your credit score. If you have been building credit for five years and open a new store card, your average account age drops. The impact depends on how many other accounts you have and how old they are. It adds available credit and potentially lowers utilization. A new card adds to your total available credit. If your existing balances stay the same, your overall utilization ratio drops, which is positive for your score. However, store cards typically come with low credit limits, so the utilization benefit may be modest. High utilization on the store card itself is a risk. Store cards often have low credit limits, sometimes as low as 500 dollars. If you use the card for a significant purchase and carry a balance, the utilization on that specific card can be very high even if your overall utilization is fine. Per-card utilization is a factor in scoring models as well as total utilization. Interest rates are typically very high. Store credit cards carry some of the highest interest rates in the consumer credit market, frequently 28% to 32% or above. If you carry a balance for even a month or two, the interest cost often exceeds any discount you received for opening the card. When opening a store card makes sense You are making a large purchase and will pay it off immediately. If you are buying 800 dollars of furniture and a store card gives you 20% off that purchase, you save 160 dollars. If you pay the balance in full before the statement closes, you pay no interest. The hard inquiry costs a few points temporarily. For a large purchase you were going to make anyway, this math can work in your favor. You shop at that retailer frequently enough to use the rewards. Co-branded store cards often offer meaningful ongoing rewards at their partner retailer, sometimes 5% back or more. If you consistently spend significant amounts at a specific store, the rewards can accumulate to real value over time. Store cards often have lower approval requirements than mainstream credit cards. For someone with a thin or fair credit file who cannot yet qualify for a better card, a store card can be a stepping stone. The key is to use it minimally, pay it in full every month, and treat it as a temporary tool while building toward better products. When opening a store card does not make sense You are about to apply for a major loan. If you are planning to apply for a mortgage, car loan, or any major credit product in the next six to twelve months, do not open any new credit accounts including store cards. The hard inquiry and the reduction in average account age are exactly what you do not want on your file before an important application. You might carry a balance. If there is any chance you will not pay the full balance immediately, the interest rate on a store card will almost certainly cost you more than the discount you received. Store card interest rates are among the highest in the consumer credit market. You already have multiple credit cards. If you already have several well-managed credit cards with good terms, a store card adds complexity and risk without meaningful credit benefit. A better card with broader acceptance and stronger rewards is almost always preferable. You are opening it purely for the discount. Opening a card for a one-time discount on a small purchase, then never using it again, is rarely worth it. The hard inquiry, the account management overhead, and the risk of forgetting to pay the first statement on time make the discount a poor trade in most cases. What to do if you already have store cards If you have store cards you opened in the past and never use, do not rush to close them. Closing accounts reduces your available credit and can shorten your average account age. Leave them open, put a small recurring charge on them if possible to keep them active, and pay the balance in full each month. If a store card has an annual fee you do not want to pay, call the issuer and ask whether they can waive it or convert the account to a

What the CFPB Credit Card Late Fee Cap Means for Your Credit

In 2024 the Consumer Financial Protection Bureau finalized a rule that would cap credit card late fees at eight dollars for most credit card issuers, down from the typical 30 to 41 dollar fees that had become standard. The rule was immediately challenged in court by the banking industry and its implementation has been tied up in legal proceedings. Regardless of where the legal battle ultimately lands, the rule and the debate around it have significant implications for how Americans think about late fees, credit card costs, and credit building. Here is what you need to know. What the rule actually says The CFPB’s rule, issued under authority granted by the Credit Card Accountability Responsibility and Disclosure Act of 2009, known as the CARD Act, would limit late fees to eight dollars for a first missed payment and the same amount for subsequent missed payments. Current rules allow fees up to 30 dollars for a first late payment and up to 41 dollars for additional late payments within six months. The CFPB estimated that the rule would save American consumers approximately 10 billion dollars per year in late fees. The banking industry contested this, arguing that the fees serve as a deterrent against late payments and that reducing them would lead issuers to raise interest rates or reduce credit access to offset the lost revenue. The rule applies to larger credit card issuers and exempts smaller institutions with fewer than one million open accounts. What the rule does not change This is the most important thing to understand about the late fee rule from a credit perspective: it does not change how late payments are reported to the credit bureaus or how they affect your credit score. A payment reported as 30 days late damages your credit score the same amount whether the late fee was 8 dollars or 41 dollars. The fee is a financial penalty charged by the lender. The credit report mark is a separate event reported to the bureaus. Reducing the fee does not reduce the credit score impact. If the rule leads some consumers to be less concerned about missing a payment because the fee is smaller, that would be the wrong conclusion to draw. The fee is one cost of a late payment. The credit score damage is a separate and often much larger cost. The potential unintended consequences The banking industry’s argument that reduced late fees would lead to higher interest rates or tighter credit access is not without basis. Credit card issuers need to price risk into their products. If one revenue source is capped, they may adjust elsewhere. Some analysis has suggested that the primary beneficiaries of late fees are the issuers themselves, since the fees often exceed the actual cost to the issuer of a late payment. Other analysis suggests that consumers who miss payments regularly are higher-risk borrowers and that higher fees serve a legitimate deterrence function. What is clear is that the net effect on consumers depends on how issuers respond. If they raise interest rates to compensate, consumers who carry balances may pay more overall even with lower late fees. If they tighten credit access, some consumers may find it harder to get approved. What this means for credit building For consumers actively building or protecting their credit score, the late fee cap changes very little in practical terms. The single most important credit principle remains unchanged: pay on time, every time. A missed payment costs 50 to 100 points or more on your credit score and stays on your report for seven years. That is a cost that dwarfs any late fee, capped or uncapped. The fee reduction does not change the calculus around the importance of on-time payments. Set up autopay for the minimum payment on every account. This ensures you never miss a payment due to forgetfulness regardless of what the late fee happens to be. The fee is the least of the consequences of a missed payment. The broader CFPB credit reform agenda The late fee rule is one piece of a broader CFPB agenda that has significant implications for how credit works in America. Other major actions have included the removal of medical debt from credit reports, guidance on Buy Now Pay Later regulation, and ongoing scrutiny of credit reporting accuracy. The removal of medical collections under 500 dollars from credit reports in 2023 was a significant change that directly improved scores for millions of Americans who had medical debt on their files. This is an example of a regulatory change that had a real and immediate credit score impact, unlike the late fee cap which leaves the credit reporting system unchanged. Staying informed about regulatory changes affecting the credit system is worth doing. Tools like Credit Genius that provide real-time Experian monitoring and AI-powered guidance will reflect these changes as they take effect and help users understand how their own credit profile is affected. The bottom line The CFPB credit card late fee cap is a significant consumer finance development that could save Americans billions of dollars in fees if implemented as written. Its legal future remains uncertain as of 2026.For your credit score, the rule changes nothing. Late payments damage your credit regardless of the fee size. The most important thing you can do remains the same: pay on time, every time, on every account. No regulatory change makes that less true.