Will Buy Now Pay Later Eventually Replace Credit Cards?

Buy Now Pay Later has grown from a niche checkout option to one of the most widely used payment methods in the United States. Tens of millions of Americans now use it regularly. The companies behind it are valued in the billions. And a growing number of younger consumers appear to prefer it over traditional credit cards. So will Buy Now Pay Later eventually replace credit cards? The short answer is no, at least not in any complete or near-term sense. But the longer answer reveals something more interesting about how the two products are evolving and what that means for your credit. What Buy Now Pay Later does well Buy Now Pay Later solves a specific problem elegantly: it lets consumers spread the cost of a purchase over a short period, typically four installments over six weeks, without the complexity of a credit card application, a credit limit, or revolving debt. For many consumers, particularly younger ones who are skeptical of credit card debt or who have been excluded from traditional credit products, Buy Now Pay Later is more accessible and feels more transparent. You know exactly what you will pay and when. There is no revolving balance that can grow if you only pay the minimum. The frictionless checkout experience has also driven rapid adoption. Adding a Buy Now Pay Later option at checkout takes seconds. It does not require an existing account or a credit check in most cases. For retailers, it increases conversion and average order value. For consumers, it feels less like debt and more like a payment schedule. What Buy Now Pay Later does not do Despite its growth, Buy Now Pay Later has significant limitations that prevent it from replacing credit cards for most consumers and use cases. It does not build credit reliably. Credit cards with consistent on-time payments build a strong credit history. Buy Now Pay Later reporting to credit bureaus is inconsistent across providers and still evolving. For consumers who need to build or maintain a credit score for housing, auto loans, or mortgages, credit cards remain the more reliable credit-building tool. It does not offer the same consumer protections. Credit cards come with robust federal protections including the ability to dispute charges, chargeback rights, and zero liability for fraudulent purchases. Buy Now Pay Later protections vary significantly by provider and are generally weaker. The CFPB has noted this gap and has signaled interest in extending credit card-style protections to Buy Now Pay Later products. It does not offer rewards. The rewards ecosystem built around credit cards, including cash back, travel points, and sign-up bonuses, represents significant value for cardholders who pay their balance in full. Buy Now Pay Later products generally offer no equivalent. It does not work everywhere. Credit cards are universally accepted. Buy Now Pay Later is available only at participating merchants. For everyday spending like groceries, gas, and utilities, credit cards remain the only option. It does not handle large or ongoing expenses. Buy Now Pay Later is designed for discrete purchases. It does not work for recurring bills, subscriptions, or large ongoing expenses in the way that a credit card with a revolving limit does. How credit cards are responding The credit card industry has not ignored Buy Now Pay Later’s growth. Major card issuers have responded by adding installment plan features directly to existing cards. American Express, Chase, Citi, and others now offer their own versions of pay-over-time options for large purchases. This hybrid approach combines the credit-building benefits, consumer protections, and universal acceptance of credit cards with the installment payment structure that makes Buy Now Pay Later appealing. For many consumers, this may be the best of both worlds. The regulatory picture The CFPB has taken an increasing interest in Buy Now Pay Later and in 2024 issued guidance clarifying that many Buy Now Pay Later products should be treated as credit cards under existing law, which would subject them to the same disclosure requirements, dispute rights, and consumer protections. This regulatory pressure is pushing the industry in two directions simultaneously: toward more consumer-friendly terms that look more like credit cards, and toward more consistent credit bureau reporting. Both developments will change the credit implications of Buy Now Pay Later over the next several years. What this means for your credit As Buy Now Pay Later reporting to credit bureaus becomes more common, the credit implications of these products will become more significant in both directions. On-time payments may begin building credit more reliably. Missed payments will increasingly damage credit scores. For anyone actively building or managing their credit, the practical implication is to treat Buy Now Pay Later obligations with the same discipline as credit card payments. Missed payments are increasingly likely to show up on your credit report, and the informal feeling of the product should not obscure that reality. For credit building specifically, traditional tools like credit cards, credit builder loans, and rent reporting through services like Credit Genius remain more reliable than Buy Now Pay Later because their reporting relationships with credit bureaus are established and consistent. The bottom line Buy Now Pay Later will not replace credit cards. It will continue to grow as a complement to credit cards for specific purchase types and specific consumer segments. The two products are converging in some ways, with credit cards adding installment features and Buy Now Pay Later products facing pressure to add consumer protections and credit reporting.For consumers, the takeaway is straightforward. Use Buy Now Pay Later where it genuinely helps you manage a purchase. Treat every payment obligation seriously regardless of how informal the product feels. And if building or maintaining your credit score is a priority, make sure the financial behaviors you are relying on to do that are connected to products with reliable, consistent bureau reporting.

How Credit Scores Differ by Race and Income in America

Credit scores are presented as objective measures of individual financial behavior. In practice, the data shows persistent and significant gaps in credit scores across racial and income lines. Understanding those gaps, where they come from, and what they mean for the people affected by them is important context for anyone trying to build or improve their credit in America. This article covers what the data actually shows, the structural reasons behind it, and what individuals can do to build credit despite systemic disadvantages. What the data shows The credit score gaps between racial groups in the United States are well documented. Research from the Urban Institute and other policy organizations consistently finds that Black and Hispanic Americans have significantly lower average credit scores than white and Asian Americans. A 2022 analysis found that the average credit score for Black Americans was approximately 100 points lower than for white Americans. Income correlates with credit scores as well, though the relationship is more nuanced than it might appear. Higher income households tend to have higher average credit scores, but the correlation is not one-to-one. Lower income households are more likely to be credit invisible, meaning they have no credit file at all, or to have thin files with limited history. The Consumer Financial Protection Bureau has estimated that approximately 26 million Americans are credit invisible and another 19 million have files too thin or stale to generate a reliable score. These populations are disproportionately Black, Hispanic, and lower income. Why these gaps exist: the structural factors The credit score gaps between racial and income groups did not emerge from individual behavior alone. They are the product of structural factors that have shaped access to credit building opportunities across generations. Historical exclusion from credit. Redlining, discriminatory lending practices, and explicit exclusion of Black Americans from FHA-backed mortgages and conventional credit products through much of the twentieth century meant that generations of Black families were prevented from building the credit history and home equity that wealth and credit scores are built on. These exclusions were not individual failures. They were policy. The homeownership gap. Mortgage payments are automatically reported to the credit bureaus and contribute directly to credit scores. Homeownership rates among Black Americans are significantly lower than among white Americans, a gap that traces directly to historical exclusion and continues to compound. Renters, who are disproportionately Black and Hispanic, make their largest monthly payment without receiving credit recognition for it unless they actively report it. Lower income creates direct credit challenges: higher likelihood of carrying high utilization, greater vulnerability to missed payments during financial shocks, and less ability to maintain the savings buffer that protects credit during emergencies. The racial wealth gap, estimated at roughly ten to one between white and Black households by the Federal Reserve, means these income-related credit challenges fall disproportionately on communities of color. Predatory lending. Communities of color have been disproportionately targeted by high-interest payday lenders, predatory auto dealers, and subprime mortgage products. These products often create credit damage rather than building credit, leaving borrowers with derogatory marks from products that were designed to extract rather than support. Credit invisibility. Communities with lower homeownership rates, less access to mainstream banking, and less generational wealth to pass on credit-building knowledge and authorized user access are more likely to be credit invisible. Credit invisibility is not a reflection of financial irresponsibility. It is a reflection of which financial behaviors the credit system was designed to recognize. Does the credit scoring system itself contribute to the gaps? This is a legitimately debated question among researchers and policy advocates. The credit scoring system does not use race as a factor and is prohibited from doing so. But critics argue that factors like the exclusion of rent and utility payments from traditional scoring, the emphasis on account age which disadvantages those who were historically excluded from credit, and the reliance on data from a system that has historically underserved communities of color means the system encodes historical inequity even without explicitly using race. Defenders of the current system argue that credit scores are accurate predictors of repayment behavior across all demographic groups and that the solution to the gap is expanding access to credit rather than changing the scoring methodology. Both arguments contain truth. The gaps in credit scores reflect real differences in credit behavior that are themselves produced by structural inequity. Addressing the gaps requires both expanding what counts as credit-worthy behavior and addressing the underlying conditions that create unequal credit outcomes. What is being done to address the gaps Several policy and industry developments in recent years are directly aimed at reducing credit score disparities. The expansion of rent reporting is one of the most significant. Legislation in several states now requires landlords to offer rent reporting to tenants. The CFPB has encouraged broader use of alternative data including rent and utility payments in credit underwriting. Companies like Credit Genius that report rent to Experian are part of an industry-wide movement to make the credit system recognize the financial behaviors of renters, who are disproportionately people of color. The removal of medical debt from credit reports, completed for collections under 500 dollars in 2023 and expanded further, disproportionately benefits communities of color who are more likely to carry medical debt due to lower rates of insurance coverage. Alternative credit scoring models that incorporate rent, utility, and other non-traditional payment data are gaining traction among some lenders, particularly for mortgage underwriting. What individuals can do Structural problems require structural solutions and individual action alone cannot close gaps that were produced by decades of policy. But understanding the system and using the tools available to work within it remains the most practical path forward for individuals navigating it right now. Report your rent. If you are paying rent on time, that payment should be on your credit file. Credit Genius reports to Experian with backdating, giving you credit for the financial behavior you are already demonstrating. Dispute errors. Research suggests that errors

How to Get Your First Apartment After College With Limited Credit History

Getting your first apartment after college puts you in a frustrating position. Landlords want to see credit history to prove you are a reliable tenant. But you have spent the last four years living in dorms or student housing that did not require a credit check or build any credit history. The system expects experience you were never given the chance to build. This is a solvable problem. Here is a practical guide to getting approved for your first apartment even with limited or no credit history. Understand what landlords are actually evaluating Landlords are not just looking at a credit score number. They are trying to answer one question: will this person pay rent on time every month? Your credit score is one input into that question but it is not the only one. Income, references, rental history, and the overall picture of your application all factor in. This matters because it means a thin credit file is not automatically a dealbreaker. It means you need to build a compelling case through other parts of your application that compensates for what the credit file cannot yet show. Know your credit situation before you apply Pull your credit reports from annualcreditreport.com before you start applying. You may have more credit history than you think. Student loans appear on your credit file. If you were added as an authorized user on a parent’s credit card at some point, that account history may appear on your report. If you had a credit card in college, that history is there. Knowing exactly what is in your file lets you speak to it confidently in conversations with landlords and avoid surprises when they run a check. Prove income clearly and compellingly Most landlords want to see monthly income of at least two to three times the rent. If you have a job offer or have already started working, your offer letter, first pay stub, or employment verification letter is powerful documentation. If you are freelancing or starting a business, bank statements showing regular income deposits can supplement. If your income meets the threshold clearly, many landlords are willing to look past a thin credit file. Lead with the income documentation rather than waiting for them to ask. Get a co-signer A co-signer with strong credit agrees to be legally responsible for the rent if you fail to pay. For a landlord worried about a thin credit file, a co-signer eliminates the risk they are concerned about. Most landlords will approve an applicant with limited credit if the co-signer has a strong profile. This is a significant ask of the co-signer, typically a parent or close family member, because they are taking on real legal and financial exposure. Have an honest conversation about what you are asking them to do before making the request. Offer a larger security deposit A larger upfront deposit directly addresses the risk a landlord is concerned about. If you can offer two or three months of rent as a security deposit instead of one, many landlords will approve an application that might otherwise give them pause. This requires having the cash available, which not everyone does immediately after college. If you have some savings from a summer job or a signing bonus from a new employer, allocating a portion to a larger deposit can be the difference between getting the apartment and not. Provide strong references A reference letter from a previous landlord, even a dorm RA, resident advisor, or university housing office, confirming that you paid on time and took care of your space carries real weight. If you lived off campus at any point, a reference from that landlord is even more valuable. Personal references from employers, professors, or mentors who can speak to your reliability and character are also useful. A well-rounded application with strong references humanizes what a credit report cannot yet show. Consider different types of landlords Large corporate property management companies tend to have stricter, more standardized credit requirements with less flexibility for individual circumstances. Independent landlords renting one or a few units are often more willing to consider the full picture of an applicant rather than applying a hard cutoff score. This does not mean avoiding large buildings, but it does mean that a direct conversation with a smaller landlord about your situation may be more productive than an online application to a large complex with automated screening. Start building credit before you apply If you have any lead time before your apartment search, use it. Even two to three months of credit building can make a meaningful difference. If you have student loans, they are likely already on your credit file. Make your payments on time from the first payment due. Open a secured credit card and use it for one small purchase per month, paying the full balance each time. If you have a parent willing to add you as an authorized user on a long-standing account, that can immediately give your file more substance. And once you are in your first apartment, enroll in rent reporting through Credit Genius immediately. That monthly rent payment is the largest financial obligation most people your age have. Getting it on your credit file from day one means you start building a real credit history from the moment you move in rather than losing months of positive data. The bottom line Getting your first apartment after college with limited credit is harder than it should be but it is absolutely achievable. Know your credit situation, lead with strong income documentation, consider a co-signer or larger deposit, choose the right type of landlord, and build as much credit as you can in the time available before you apply.Once you are in, report your rent from day one. The credit history you build in your first apartment sets the foundation for every housing application, loan, and financial decision that follows.

How to Build an Emergency Fund and Good Credit at the Same Time

Most personal finance advice treats emergency funds and credit building as separate goals that you tackle one at a time. Build your emergency fund first, then work on credit. Or get your credit sorted, then focus on savings. In practice, most people do not have the luxury of addressing one before the other. They need both, and they need to be building both simultaneously. The good news is that these two goals are not in conflict. With the right approach they reinforce each other. Here is how to build both at the same time without feeling like you are being pulled in two directions. Why you need both and why they are connected An emergency fund and good credit serve similar purposes from different directions. An emergency fund is liquid cash you can access immediately when something goes wrong. Good credit is the ability to access borrowed money quickly and cheaply when something goes wrong. Together they give you two layers of financial resilience. The connection goes deeper. One of the most common ways people damage their credit is by missing payments during financial emergencies. A job loss, medical bill, or car repair that wipes out available cash can lead to missed minimum payments, which are among the most damaging credit events you can experience. An emergency fund prevents that cascade. It protects your payment history, the most important factor in your credit score, from being disrupted by events outside your control. Building both simultaneously is not just possible. It is strategically smarter than doing one at a time. Start with a minimum viable emergency fund The conventional advice is to build three to six months of expenses as an emergency fund. For most people starting from scratch, that is an overwhelming target that can feel paralyzing. Do not start there. Start with one month of essential expenses. Rent, utilities, minimum debt payments, and basic groceries. That number is smaller and more achievable. And one month of runway is enough to absorb most common financial emergencies without missing credit payments. Once you have one month saved, you can begin directing more attention to credit building while continuing to grow the fund toward two and then three months over time. The one-month mark is the threshold that provides meaningful credit protection. Use a credit builder loan to save and build credit simultaneously This is one of the most elegant solutions to the save-and-build-credit challenge. A credit builder loan works by making fixed monthly payments into a locked savings account. The lender reports those payments to the credit bureaus while you build savings. At the end of the loan term you receive the accumulated balance back minus fees. Every dollar you put into a credit builder loan is simultaneously building your emergency fund and your credit history. At the end of a 12-month term on a modest loan, you have a year of positive payment history on your credit file and a lump sum of savings returned to you. That savings can then go directly into your emergency fund. The fixed monthly payment is also behaviorally useful. It automates the savings habit without requiring ongoing willpower decisions about whether to save this month. Report your rent to build credit without touching your savings One of the most powerful aspects of rent reporting is that it builds credit from payments you are already making. You are not redirecting money away from savings. You are not taking on new debt. You are simply getting credit recognition for a financial obligation you are already meeting. Credit Genius reports rent payments to Experian with backdating of up to 24 months. This means you can add significant positive payment history to your credit file without any change to your monthly budget. Every dollar of your income continues flowing toward savings or debt reduction while your credit file grows simultaneously. For someone trying to build both an emergency fund and good credit on a tight budget, rent reporting is the closest thing to a free credit-building move available. Use a secured credit card with a small deposit A secured credit card requires a deposit that becomes your credit limit. The deposit sits in your account, functioning similarly to a small emergency reserve while also enabling credit building. When you eventually close the card or graduate to an unsecured product, the deposit is returned to you. The key is to use the card for one or two small recurring purchases, like a streaming subscription or a gas fill-up, and pay the full balance every month. This builds payment history and keeps utilization low without adding any meaningful debt to your financial picture. Think of the deposit not as money spent but as money working double duty: it is securing your credit-building tool while remaining yours to reclaim. Automate both goals The most reliable way to build both an emergency fund and good credit simultaneously is to automate both so neither requires an active decision every month. Set up autopay for the minimum payment on every credit account. Set up an automatic transfer to your savings account on payday. Enroll in rent reporting so your monthly payment goes to the bureau without any action on your part. With these three automations in place, you are building your emergency fund and your credit profile every month without having to think about it. Automation removes the willpower requirement from both goals. And behavioral research is clear that habits sustained by automation are far more durable than those that depend on consistent conscious decisions. How to split your extra money between the two goals If you have extra money each month after covering essentials and minimum debt payments, a simple allocation framework is helpful. Until you have one month of essential expenses saved, direct 70% of extra money toward the emergency fund and 30% toward credit building activities like paying down high-utilization cards. Once you hit one month saved, shift to 50/50. Once you hit three months saved, you can direct more

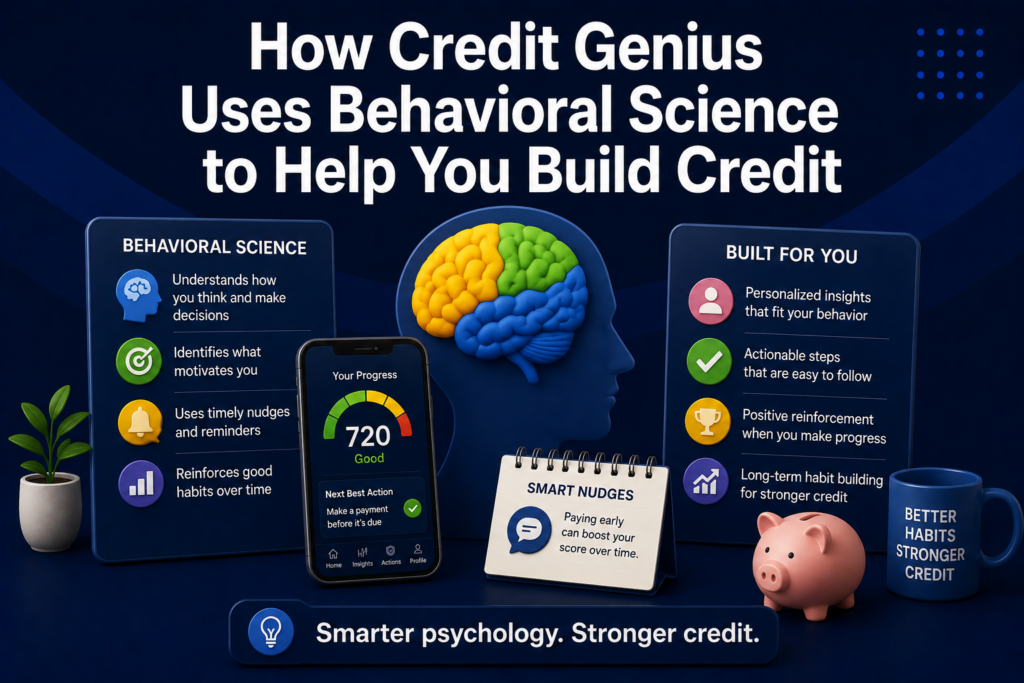

How Credit Genius Uses Behavioral Science to Help You Build Credit

Most credit apps treat credit building as an information problem. They assume that if you show someone their score and explain what affects it, they will make better credit decisions. The data on financial literacy programs consistently shows this is not how behavior change actually works. Credit Genius was built around a different premise: that credit building is primarily a behavior problem, not an information problem. And behavior change requires a different set of tools than information delivery. Here is how behavioral science principles are applied throughout the Credit Genius platform. The gap between knowing and doing Research in behavioral economics has consistently found that the gap between knowing what to do and actually doing it is one of the most stubborn problems in personal finance. People know they should pay their bills on time. They know they should keep their credit utilization low. They know they should check their credit report regularly. Most of them do not do these things consistently. This is not a failure of intelligence or willpower. It is a reflection of how human motivation and habit formation actually work. Knowing the right behavior does not automatically produce the right behavior, particularly when the reward is abstract and distant while the effort is immediate and concrete. Credit building has exactly this structure. The reward, a better credit score and better financial opportunities, may be months away. The effort, managing payments, monitoring accounts, making deliberate financial decisions, is required right now. Behavioral science offers a framework for bridging that gap. Immediate feedback loops One of the core principles of behavioral design is that behavior is reinforced when feedback is immediate and visible. When the connection between an action and its outcome is clear and fast, people are more likely to repeat the action. Credit Genius provides real-time Experian credit monitoring that delivers immediate alerts when anything changes on your credit file. When a positive change appears, such as a rent payment being processed or a balance updating after a payoff, you see it right away. The feedback loop between action and outcome is compressed from weeks or months into days. This immediacy matters. Behavioral research shows that delayed feedback significantly weakens its reinforcing power. A credit score update that arrives weeks after the action that caused it feels disconnected from the behavior. A real-time alert that says your score moved because of a specific action you took creates a much stronger link between the behavior and its reward. Personalization and relevance Generic advice is easy to ignore. Specific, relevant guidance directed at your particular situation is much harder to dismiss. This is why personalization is a behavioral principle as much as a product feature. The Credit Genius AI credit assistant does not deliver the same tips to every user. It reads your actual Experian credit file and identifies the specific factors that are limiting your score right now. The guidance you receive is prioritized by impact and tailored to your individual situation. When someone is told that their single biggest opportunity to improve their score is paying down a specific card from 78% utilization to below 30%, that is actionable and specific. It is behaviorally different from being told to keep utilization low in general. The specific, personalized instruction removes the ambiguity that causes inaction. Gamification and intrinsic motivation Credit Games, the gamified financial education component of Credit Genius, is built directly on behavioral science principles around motivation and habit formation. Games are one of the few contexts where humans voluntarily engage in repetitive, effortful behavior for extended periods. The reason is that games are designed to satisfy the psychological needs that drive sustained engagement: competence, progress, and autonomy. Progress indicators. Seeing measurable progress toward a goal is one of the most reliable motivators in behavioral psychology. Credit Games use progress tracking to make the learning journey visible, giving users a concrete sense of advancement rather than an abstract sense of reading articles. Streaks and consistency reinforcement. Streak mechanics, where users are rewarded for consecutive days or sessions of engagement, tap into loss aversion, one of the most powerful forces in behavioral economics. The desire not to break a streak motivates continued engagement even on days when motivation is otherwise low. Challenges and goal setting. Structured challenges give users specific short-term goals to work toward, which behavioral research shows produces more consistent effort than open-ended aspirations. A user working toward completing a specific Credit Game challenge is more focused than one told to generally improve their financial literacy. Reducing friction Behavioral science consistently shows that reducing friction around desired behaviors dramatically increases the likelihood of those behaviors occurring. Every additional step between a user and a credit-building action is a point at which they may give up. The Genius Rent Boost enrollment process is designed with friction reduction in mind. Rather than requiring users to gather extensive documentation, navigate complex forms, or wait weeks for results, the enrollment is streamlined and the backdating feature means results appear quickly. The behavioral principle at work is that the faster and easier a beneficial action is to take, the more people take it. Similarly, having all credit-building tools, rent reporting, AI guidance, financial education, and monitoring in a single app reduces the friction of managing a credit improvement strategy across multiple platforms. Social proof and community One of the most powerful behavioral influences on human decision-making is observing what others in similar situations are doing and achieving. When people see that others like them have successfully improved their credit through specific actions, they are more likely to believe those actions will work for them and to take them. The pilot data from Credit Genius’s 10,000-user launch showed measurable score improvements across the user base. When users can see that the behaviors the platform is encouraging are producing real outcomes for real people, the motivational power of that evidence compounds their own engagement. Why this approach produces better outcomes The behavioral science approach to credit building is not just philosophically

How to Prepare Your Credit Before Having a Baby

Having a baby changes almost everything about your financial life. Costs go up, income may temporarily go down during parental leave, and the financial decisions you make in the months before and after birth carry more weight than they ever have before. Your credit score sits in the middle of all of it, affecting your housing options, your borrowing costs, and your financial flexibility during one of the most expensive transitions of your life. Here is how to use the months before your baby arrives to get your credit in the strongest position possible. Why credit matters more than usual before a baby The timing of parenthood often coincides with other major financial decisions. Many people buy a home, upgrade to a larger apartment, or take out a personal loan for home improvements or baby expenses in the period around a new child. Each of these decisions is heavily influenced by your credit score. Parental leave adds another layer. If one parent takes unpaid or partially paid leave, the household income drops while expenses rise. A financial buffer and a strong credit profile together provide the flexibility to handle that period without making panic decisions that damage your long-term financial health. Starting this process at least six to twelve months before your due date gives your credit improvements time to show up in your score before the decisions that depend on it arrive. Pull and review all three credit reports Start by pulling your full credit reports from annualcreditreport.com and reviewing each one carefully. Look for errors in payment history, accounts you do not recognize, outdated negative marks, and anything that should have fallen off your report but has not. One in five Americans has at least one error on their credit report. An error that goes unnoticed until you are trying to qualify for a mortgage or a personal loan in the middle of a new baby’s arrival is a problem you do not need at that moment. Find it now, dispute it now, and let it be resolved before the stakes are higher. Pay down credit card balances Credit utilization is the second most important factor in your credit score at 30% of the total. If you are carrying significant balances on credit cards, paying them down before your baby arrives does two things simultaneously: it improves your credit score and it frees up your credit line for genuine emergencies during a period when unexpected expenses are almost guaranteed. The goal is to get utilization below 30% on each card and ideally below 10%. This can produce a noticeable score improvement within one to two billing cycles of paying down balances. If you are planning to apply for a mortgage or a larger apartment before the baby comes, paying down utilization should be your first credit priority. Set up autopay on everything New parents are busy people. Sleep deprivation is real and so is the cognitive load of managing a newborn alongside every other responsibility. This is exactly the wrong environment for manually tracking payment due dates across multiple accounts. Set up autopay for the minimum payment on every account before your baby arrives. You can always pay more manually. But autopay ensures you never miss a payment simply because you forgot in the fog of a newborn’s first months. A missed payment costs 50 to 100 points and stays on your report for seven years. That is a problem you can completely prevent with ten minutes of setup today. Do not open new credit accounts in the months before major applications If you are planning to apply for a mortgage, a larger apartment, or a personal loan in the six to twelve months before or after your baby arrives, stop opening new credit accounts now. New accounts lower your average account age and add hard inquiries, both of which temporarily reduce your score. The temptation to open a new store card for baby purchases or take advantage of a promotional financing offer on a crib or stroller is real. Resist it. The discount is not worth the credit impact at a moment when your score matters for larger decisions. Build a credit buffer before income drops If you or your partner plan to take parental leave that reduces household income, the months before the baby arrives are the time to pay down as much revolving debt as possible. High utilization during a period of reduced income is harder to manage and easier to slip into. Going into parental leave with low balances on your credit cards gives you a buffer. If an unexpected expense arises during leave, you have available credit to use without immediately pushing utilization into score-damaging territory. Think of low credit utilization as financial headroom for an unpredictable period. Make sure your rent is being reported If you are renting and your payments are not being reported to the credit bureaus, you are missing an opportunity to add positive payment history to your file at a time when every point matters. Credit Genius reports rent to Experian with backdating of up to 24 months, meaning you do not have to start from zero. Adding verified rent payment history to your credit file in the months before a major housing application can meaningfully improve your score and strengthen your overall credit profile at exactly the right moment. Understand your parental leave rights and plan financially This is not strictly a credit tip but it directly affects your credit outcomes. Know what your employer provides for parental leave, what state benefits you may be entitled to, and what the income gap will be during leave. Understanding the numbers in advance allows you to plan for them rather than react to them. A household that enters parental leave with a clear budget for the leave period, low credit card balances, autopay set up on all accounts, and a small emergency fund is in a fundamentally different position than one that enters it unprepared. The credit implications

How a Car Repossession Affects Your Credit and How Long It Stays

A car repossession is one of the more damaging credit events a person can experience. It is not just the loss of a vehicle. It is a cascade of negative credit marks that can take years to fully recover from. Understanding exactly what happens to your credit, how long each mark stays, and what you can do to recover is the starting point for getting through it. What actually happens to your credit during a repossession A repossession does not create a single credit mark. It creates several, each layered on top of the other. By the time a vehicle is repossessed, your credit has usually already been damaged through a series of escalating events. Missed payments. Lenders typically repossess a vehicle after two or three consecutive missed payments. Each missed payment is reported to the credit bureaus at the 30-day, 60-day, and 90-day marks. Each stage is increasingly damaging. By the time repossession happens, your report may already carry multiple late payment marks. The repossession itself. Once the vehicle is repossessed, the lender reports it to the credit bureaus as a repossession. This is a separate derogatory mark from the missed payments and it carries significant weight on its own. Deficiency balance. After repossessing the vehicle, the lender typically sells it at auction. If the sale price does not cover what you owe on the loan, the remaining balance is called a deficiency. You are still legally responsible for that deficiency and the lender can pursue it through collections. A collections account for the deficiency balance adds yet another negative mark to your report. If the deficiency balance goes unpaid long enough, the lender may charge it off, meaning they write it off as a loss. A charge-off is reported to the bureaus and represents another derogatory mark on your file. How many points can you lose? The total credit score impact of a repossession depends on where your score was before it happened and how many negative marks accumulated. The combination of multiple late payments plus a repossession notation plus a potential collections account can easily drop a score by 100 points or more. For someone who started with a score in the 700s, a repossession can push them into the 500s. For someone already in the 600s, it can push them into territory where qualifying for basic credit products becomes very difficult. How long does a repossession stay on your credit report? The repossession notation itself stays on your credit report for seven years from the date of the first missed payment that led to the repossession, not from the date the car was actually taken. This is the original delinquency date rule that applies to most derogatory marks. The missed payment marks also stay for seven years from their respective dates. A collections account for the deficiency stays for seven years from the original delinquency date. A charge-off stays for seven years from the date of the charge-off. The practical reality is that all of these marks tend to cluster around the same general time period since they all stem from the same series of events. Most of the damage clears from your report at around the same seven-year mark. Voluntary surrender vs involuntary repossession If you know you cannot make your payments and repossession is inevitable, voluntarily surrendering the vehicle is worth considering. A voluntary surrender is still reported as a negative event and still appears on your credit report. It is not dramatically better for your credit than an involuntary repossession. However, it can reduce additional costs. Lenders may charge fees for the repossession process itself if they have to send someone to collect the vehicle. Voluntary surrender eliminates those costs, which reduces the potential deficiency balance you might owe. Some lenders also view voluntary surrender slightly more favorably than an involuntary repossession when making future lending decisions, though both appear as negative items on your report. Can you remove a repossession from your credit report early? If the repossession is accurately reported, it cannot be removed before the seven-year period expires. However, if there are inaccuracies in how it is reported, such as an incorrect date of first delinquency, wrong balance, or errors in account details, those can be disputed and corrected. Pull your credit reports from all three bureaus and review the repossession entry carefully. If you find errors, file a dispute with documentation. An inaccurately reported repossession is worth pursuing through the dispute process. How to rebuild after a repossession Recovery from a repossession is a long-term process but it is achievable with consistent effort. Address the deficiency balance. If you owe a deficiency, ignoring it leads to collections and additional credit damage. Contact the lender to negotiate a settlement or payment arrangement. Settling the deficiency for less than the full amount is often possible and stops the damage from compounding further. Open a secured credit card. After a repossession, your credit options are limited but secured cards are generally accessible. A small deposit, consistent use, and on-time monthly payments start rebuilding your payment history immediately. Report your rent. If you are renting, every on-time payment is an opportunity to add positive data to your credit file. Credit Genius reports rent to Experian with backdating of up to 24 months, giving you an immediate foundation of positive payment history to build on while the repossession sits on your report. Pay everything else on time. The repossession is on your report for seven years regardless of what you do next. What you can control is what gets added around it. Consistent on-time payments on all remaining and new accounts dilute the impact of the repossession over time. The bottom line A car repossession is a serious credit event that leaves multiple negative marks and stays on your report for up to seven years. The damage is real but it is not permanent. The path forward is to address any remaining debt, open accessible credit products, build positive payment history consistently, and

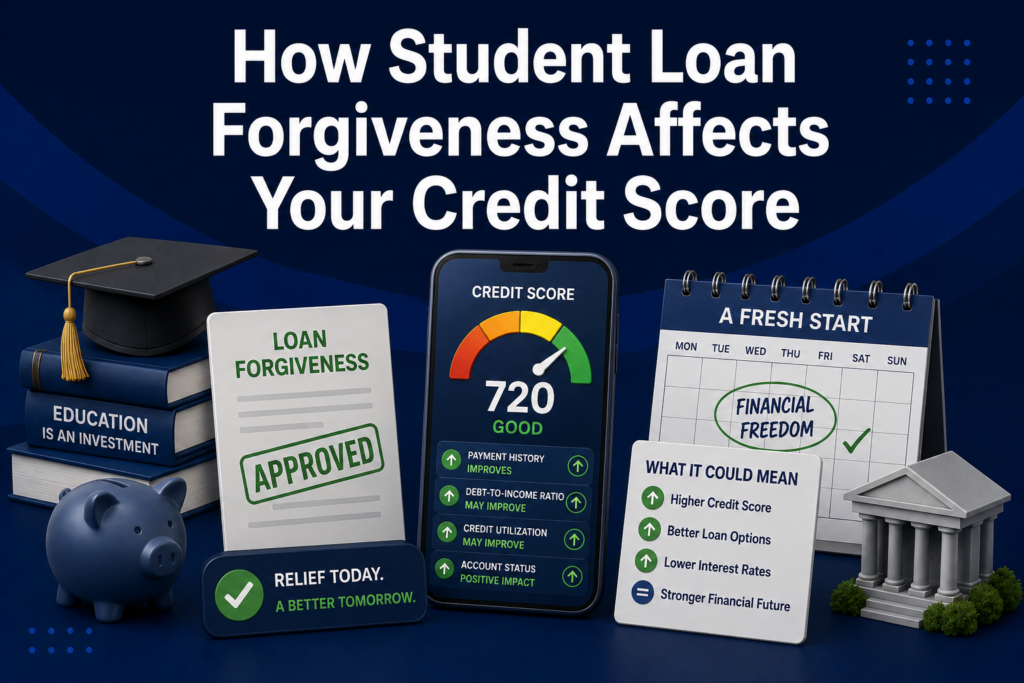

How Student Loan Forgiveness Affects Your Credit Score

Student loan forgiveness sounds like an unambiguous win. Your debt is wiped out and you never have to pay it back. But when it comes to your credit score, the reality is more nuanced. Loan forgiveness can affect your credit in ways that are positive, neutral, or occasionally temporarily negative depending on how your loans were structured and what your credit file looks like before forgiveness. Here is a clear breakdown of what actually happens to your credit when student loans are forgiven. The good news first For most borrowers, student loan forgiveness is either neutral or mildly positive for their credit score. The forgiven loan shows up on your credit report as paid in full or closed with a zero balance. A loan that is paid in full is a positive credit event, and it removes what may have been a significant balance from your total debt load. If your forgiven loans had been in good standing throughout repayment, the account history, including all those years of on-time payments, remains on your credit report for up to ten years after the account closes. That positive payment history continues to benefit your score for years after the loan is gone. The potential temporary downside The reason some borrowers see a temporary score dip after loan forgiveness comes down to two factors: credit mix and account age. Having a mix of revolving accounts like credit cards and installment accounts like loans contributes positively to credit mix, which accounts for 10% of your FICO score. When an installment account is closed, your mix becomes less diverse. If student loans were your only installment accounts, their forgiveness and closure can slightly reduce this factor. Average account age. The length of your credit history accounts for 15% of your score, including the average age of all open accounts. When a long-standing loan account closes, it no longer contributes to your average account age calculation for open accounts. If your student loans were among your oldest accounts, their closure can lower your average account age slightly. Both of these effects tend to be modest, often just a few points, and temporary. The closed account remains on your report for up to ten years and its positive history continues to count during that time. What about debt-to-income ratio? Debt-to-income ratio does not appear on your credit report and is not a factor in your credit score. However, it matters significantly to lenders when you apply for mortgages and other major loans. Having student loan debt forgiven reduces your monthly debt obligations and therefore improves your DTI. This can be a significant benefit if you were previously unable to qualify for a mortgage because your student loan payments were pushing your DTI above lender thresholds. Forgiveness may open the door to homeownership that the debt was blocking. What about loans that were in default before forgiveness? This is where it gets more complicated. If your student loans were in default before being forgiven, the negative marks associated with that default, including late payment records and the default notation itself, do not automatically disappear when the loan is forgiven. A loan forgiven through Public Service Loan Forgiveness or income-driven repayment forgiveness programs, where the borrower was in good standing throughout, closes as paid in full with no negative history attached. A loan forgiven after a period of default may still carry the derogatory marks from that period on the credit report, even though the balance is now zero. If your loans had negative marks before forgiveness and those marks are still showing on your report, you can dispute any inaccuracies but accurately reported derogatory information from a default period remains on your report for seven years from the original delinquency date regardless of forgiveness. The income tax question This is not a credit question but it is an important one. Depending on the type of forgiveness and current tax law, forgiven student loan balances may be treated as taxable income in the year of forgiveness. This does not affect your credit score but it can affect your financial situation in that year. Federal student loan forgiveness under income-driven repayment plans was tax-free through 2025 under temporary provisions. The tax treatment beyond that period depends on legislation in effect at the time of forgiveness. If you are approaching forgiveness, it is worth understanding the potential tax implications in advance. How to protect your credit around loan forgiveness In the months leading up to expected loan forgiveness, avoid opening new credit accounts that would lower your average account age further. If you have other installment accounts in good standing, maintain them to preserve your credit mix. After forgiveness, monitor your credit file closely to make sure the loan is reported correctly as paid in full or closed with zero balance. If anything is reported inaccurately, dispute it promptly. If the closure of your student loans reduces your credit mix and you want to add a new installment account to maintain diversity, a credit builder loan is a low-risk option. It adds an installment account without taking on significant debt. And if you are a renter, this is a good moment to ensure your rent payments are being reported to the credit bureaus through a service like Credit Genius. Adding verified rent payment history to your Experian file provides ongoing positive payment data that supports your score as your credit profile adjusts to the closure of your student loans. The bottom line Student loan forgiveness is generally neutral to mildly positive for your credit score when the loans were in good standing. You may see a small temporary dip from credit mix and account age effects, but the positive payment history from years of on-time payments remains on your report and continues to benefit you.The financial benefit of eliminating the debt and improving your debt-to-income ratio almost always outweighs any minor credit score adjustment. For most borrowers, forgiveness is unambiguously good news, credit included.

How Your Credit Score Affects Every Major Purchase You Make

Most people think about their credit score when they are applying for something specific, a loan, a credit card, an apartment. But the impact of your credit score is broader and more constant than that. It quietly shapes the cost of almost every significant financial transaction in your life, often in ways you never see directly. Here is a complete picture of how your credit score affects the major purchases and financial decisions you will make throughout your life, with real numbers where available. Renting an apartment Your credit score is one of the first things most landlords and property management companies check. In competitive rental markets, a score below 620 can result in outright rejection. A score in the Fair range often means being asked for a larger security deposit, sometimes two or three months of rent rather than one. On a 1,500 dollar per month apartment, the difference between a one-month and a two-month deposit is 1,500 dollars of your money sitting tied up rather than available to you. Over the course of several rentals across your 20s and 30s, the cumulative deposit cost of a low credit score can run into thousands of dollars. Beyond deposits, a low score may also limit which apartments you can qualify for, pushing you toward less competitive housing in less desirable locations. The real cost of poor credit on housing is not just financial. It affects where you can live. Buying a home This is where the credit score impact is most dramatic in absolute dollar terms. Mortgage interest rates vary significantly by credit score tier, and on a large, long-term loan those rate differences translate into tens of thousands of dollars. On a 350,000 dollar 30-year mortgage, the difference between a 680 credit score and a 760 credit score can be approximately 0.75 to 1.25 percentage points in interest rate. At a 1 percentage point difference, that translates to roughly 200 dollars more per month in mortgage payments and approximately 72,000 dollars more in total interest paid over the life of the loan. That is not a small number. It is the cost of a car, a significant portion of a college education, or years of retirement savings. All determined by a three-digit number. Buying a car Auto loan interest rates vary significantly by credit score. According to Experian’s State of the Automotive Finance Market report, borrowers with excellent credit scores in the 781 to 850 range received average new car loan rates of around 5% in recent years. Borrowers in the subprime range of 501 to 600 paid average rates above 14%. On a 30,000 dollar 60-month auto loan, the difference between 5% and 14% interest is approximately 150 dollars per month and roughly 9,000 dollars in total interest paid over the life of the loan. That is an amount that would easily cover the cost of a significantly better vehicle if your credit score had been higher. People with very poor credit may also be pushed toward buy-here-pay-here dealerships with even higher rates and less favorable terms, compounding the cost further. Car insurance This one surprises most people. In most US states, auto insurers use credit-based insurance scores to help determine your premium. These scores are similar but not identical to credit scores and they reflect the statistical correlation between credit behavior and insurance claim frequency. The impact is significant. According to a study by the Consumer Federation of America, drivers with poor credit can pay 50 to 100% more for auto insurance than drivers with excellent credit for the same coverage. On a 1,500 dollar annual premium, that is an additional 750 to 1,500 dollars per year, or 60 to 125 dollars per month, purely because of credit score. Three states, California, Hawaii, and Massachusetts, ban the use of credit in auto insurance pricing. In all other states, your credit score is a factor in what you pay to drive. Home insurance Home insurance premiums are also affected by credit-based insurance scores in most states. The same principle applies: insurers use credit data as a predictor of claim likelihood. Poor credit can result in meaningfully higher home insurance premiums, adding to the ongoing cost of homeownership for people who are already paying more on their mortgage because of a lower score. Personal loans Personal loans are used for everything from medical expenses to home improvements to consolidating debt. The interest rate on a personal loan is heavily determined by your credit score. Rates for borrowers with excellent credit can be as low as 6 to 8%. Borrowers with poor credit may face rates of 25 to 36% or higher, if they can get approved at all. On a 10,000 dollar personal loan over three years, the difference between 8% and 25% interest is approximately 2,500 dollars in additional interest. For someone using a personal loan to cover a medical emergency or essential repair, that difference is felt immediately and significantly. Credit cards Credit card interest rates, known as APR, vary dramatically based on creditworthiness. Premium rewards cards with the best benefits are generally only available to people with good or excellent credit. Borrowers with fair or poor credit are often limited to cards with higher rates, lower limits, and annual fees. For people who carry a balance, the interest rate difference compounds quickly. A 3,000 dollar balance at 16% APR costs about 480 dollars per year in interest. The same balance at 28% costs about 840 dollars per year. That 360 dollar annual difference is real money that goes directly to the card issuer rather than toward the balance. Employment Some employers, particularly those in financial services, government, and positions requiring security clearances, run credit checks as part of the background screening process. Poor credit does not automatically disqualify a candidate in most cases, but it can raise questions and in some industries it can affect hiring decisions. Employers must obtain your permission before running a credit check and in some states credit checks for employment

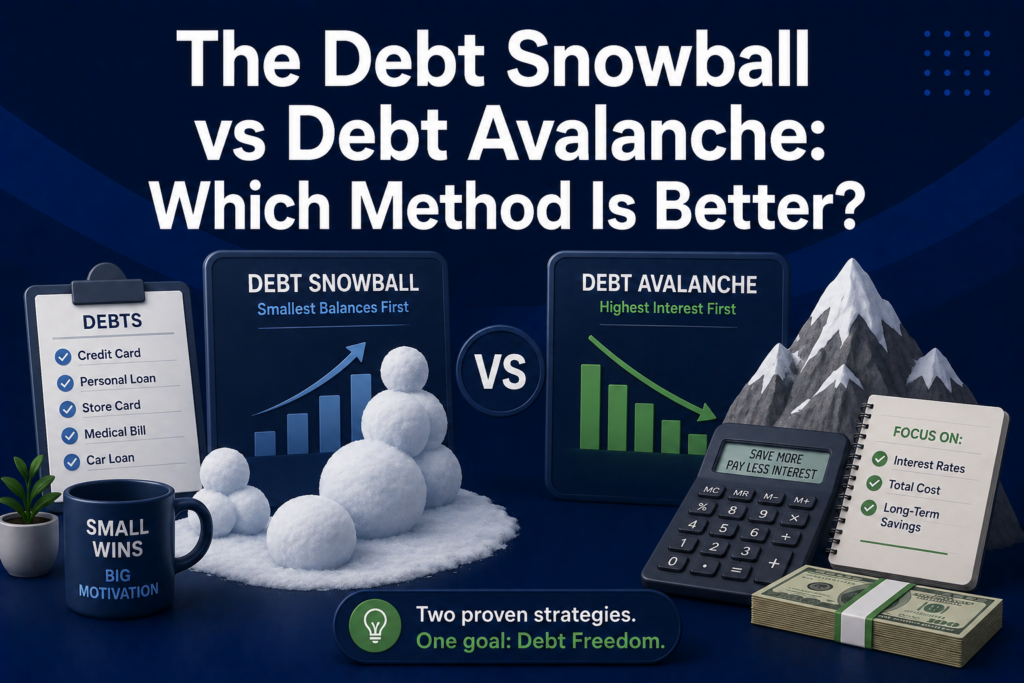

The Debt Snowball vs Debt Avalanche: Which Method Is Better?

If you are trying to pay off multiple debts, two methods come up more than any others: the debt snowball and the debt avalanche. Both work. Both have legitimate advantages. The debate between them has been going on for years and the honest answer is that the better one depends on who you are, not just what the math says. Here is a clear breakdown of how each method works, what the research says, and how to decide which one is right for your situation. How the debt snowball works The debt snowball method, popularized by personal finance commentator Dave Ramsey, works by paying off your smallest debt first regardless of interest rate. You make minimum payments on all your debts and put every extra dollar toward the smallest balance. When that debt is gone, you roll that payment amount onto the next smallest balance, and so on. The name comes from the momentum that builds as you eliminate accounts. Each payoff frees up more cash to attack the next debt, and the payments compound like a rolling snowball gaining size. Example: You have three debts. A 500 dollar medical bill, a 3,000 dollar credit card, and an 8,000 dollar car loan. Under the snowball method, you attack the 500 dollar bill first regardless of what interest rate any of them carry. How the debt avalanche works The debt avalanche method focuses on interest rates rather than balances. You make minimum payments on all your debts and put every extra dollar toward the debt with the highest interest rate. When that debt is paid off, you roll the payment to the next highest rate. The logic is straightforward: high-interest debt costs more money over time. Eliminating it first reduces the total interest you pay across all your debts. Example: Using the same three debts. If the 3,000 dollar credit card carries 24% interest, the 500 dollar medical bill carries 0%, and the car loan carries 7%, the avalanche method attacks the credit card first regardless of its balance being larger than the medical bill. What the math says The debt avalanche wins on math. Period. If you pay the same amount every month toward your debts, the avalanche method will cost you less money in total interest and get you debt-free faster in most scenarios. The higher the interest rates on your debts, the bigger the mathematical advantage of the avalanche. The difference can be significant. Depending on your debt mix and interest rates, the avalanche method can save hundreds or even thousands of dollars in interest compared to the snowball. What the research says about behavior Here is where it gets interesting. A study published in the Journal of Marketing Research found that people who focused on paying off individual accounts entirely, which aligns with the snowball approach, were more likely to eliminate their overall debt than those who spread payments based on balances or rates. The reason is psychological. Paying off a debt completely produces a sense of accomplishment that motivates continued effort. Mathematically optimal strategies do not help you if you abandon them three months in because the progress feels invisible. If you have tried to pay off debt before and given up, the snowball method’s quick wins may be more valuable to your long-term outcome than the avalanche’s mathematical efficiency. How each method affects your credit score Both methods improve your credit score over time by reducing your total debt. But they affect your score differently in the short term. Debt snowball and credit score: Paying off small balances quickly eliminates accounts, which can slightly affect your credit mix and account age. However, eliminating small balances also reduces overall utilization. If those small debts are revolving accounts like credit cards, paying them off reduces your utilization ratio and can produce noticeable score improvement quickly. Paying down high-interest revolving debt reduces utilization on those accounts, which can improve your score faster in many cases. If your highest-rate debt is a credit card with a high balance relative to its limit, the avalanche method can produce meaningful score improvement earlier than the snowball in some scenarios. For people who are building credit alongside paying off debt, the general principle is to prioritize paying down revolving credit card balances over installment debts when possible, since utilization is the second biggest factor in your credit score. Which method should you choose? Choose the debt snowball if: you have struggled to stay motivated with debt payoff in the past, you have several small debts that are making the situation feel overwhelming, you need quick wins to build momentum, or the interest rate differences between your debts are relatively small. Choose the debt avalanche if: you are highly motivated and confident you will stick with the plan regardless of early progress, you have significant high-interest debt where the math advantage is substantial, or you are focused on minimizing total interest paid over time. Consider a hybrid approach if: you have one or two very small debts you can eliminate quickly for a psychological win, then switch to the avalanche method for the remaining balances. This captures some motivational benefit of the snowball while shifting to the mathematically superior approach once momentum is established. What both methods have in common Regardless of which method you choose, the same fundamentals apply. Make minimum payments on all accounts every single month without exception. A missed payment damages your credit score far more than any debt payoff method can help it. Set up autopay on minimums so this never happens accidentally. And while you are paying off debt, continue building positive credit history where possible. If you are renting and your payments are not being reported to the credit bureaus, adding rent reporting through Credit Genius runs in parallel with your debt payoff without requiring any additional money. It adds positive data to your Experian file while you work through your debt, so your credit profile is stronger on the other side. The bottom line The