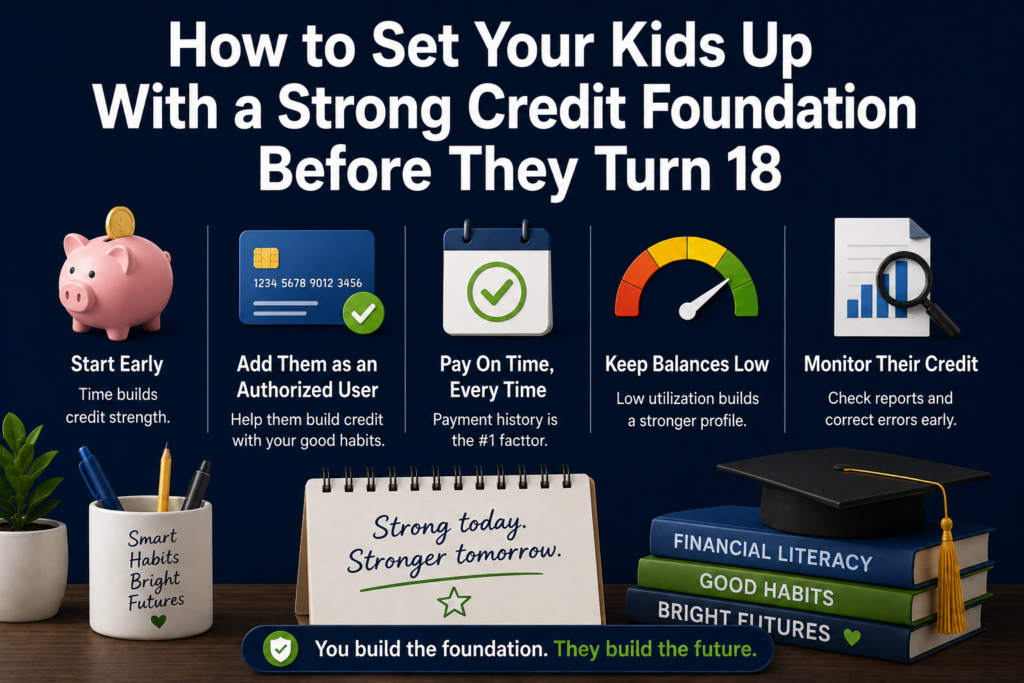

How to Set Your Kids Up With a Strong Credit Foundation Before They Turn 18

Most Americans turn 18 with no credit history whatsoever. They enter adulthood invisible to the credit system, which means their first apartment application, first car loan, and first major financial decision are all made at a disadvantage. It does not have to work that way. Parents who understand how credit works can give their children a meaningful head start by taking a few deliberate steps before their kids reach adulthood. Here is what you can do and when. Why starting before 18 matters Credit scoring rewards length of history. The longer a positive account has been open, the more value it adds to a credit profile. A child added as an authorized user on a parent’s credit card at age 13 has five years of established credit history by the time they turn 18. A young adult who opens their first account at 18 starts from zero. That five-year difference in account age matters when an 18-year-old applies for their first apartment or a 21-year-old applies for a car loan. The person with five years of established history in good standing is in a fundamentally different position than the person with six months. Add your child as an authorized user This is the most powerful credit-building tool available to parents for their children. When you add a child as an authorized user on your credit card, your payment history and account age on that card can appear on their credit report. You do not need to give your child the physical card or allow them to use it. The credit benefit comes from the account appearing on their report, not from their usage. Many parents add a child as an authorized user, keep the card, and never let the child use it. The child still receives the credit history benefit. The account you choose matters. Add your child to an account with a long history, a clean payment record, and low utilization. If your oldest card has a few late payments on it, consider whether a newer card with a cleaner record might be the better choice to put on your child’s report. Different card issuers have different policies on authorized user age minimums. Some allow authorized users as young as 13. Others require 15 or 16. Check your card issuer’s policy before adding your child. Freeze your child’s credit file Children’s credit files are attractive targets for identity thieves because the fraud often goes undetected for years. A child whose Social Security Number is used to open fraudulent accounts may not discover the damage until they apply for their first credit card at 18 or their first apartment at 21. Parents can place a credit freeze on their child’s file at all three bureaus. This prevents any new accounts from being opened in the child’s name. The freeze costs nothing and can be lifted when the child is ready to start using their credit. The process requires submitting documentation proving your identity and your relationship to the child, including a birth certificate and your own ID. It takes a bit more effort than freezing an adult file but the protection is significant. Teach the fundamentals before they need them A credit foundation is most valuable when paired with understanding. A teenager who becomes an authorized user on your card but does not understand what credit is, how scores work, or why payment history matters is less equipped to manage credit independently than one who understands the system. Walk your child through how credit scores are calculated. Explain what payment history is and why missing a payment is such a significant event. Show them what a credit report looks like. Explain what utilization means and why carrying high balances hurts your score even if you eventually pay them off. Financial education tools like the Credit Games feature inside Credit Genius can make this more engaging for teenagers who find the subject dry when explained as a lecture. Gamified financial education builds knowledge retention in a way that passive content consumption typically does not. When your child turns 16 to 18: prepare for independence In the two years before your child turns 18, start preparing them to manage credit independently. Pull their credit report to see what is on it, confirm the authorized user account is reporting correctly, and check for any unexpected entries. If you want your teenager to have their own credit account before 18, some credit card issuers offer student cards to 17-year-olds with a parent co-signer. A secured card with a small deposit is another option for older teenagers who are demonstrating financial responsibility. Have a direct conversation about the plan for when they turn 18. Will they keep the authorized user account? Will you remove them? Will they open their own card? Knowing the plan in advance prevents the scenario where a newly independent adult is suddenly starting from scratch with their credit because the authorized user account was closed. What not to do Do not add your child to an account with a poor payment history or high utilization. The negative information transfers along with the positive. A card with a few missed payments in its history can hurt your child’s credit file rather than help it. Do not give a teenager unrestricted access to a credit card before they understand how it works. The goal is to build a credit foundation, not to create an opportunity for spending that damages the very file you are trying to build. Do not neglect the freeze. A child’s Social Security Number is a valuable identity theft target. Placing a freeze on their credit file is one of the most protective actions a parent can take. The bottom line The credit foundation you build for your child before they turn 18 is one of the most practical financial gifts you can give them. Adding them as an authorized user on a well-managed account, freezing their credit file to protect against identity theft, and teaching them how credit

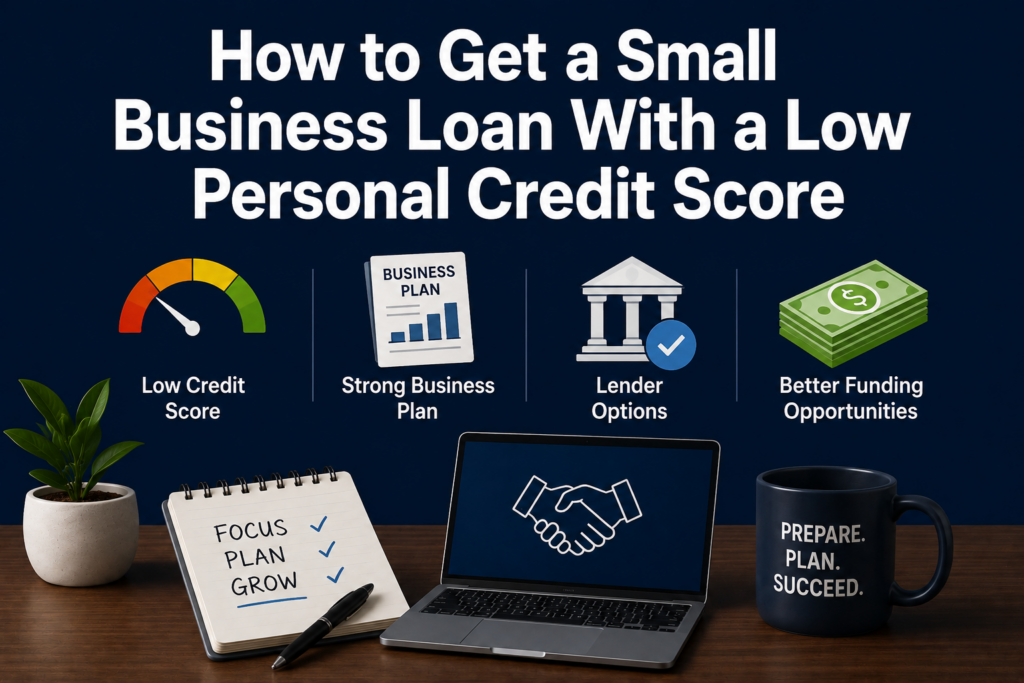

How to Get a Small Business Loan With a Low Personal Credit Score

Starting or growing a business with a low personal credit score is genuinely harder than doing it with good credit. Most small business lenders, particularly traditional banks, rely heavily on the owner’s personal credit score when evaluating a loan application, especially for newer businesses that do not yet have an established business credit profile. But low personal credit does not make small business financing impossible. It changes which options are available, what they cost, and what documentation you need to make a compelling case. Here is a practical guide to navigating small business lending with a low personal credit score. Why personal credit matters for business loans Most small business lenders, particularly banks and SBA-backed lenders, check the owner’s personal credit score as part of the application process. For businesses with less than two to three years of operating history, the owner’s personal credit is often the primary indicator of financial reliability because the business itself does not have a long enough track record to evaluate independently. Traditional bank loans and SBA 7a loans typically require a personal credit score of 680 or above. Some lenders set the bar at 700 or higher. Below those thresholds, the application becomes significantly harder and the available options shift toward alternative lenders who accept lower scores but charge higher rates. Know your minimum score requirements by loan type The SBA does not set a minimum credit score requirement but most SBA-approved lenders require at least 650 to 680. The SBA microloan program, which offers loans up to 50,000 dollars through nonprofit intermediary lenders, generally has more flexible credit requirements and is worth exploring for smaller funding needs. Online business lenders: Alternative online lenders like Kabbage, OnDeck, and Fundbox have lower minimum credit score requirements, sometimes accepting scores as low as 500 to 550. The tradeoff is significantly higher interest rates and shorter repayment terms. These are viable for short-term needs but expensive for long-term financing. Nonprofit lenders and Community Development Financial Institutions, known as CDFIs, offer microloans specifically designed for underserved business owners including those with limited or poor credit history. Accion Opportunity Fund, Kiva US, and local CDFI networks are worth researching. These lenders often look at the full picture of your business rather than relying primarily on credit score. Equipment financing: If you need funding specifically to purchase equipment, equipment financing uses the equipment itself as collateral, which reduces the lender’s reliance on your personal credit score. Approval requirements can be more flexible than for unsecured business loans. If your business has outstanding invoices from clients, invoice financing allows you to borrow against those receivables. The creditworthiness of your clients matters more than your personal score in many of these arrangements. Strengthen your application beyond the credit score A low personal credit score makes the application harder. A strong application in every other dimension can partially offset that disadvantage. Business revenue and cash flow. Strong business bank statements showing consistent revenue and healthy cash flow are compelling evidence of creditworthiness that your personal score cannot provide. Many alternative lenders weight revenue-based metrics heavily alongside or even above personal credit. Time in business. The longer your business has been operating successfully, the more evidence you have of its viability. Even two years of solid operating history can significantly improve your chances with many lenders. Collateral. Offering collateral, whether business assets, equipment, or in some cases personal assets, reduces the lender’s risk and can overcome credit score concerns. Secured loans are generally more accessible than unsecured ones for borrowers with lower scores. For newer businesses with limited revenue history, a detailed, credible business plan that demonstrates market understanding, realistic financial projections, and a clear repayment strategy can make a meaningful difference, particularly with CDFI and microloan lenders who evaluate applications more holistically. Build business credit separately Business credit, tracked by Dun and Bradstreet, Experian Business, and Equifax Business, is separate from personal credit. Building a business credit profile reduces your reliance on personal credit for future financing. Start by incorporating your business or forming an LLC, opening a dedicated business bank account, and getting an EIN from the IRS. Then open trade credit accounts with suppliers who report to business credit bureaus. Net-30 accounts with vendors who report payment history are a common starting point. A business credit profile with even six to twelve months of positive payment history makes future lending conversations significantly easier and reduces the weight placed on your personal score. Work on your personal credit in parallel If your personal credit score is genuinely a barrier to the financing you need, improving it should be a parallel priority alongside running your business. The most impactful short-term actions are paying down credit card balances to reduce utilization, disputing any errors on your credit report, and ensuring all payments are made on time going forward. If you are renting your home or business space, rent reporting through Credit Genius adds positive payment history to your Experian file without requiring any new debt or significant time investment. Every point gained on your personal score opens more business financing options at better rates. The bottom line A low personal credit score narrows your small business lending options and increases your cost of capital. It does not eliminate your options entirely. Alternative lenders, microloans, CDFIs, equipment financing, and invoice financing all offer paths to business capital with lower credit requirements.The best strategy combines pursuing the financing options available to you now with actively improving your personal credit and building a business credit profile in parallel. Better credit means better options and lower costs for every future financing need your business has.

How to Prepare Your Credit Before Having a Baby

Having a baby changes almost everything about your financial life. Costs go up, income may temporarily go down during parental leave, and the financial decisions you make in the months before and after birth carry more weight than they ever have before. Your credit score sits in the middle of all of it, affecting your housing options, your borrowing costs, and your financial flexibility during one of the most expensive transitions of your life. Here is how to use the months before your baby arrives to get your credit in the strongest position possible. Why credit matters more than usual before a baby The timing of parenthood often coincides with other major financial decisions. Many people buy a home, upgrade to a larger apartment, or take out a personal loan for home improvements or baby expenses in the period around a new child. Each of these decisions is heavily influenced by your credit score. Parental leave adds another layer. If one parent takes unpaid or partially paid leave, the household income drops while expenses rise. A financial buffer and a strong credit profile together provide the flexibility to handle that period without making panic decisions that damage your long-term financial health. Starting this process at least six to twelve months before your due date gives your credit improvements time to show up in your score before the decisions that depend on it arrive. Pull and review all three credit reports Start by pulling your full credit reports from annualcreditreport.com and reviewing each one carefully. Look for errors in payment history, accounts you do not recognize, outdated negative marks, and anything that should have fallen off your report but has not. One in five Americans has at least one error on their credit report. An error that goes unnoticed until you are trying to qualify for a mortgage or a personal loan in the middle of a new baby’s arrival is a problem you do not need at that moment. Find it now, dispute it now, and let it be resolved before the stakes are higher. Pay down credit card balances Credit utilization is the second most important factor in your credit score at 30% of the total. If you are carrying significant balances on credit cards, paying them down before your baby arrives does two things simultaneously: it improves your credit score and it frees up your credit line for genuine emergencies during a period when unexpected expenses are almost guaranteed. The goal is to get utilization below 30% on each card and ideally below 10%. This can produce a noticeable score improvement within one to two billing cycles of paying down balances. If you are planning to apply for a mortgage or a larger apartment before the baby comes, paying down utilization should be your first credit priority. Set up autopay on everything New parents are busy people. Sleep deprivation is real and so is the cognitive load of managing a newborn alongside every other responsibility. This is exactly the wrong environment for manually tracking payment due dates across multiple accounts. Set up autopay for the minimum payment on every account before your baby arrives. You can always pay more manually. But autopay ensures you never miss a payment simply because you forgot in the fog of a newborn’s first months. A missed payment costs 50 to 100 points and stays on your report for seven years. That is a problem you can completely prevent with ten minutes of setup today. Do not open new credit accounts in the months before major applications If you are planning to apply for a mortgage, a larger apartment, or a personal loan in the six to twelve months before or after your baby arrives, stop opening new credit accounts now. New accounts lower your average account age and add hard inquiries, both of which temporarily reduce your score. The temptation to open a new store card for baby purchases or take advantage of a promotional financing offer on a crib or stroller is real. Resist it. The discount is not worth the credit impact at a moment when your score matters for larger decisions. Build a credit buffer before income drops If you or your partner plan to take parental leave that reduces household income, the months before the baby arrives are the time to pay down as much revolving debt as possible. High utilization during a period of reduced income is harder to manage and easier to slip into. Going into parental leave with low balances on your credit cards gives you a buffer. If an unexpected expense arises during leave, you have available credit to use without immediately pushing utilization into score-damaging territory. Think of low credit utilization as financial headroom for an unpredictable period. Make sure your rent is being reported If you are renting and your payments are not being reported to the credit bureaus, you are missing an opportunity to add positive payment history to your file at a time when every point matters. Credit Genius reports rent to Experian with backdating of up to 24 months, meaning you do not have to start from zero. Adding verified rent payment history to your credit file in the months before a major housing application can meaningfully improve your score and strengthen your overall credit profile at exactly the right moment. Understand your parental leave rights and plan financially This is not strictly a credit tip but it directly affects your credit outcomes. Know what your employer provides for parental leave, what state benefits you may be entitled to, and what the income gap will be during leave. Understanding the numbers in advance allows you to plan for them rather than react to them. A household that enters parental leave with a clear budget for the leave period, low credit card balances, autopay set up on all accounts, and a small emergency fund is in a fundamentally different position than one that enters it unprepared. The credit implications

10 Signs You Are Ready to Apply for a Mortgage

Buying a home is one of the biggest financial decisions most people make and one of the most common mistakes is applying for a mortgage before you are actually ready. A rejected application damages your credit through hard inquiries and can lock you out of favorable rates for months. Knowing when you are genuinely prepared makes the difference between a smooth process and a frustrating one. Here are ten signs that you are ready to apply. 1. Your credit score is at least 620 and ideally 740 or above Most conventional lenders require a minimum score of 620. FHA loans can go as low as 580 with a 3.5% down payment. But meeting the minimum is not the same as being in the best position. A score of 740 or above typically qualifies you for the best available rates. On a 350,000 dollar 30-year mortgage, the difference between a 680 score and a 760 score can translate to more than 50,000 dollars in total interest paid over the life of the loan. If your score is between 620 and 700, it is worth asking whether six to twelve more months of credit building would meaningfully change your rate before you apply. Tools like Credit Genius can help you identify the specific actions that will move your Experian score most efficiently in the months leading up to an application. 2. You have at least two years of steady income history Lenders want to see stable, documented income. Most require two years of employment history in the same field, verified through W-2s, tax returns, and pay stubs. Self-employed borrowers need two years of tax returns showing consistent income. A recent job change is not automatically disqualifying, particularly if you moved into the same field at a higher salary. But gaps in employment or a recent career pivot into a new industry can complicate the application. If your income history is not clean and consistent, it is worth understanding how your specific situation will be evaluated before you apply. 3. Your debt-to-income ratio is below 43% Your debt-to-income ratio, or DTI, is the percentage of your gross monthly income that goes toward debt payments. Most conventional lenders cap DTI at 43% for approval, with better rates available at lower ratios. Some loan programs allow up to 50% but with stricter requirements elsewhere. Calculate your DTI by adding up all your monthly debt payments, including the projected mortgage payment, and dividing by your gross monthly income. If the number is above 43%, paying down existing debt before applying will improve both your approval odds and your rate. 4. You have a down payment ready The size of your down payment affects your loan options, your rate, and your monthly payment. Conventional loans require as little as 3% down but anything below 20% typically requires private mortgage insurance, or PMI, which adds to your monthly cost. FHA loans require 3.5% with a score of 580 or above. VA loans for eligible veterans require no down payment. USDA loans for qualifying rural properties also have no down payment requirement. Beyond the down payment itself, lenders also want to see reserves, meaning money left over after closing that covers several months of mortgage payments. Having the down payment ready is a prerequisite. Having reserves on top of it signals to lenders that you will not be stretched thin immediately after closing. 5. Your credit report is clean and accurate Pull all three of your credit reports from annualcreditreport.com before applying and review them carefully. One in five Americans has at least one error on their credit report. An error that goes unnoticed until a lender pulls your credit can derail an application or cost you a better rate. Look for accounts you do not recognize, late payments recorded incorrectly, collections that should have fallen off, and any public records that are outdated or inaccurate. Dispute anything that is wrong at least 60 to 90 days before you plan to apply so there is time for the correction to be processed and reflected in your score. 6. You have not opened any new credit accounts in the past six months New credit accounts lower your average account age and add hard inquiries to your file. Both have a negative impact on your score, even if small. In the six to twelve months before a mortgage application, stop opening new credit accounts entirely. This includes store credit cards opened for a discount, new auto loans, and any other credit products. Lenders also look at recent credit activity as a signal of financial stability. A flurry of new accounts shortly before a mortgage application can raise questions. 7. You have been at your current address for at least a year Residential stability is a signal lenders look at as part of the overall application picture. Frequent moves in the years before an application are not disqualifying but they can prompt additional questions. Having a stable address history alongside stable employment and stable credit is the profile that produces the smoothest mortgage applications. 8. You understand the full cost of homeownership Being financially ready for a mortgage means being ready for more than the monthly payment. Property taxes, homeowners insurance, HOA fees if applicable, maintenance costs, and repair reserves all add to the real cost of ownership. A common rule of thumb is to budget 1% of the home’s value per year for maintenance and repairs. On a 350,000 dollar home that is 3,500 dollars per year or roughly 290 dollars per month on top of your mortgage payment, taxes, and insurance. If your budget only works if nothing goes wrong, you are not ready. 9. You have been pre-approved, not just pre-qualified Pre-qualification is an informal estimate based on self-reported information. Pre-approval involves a lender actually reviewing your income documentation, credit report, and assets to confirm how much they are willing to lend. In competitive markets, sellers increasingly require pre-approval letters before considering offers. Getting pre-approved before you start

What Credit Score Do You Need to Buy a House in 2026?

Buying a home is the largest financial decision most people make in their lifetime and your credit score is one of the most important factors in determining whether you can do it and at what cost. The minimum score you need depends on the type of loan you are applying for, and the score that gets you the best rate is higher than most people expect. Here is a clear breakdown of what credit score you actually need in 2026 and what the difference between a good and a great score means for your mortgage. Minimum credit scores by loan type Conventional loans: 620 minimum. Conventional loans, which are not backed by a government agency, typically require a minimum credit score of 620. However, a score at or near the minimum will result in higher interest rates and stricter requirements around down payment and debt-to-income ratio. FHA loans: 580 minimum with 3.5% down, 500 with 10% down. FHA loans are insured by the Federal Housing Administration and are designed for borrowers with lower credit scores or smaller down payments. A score of 580 qualifies you for a 3.5% down payment. Scores between 500 and 579 require a 10% down payment. Below 500, FHA financing is generally not available. VA loans: No official minimum, but lenders typically require 580 to 620. VA loans for eligible veterans, active-duty service members, and surviving spouses do not have a government-set minimum credit score. Individual lenders set their own requirements, which typically fall between 580 and 620. USDA loans: 640 recommended. USDA loans for rural and suburban home purchases have no official minimum but most lenders require at least 640 for automated approval. Below that, manual underwriting may be required. Jumbo loans, which exceed conforming loan limits, have stricter requirements. Most lenders require a minimum score of 700 to 720 and some set the bar even higher. What the score means for your interest rate Meeting the minimum score is only part of the equation. The rate you are offered depends heavily on where your score falls within lender tiers. The difference between a 640 score and a 760 score can translate to a difference of 1% or more in your mortgage rate. On a 350,000 dollar 30-year mortgage, a 1% difference in interest rate translates to approximately 200 dollars per month in payment difference and over 70,000 dollars in total interest paid over the life of the loan. The credit score you bring to a mortgage application is not just a qualification hurdle. It is a financial variable with real, lasting dollar consequences. General rate tier thresholds used by most conventional lenders in 2026 fall roughly as follows. Scores below 640 receive the least favorable rates. Scores from 640 to 679 are considered subprime by most conventional lenders. Scores from 680 to 719 are in the standard range. Scores from 720 to 759 qualify for better rates. Scores of 760 and above typically receive the best available rates. Which credit score do mortgage lenders use? Mortgage lenders do not use the VantageScore shown on most free credit monitoring apps. They pull specific FICO score versions from all three bureaus: FICO Score 2 from Experian, FICO Score 4 from TransUnion, and FICO Score 5 from Equifax. For most mortgage applications, they use the middle of the three scores. For joint applications with a co-borrower, lenders typically use the lower of the two middle scores. This means that if one borrower has a 740 and the other has a 660, the application is evaluated at 660. This is why knowing your actual FICO mortgage scores, not just your VantageScore from a monitoring app, is important when preparing to apply. The number on your app and the number your lender sees may be meaningfully different. How far in advance should you work on your credit? Ideally, at least 12 months before you plan to apply. This gives you time to dispute errors, reduce utilization, build additional payment history, and let any improvements work their way through the scoring system. If you are within six months of applying, the most impactful actions are paying down credit card balances to reduce utilization, ensuring there are no errors on your credit report, and avoiding any new credit applications that would add hard inquiries. For renters who are planning to buy in the next one to three years, rent reporting through Credit Genius is one of the most effective preparatory steps available. Adding verified rent payment history to your Experian file, including backdated history, can meaningfully improve your score over the months leading up to a mortgage application. What to do if your score is not there yet If your score is below where you need it to be, a realistic improvement timeline depends on what is holding it down. High utilization can be addressed in one to two billing cycles by paying down balances. Errors can be corrected within 30 days through the dispute process. Building additional payment history takes longer but compounds steadily over months. Most people who are 20 to 40 points below their target can reach it within six to twelve months of consistent, focused effort. A 50 to 80 point gap typically takes twelve to twenty-four months. Gaps above 100 points often require a longer timeline depending on what is causing them. Using a tool like Credit Genius that analyzes your specific credit profile and tells you exactly which actions will move your score most efficiently can significantly shorten this timeline by helping you focus on the highest-impact actions rather than applying generic advice. The bottom line The minimum credit score to buy a house in 2026 is 500 for FHA loans with a large down payment and 620 for conventional financing. But the score that gets you the best rate and the lowest total cost of borrowing is 760 or above.If homeownership is a goal, treat your credit score as a financial variable worth actively managing in the years leading up to your purchase.

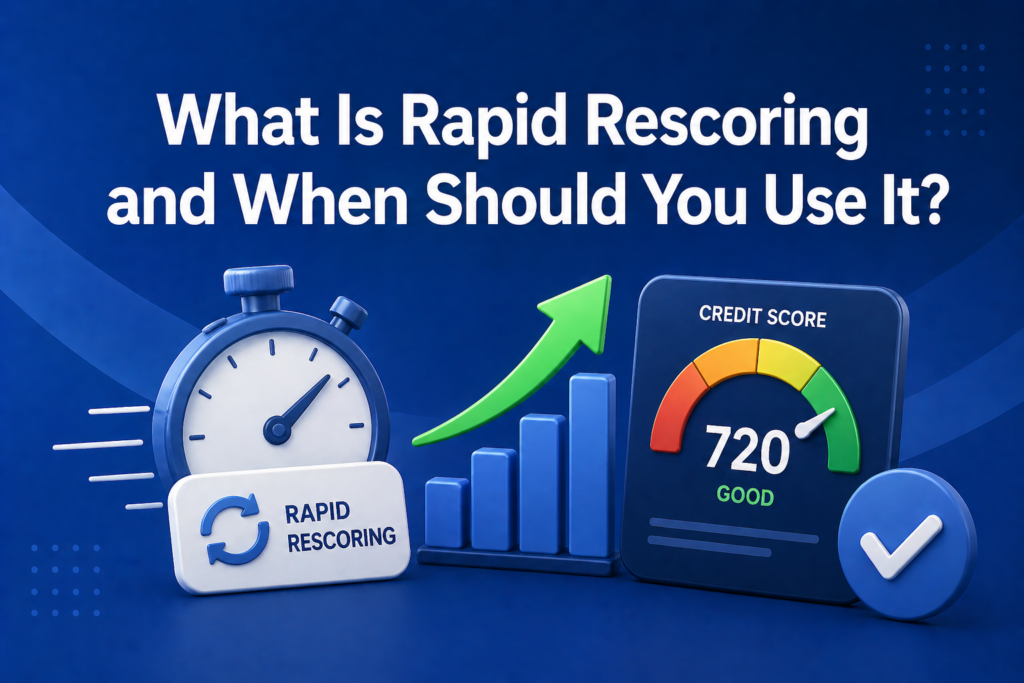

What Is Rapid Rescoring and When Should You Use It?

Rapid rescoring is one of the lesser-known credit tools available to borrowers, and it can make a significant difference in specific situations. Most people have never heard of it. Those who have often do not know exactly how it works or when it is actually worth using. Here is a clear explanation of what rapid rescoring is, how the process works, and the situations where it genuinely makes sense. What rapid rescoring actually is Rapid rescoring is a process where a lender, typically a mortgage lender, works with a credit bureau to update your credit file quickly and generate a new credit score that reflects recent changes. Under normal circumstances, changes to your credit file such as paying down a balance or correcting an error can take 30 to 45 days to be reflected in your credit score. Rapid rescoring compresses that timeline to as little as three to five business days. The key point is that rapid rescoring is not something you can request directly. It must be initiated by a lender on your behalf. It is also not free, though the cost is typically absorbed by the lender rather than charged to the borrower. How the process works When a lender initiates rapid rescoring, they submit documentation of recent changes to your credit file directly to the credit bureau. This might include proof that you paid down a credit card balance, documentation that an error has been corrected by the creditor, or evidence that a collection account has been settled. The bureau processes the updated information and generates a new credit score that reflects the changes. The lender then uses this updated score for your application rather than the score from the original pull. Rapid rescoring only updates the information that is submitted with documentation. It cannot add positive information that does not exist or remove accurate negative information. It is a tool for making sure your file reflects changes that have already happened, not a way to manufacture a better score. When rapid rescoring makes sense You are close to a score threshold for a better rate. This is the most common use case. If your score is 717 and a score of 720 or above would qualify you for a significantly lower mortgage rate, and you have recently paid down a balance or had an error corrected that would push you over that threshold, rapid rescoring lets you capture that improvement before closing rather than waiting for it to appear naturally. An error was recently corrected. If you discovered an error on your credit report, disputed it successfully, and had it removed or corrected, rapid rescoring allows the corrected file to be reflected in your score immediately rather than waiting for the normal update cycle. You paid down a significant balance just before applying. If you paid off a credit card balance to reduce your utilization before a mortgage application, that payoff may not yet be reflected in the score the lender pulled. Rapid rescoring can capture the lower utilization and the improved score that comes with it. You are on a tight timeline. If you are closing on a home purchase or refinance within a matter of days and a score improvement would meaningfully affect your rate or approval, rapid rescoring is one of the few tools that can produce a result fast enough to matter. When rapid rescoring does not make sense Rapid rescoring is not useful if you have not actually made changes to your credit file. If you are hoping it will somehow improve a score without underlying changes to support the improvement, it will not. The process only reflects what has already happened. It is also not a substitute for longer-term credit building. If your score is significantly below the threshold you need, a few points from rapid rescoring will not bridge a large gap. It is most effective when you are already close and just need the score to catch up to the changes you have already made. How to ask for rapid rescoring If you think rapid rescoring might help your situation, raise it with your mortgage lender or loan officer. Ask whether they offer it and whether your situation qualifies. Come prepared with documentation of the changes that have been made to your credit file, whether that is a payoff confirmation, a letter from a creditor confirming an error correction, or a settlement receipt. Not all lenders offer rapid rescoring and those that do have their own processes for initiating it. Your loan officer is your starting point. The bottom line Rapid rescoring is a niche but genuinely useful tool for people in specific situations, primarily those who are close to a major loan application and have recently made changes to their credit file that have not yet been reflected in their score. It is not a magic fix and it is not available directly to consumers, but for the right situation it can make a meaningful difference in your rate or approval outcome. If you are actively working to build your credit ahead of a major financial decision, tools like Credit Genius that monitor your Experian file in real time and provide personalized guidance on what actions will move your score most efficiently can help you get to the score you need before rapid rescoring even becomes necessary.

The Credit Score Guide for People in Their 20s

Your 20s are the most consequential decade for credit. Not because the stakes are highest right now, they are not, but because the habits and history you build in your 20s compound over time in ways that make everything harder or easier in your 30s, 40s, and beyond. This guide covers everything you need to know about credit in your 20s: what your score should look like at different stages, what moves matter most, what mistakes are most common, and how to set yourself up for the decade ahead. What a normal credit score looks like in your 20s The average credit score for Americans aged 18 to 25 is in the low-to-mid 600s. For those aged 26 to 35 it rises to the mid-to-high 600s. These numbers reflect the reality that most people in their 20s are still building their credit file from scratch. If you are in your early 20s with a score in the 600s, that is not a problem. It is a starting point. If you are in your late 20s with a score below 620, it is worth understanding why and taking deliberate steps to improve it before the financial decisions that require strong credit become more pressing in your 30s. A score of 700 or above by the time you hit 30 is an achievable and valuable target. Here is how to get there. Early 20s: build the foundation The priority in your early 20s is getting a credit file established. Many people at 18 or 19 are credit invisible, meaning they have no credit history at all. The credit system cannot score you and lenders treat invisibility similarly to bad credit. Become an authorized user. Ask a parent or family member to add you to a long-standing account with good history. This is the fastest way to go from invisible to scoreable without opening any accounts yourself. Open your first account. A student credit card or secured card used for one small recurring purchase paid off every month is the cleanest credit-building tool available. Keep utilization low and never miss a payment. Report your rent. If you are renting an apartment or room, get that payment on your credit file. Credit Genius reports rent to Experian with backdating, meaning months of history you have already built can be added at once. For a 22-year-old with a thin file, this can be transformative. Mid 20s: build momentum and avoid common mistakes By your mid 20s you should have at least a year or two of credit history. This is when the most common and costly mistakes tend to happen. Do not miss payments. A missed payment in your mid 20s stays on your report until your early 30s. That is exactly when you are likely to apply for a car loan, a mortgage, or a rental in a competitive market. Set up autopay on everything. Do not max out your cards. High utilization is one of the fastest ways to tank a score that took years to build. Keep balances below 30% of your limit. Below 10% is better. Do not open accounts impulsively. Store cards, promotional financing, and sign-up bonus cards are tempting. Every application is a hard inquiry and every new account lowers your average account age. Be selective. Do not close old accounts. The length of your credit history matters. Closing old accounts shortens it and reduces your available credit. If a card has no annual fee, leave it open. Late 20s: optimize and prepare for the 30s Your late 20s are when credit starts to matter in more consequential ways. You may be looking at buying a home, taking out a car loan, starting a business, or applying for apartments in more competitive markets. The credit decisions you made in your early and mid 20s are showing up in your score now. Know your score and what is driving it. Pull your full credit report from all three bureaus and understand what is in it. Look for errors. Look for accounts you forgot about. Look for anything that should have fallen off but has not. Diversify your credit mix if you have not already. Having both revolving accounts like credit cards and installment accounts like a car loan, student loans, or a credit builder loan demonstrates to scoring models that you can manage different types of credit. Credit mix accounts for 10% of your FICO score. Do not open new accounts before major applications. If you are planning to apply for a mortgage in the next six to twelve months, stop opening new accounts now. New accounts lower your average account age and add hard inquiries at exactly the wrong time. Pay down high balances. If you have been carrying balances on credit cards, your late 20s are the time to get serious about paying them down. Lower utilization produces faster score improvement than almost anything else in the short term. The five factors and what they mean in your 20s Payment history (35%). The most important factor. A single missed payment can cost 50 to 100 points and stays on your report for seven years. Autopay is non-negotiable. Credit utilization (30%). Keep balances low relative to your limits. This is the fastest variable you can control directly. This is the factor that rewards starting early. Every year you build in your 20s is a year of history working for you in your 30s. Credit mix (10%). A mix of revolving and installment accounts is better than one type alone. Do not open accounts just for this reason, but be aware of it when you are considering new products. New credit (10%). Hard inquiries and new accounts have a small, temporary negative impact. Space out applications and avoid opening multiple accounts at once. Tools worth using in your 20s Monitoring your credit file regularly is not optional in your 20s. Errors happen, identity theft happens, and the only way to catch these things is to look at your report.

How to Build Credit as a Gig Worker or Freelancer

The credit system was designed around a paycheck. Consistent employment, a predictable income, and a W-2 at the end of the year. Gig workers and freelancers do not fit that mold. Irregular income, self-employment, and multiple income streams can make the credit landscape feel like it was built for someone else. It was. But that does not mean credit is out of reach. Here is how to build a strong credit profile when your income does not look the way the system expects. Why gig workers face unique credit challenges Your credit score itself is not affected by how you earn your income. Employment status and income do not appear on your credit report. The score is based purely on your credit behavior: payment history, utilization, account age, credit mix, and new inquiries. The challenge for gig workers and freelancers shows up in two places: getting approved for credit products in the first place, and proving income stability when applying for loans or apartments. Lenders want to see predictable income when they evaluate applications. Irregular or self-employed income is harder to document and often scrutinized more heavily. But once you are approved and the account is open, your credit score is built exactly the same way as anyone else’s: by paying on time and managing balances responsibly. Start with what you are already paying Most gig workers and freelancers are renting. That monthly rent payment is almost certainly your largest and most consistent financial obligation. If it is not being reported to the credit bureaus, you are missing one of the most accessible credit-building opportunities available to you. Credit Genius reports rent payments to Experian, including up to 24 months of prior history through backdating. For a freelancer with a thin credit file, adding a verified record of consistent rent payments can be one of the fastest ways to establish meaningful credit history without taking on any new debt. Build a documented income history Even though income does not appear on your credit report, it matters when you apply for new credit. Lenders evaluating a freelancer’s application want to see that your income is real, consistent, and documented. File your taxes consistently and on time, including Schedule C if you are self-employed. Keep organized records of your invoices and payments. A year or two of tax returns showing stable self-employment income is the most credible documentation you can provide. Bank statements showing regular deposits can supplement this. The stronger your income documentation, the more confidently you can apply for credit products that require income verification. Open a secured credit card A secured card is one of the most accessible credit products for someone with limited credit history or irregular income. Because you provide a cash deposit as collateral, approval requirements are generally lower and income documentation requirements are lighter. Use it for predictable small purchases, the kind you know you can pay off in full every month regardless of what your income looks like that month. Consistency is more important than volume. One small purchase paid off every month is better than large purchases that strain your cash flow in a slow month. Manage utilization carefully given income variability Variable income makes utilization management more complex. In a strong month you might be tempted to put larger expenses on a card. In a slow month, paying those balances off becomes harder. The safest approach is to keep credit card balances low regardless of your current income level. Treat your credit utilization target, ideally below 30% and better below 10% of your limit, as a fixed constraint rather than something you adjust based on how the month went. This protects your score from the volatility that naturally comes with self-employment. Consider a credit builder loan Credit builder loans are particularly well-suited to gig workers because the fixed monthly payment is small, predictable, and easy to budget for even in irregular income months. The payment goes into a savings account that you receive at the end of the term. The loan builds your payment history and your savings simultaneously. For a freelancer trying to demonstrate payment reliability to scoring models, a credit builder loan with twelve consecutive on-time payments is compelling evidence. Keep an emergency fund specifically for credit payments This is credit advice specific to gig workers that most general credit articles do not cover. Because your income is variable, your ability to make credit payments can fluctuate. A slow month that coincides with a large credit card balance is exactly the situation that produces missed payments. Maintaining a small dedicated reserve, even just enough to cover minimum payments on all accounts for two or three months, protects your payment history from the natural income variability of freelance work. Your credit score should not suffer because a client paid late. A reserve prevents that. Separate business and personal credit eventually As your freelance income grows, building a separate business credit profile becomes worthwhile. Business credit is built under your business’s EIN rather than your personal Social Security Number, and strong business credit can help you access financing for your business without it affecting your personal credit score. In the early stages of freelancing, focus on your personal credit first. Once your business is generating consistent revenue and you are thinking about business financing, tools, or equipment purchases, explore business credit as a parallel track. The bottom line Being a gig worker or freelancer does not prevent you from building excellent credit. It just means you need to be more intentional about it than someone with a predictable paycheck. Start with the payments you are already making, particularly rent. Add one accessible credit product and manage it conservatively. Document your income consistently. Protect your payment history with a small reserve. The credit system was not designed with you in mind, but it responds to the same behaviors regardless of how you earn your living.

7 Credit Moves to Make in Your 20s That Will Pay Off in Your 30s

Your 20s are when the credit habits you build have the most compounding value. The reason is simple: credit scoring rewards length of history, and every year you spend building a clean record in your 20s is a year of positive history that will still be working for you in your 30s when the stakes get higher. Here are seven specific credit moves that are worth making in your 20s and why each one pays dividends later. 1. Start building credit as early as possible Length of credit history accounts for 15% of your FICO score. Every year you delay starting is a year of history you can never get back. The person who opens their first credit account at 21 has four more years of history by 25 than the person who waits until 25 to start. That gap matters when you are trying to qualify for a mortgage in your early 30s. If you are renting, start with rent reporting. Credit Genius reports your rent payments to Experian and can backdate up to 24 months of prior history, giving you a head start on account history without requiring you to take on debt. If you want a credit account, a secured card used responsibly is the lowest-risk entry point. 2. Report your rent payments from day one Most people in their 20s are renting. Most of them are making that payment on time every month and getting absolutely no credit recognition for it. That is one of the biggest structural unfairnesses in the credit system and it is fixable. Signing up for rent reporting the moment you move into your first apartment means every on-time payment from that point forward is building your credit file. If you have been renting for a year or more and have not started yet, backdating lets you submit that prior history immediately. The sooner you start, the more history you accumulate before you need it for something important. 3. Never miss a payment Payment history is 35% of your FICO score. One missed payment in your 20s stays on your credit report for seven years, which means it could still be affecting your score when you apply for a mortgage in your early 30s. The stakes are higher than they seem. Set up autopay for the minimum on every account immediately. You can always pay more manually. But autopay ensures you never miss a payment simply because you forgot. This one habit, maintained consistently through your 20s, does more for your 30s credit score than almost anything else. 4. Keep utilization low even when you do not have to When you are in your 20s and money is tight, it is tempting to use your full credit limit as a financial buffer. Resist this where possible. High utilization hurts your score in real time, and the habit of running high balances is hard to break. Try to keep your credit card balances below 30% of your limit at all times, and below 10% when you are preparing for any significant credit application. A person who develops this habit in their 20s enters their 30s with a clean utilization record that reflects disciplined financial behavior, which is exactly what mortgage lenders are looking for. 5. Do not open accounts you do not need Retail store cards, promotional financing deals, and credit cards opened for a one-time discount are tempting in your 20s when every dollar feels significant. But each application is a hard inquiry and each new account lowers your average account age. Be intentional about every account you open. Ask whether you actually need it or whether you are just reacting to an offer. A smaller number of well-managed, long-standing accounts in your 30s is worth far more than a dozen accounts opened impulsively in your 20s. 6. Check your credit report regularly and dispute errors fast Errors on credit reports are common and they do not fix themselves. A Federal Trade Commission study found that one in five Americans has at least one error on their credit report. The earlier you catch an error, the less damage it does and the simpler the dispute process tends to be. Pull your reports from annualcreditreport.com at least once a year, or use a monitoring tool like Credit Genius that alerts you the moment anything changes on your Experian file. Getting into this habit in your 20s means you enter your 30s with a clean, accurate credit file rather than discovering a years-old error right before a major loan application. 7. Treat credit as infrastructure, not just a score The biggest mindset shift that pays off later is this: stop thinking about your credit score as a number and start thinking about your credit file as financial infrastructure. The score is an output. The file is what you are actually building. People who think about credit this way in their 20s make decisions differently. They keep old accounts open because account age is infrastructure. They pay on time every month because payment history is infrastructure. They monitor their file because knowing what is in it is infrastructure. By the time they reach their 30s, when credit matters most for mortgages, business loans, and major purchases, the infrastructure is already in place. The person who builds credit deliberately in their 20s does not have to scramble to fix it in their 30s. That is the whole point. The bottom line Your 20s are the highest-leverage decade for credit building because every year of positive history you accumulate now compounds in value for the rest of your financial life. The moves are not complicated: start early, report your rent, never miss a payment, keep utilization low, be selective about new accounts, monitor your file, and think long term. None of these require significant money or financial sophistication. They just require consistency. And consistency in your 20s is exactly what your 30s self will thank you for.

How Buy Now Pay Later Is Affecting Credit Scores in 2026

Buy Now Pay Later has gone from a niche checkout option to one of the most widely used payment methods in the United States. Tens of millions of Americans now use services like Affirm, Klarna, Afterpay, and Zip to split purchases into installments. What most of them do not know is that the credit implications of these products are changing fast, and in 2026 the rules are meaningfully different from what they were two years ago. Here is what you need to know about how Buy Now Pay Later is affecting credit scores right now. Buy Now Pay Later was mostly invisible to credit bureaus. That is changing. The majority of time in its history, there was no credit reporting for Buy Now Pay Later activities. If you got a dozen installment plans and paid each one back, your credit score will likely not budge. It worked similarly when you failed to make your payments. Credit reporting agencies simply didn’t receive this information. That is changing. Experian, TransUnion, and Equifax have all been developing frameworks for incorporating Buy Now Pay Later data into credit files. Several major providers have begun reporting to one or more bureaus, and the trend is accelerating. The result is that Buy Now Pay Later is becoming a two-edged instrument: used responsibly it can build credit, used carelessly it can damage it. How Buy Now Pay Later can hurt your credit score The risk side of Buy Now Pay Later on credit is more developed than the benefit side in 2026. Here is where it can cause damage. Missed payments. As more providers begin reporting to credit bureaus, missed or late Buy Now Pay Later payments are increasingly likely to show up as derogatory marks on your credit report. A missed payment on a 40 dollar installment plan can carry the same weight as a missed credit card payment. It gets reported as a delinquency and stays on your report for seven years. Hard inquiries. Some Buy Now Pay Later providers run a hard credit inquiry when you apply for a larger purchase plan. Hard inquiries have a small temporary negative impact on your score and remain on your credit report for two years. If you are applying for multiple Buy Now Pay Later plans in a short period, the cumulative effect of multiple hard inquiries can add up. Utilization complexity. As scoring models evolve to incorporate Buy Now Pay Later data, there is ongoing uncertainty about how outstanding installment balances will affect utilization calculations. Carrying multiple open Buy Now Pay Later plans simultaneously could affect how scoring models assess your debt load, though the specifics vary by model and are still being standardized across the industry. Overextension. The ease and accessibility of Buy Now Pay Later makes it particularly easy to take on more payment obligations than your budget comfortably supports. Missing one plan because you forgot about another is one of the most common ways Buy Now Pay Later users end up with unexpected derogatory marks. How Buy Now Pay Later can help your credit score The positive side is real but less consistent across providers and scoring models. Building payment history. For providers that report on-time payments to credit bureaus, Buy Now Pay Later can add positive payment history to your credit file. For someone with a thin file who is making small, consistent installment payments, this can be a legitimate credit-building tool. The key is confirming that your specific provider reports to bureaus and that they report positive payments, not just negative ones. Credit mix. Installment accounts contribute to credit mix, which accounts for 10% of a FICO score. If your file currently only has revolving accounts like credit cards, adding an installment account can marginally improve this factor. Does your Buy Now Pay Later provider report to credit bureaus? This is the most important question to answer before using any Buy Now Pay Later service in 2026. The answer varies significantly by provider and is changing as the industry evolves. Some providers report to all three bureaus. Some report only to one. Some report negative information only. And some do not report at all. It would be wise to check your provider’s current credit reporting policy (which is typically located in their terms of service or FAQs) before making use of a Buy Now Pay Later service for anything greater than an immediate, low dollar repayment obligation. The CFPB has been actively examining the Buy Now Pay Later industry and has indicated that further regulatory guidance on credit reporting requirements is likely. The landscape in late 2026 may look different from what it does early in the year. What this means for your credit strategy Treat Buy Now Pay Later like any other credit obligation. The informal, frictionless nature of these services can make them feel less serious than a credit card or loan, but that framing is increasingly inaccurate as bureaus incorporate more of this data. Track every active Buy Now Pay Later plan you have open. Set payment reminders. Do not assume that missing a small installment will not affect your credit just because the purchase was inexpensive. And if you are actively trying to build or improve your credit, prioritize credit-building tools that have well-established, consistent reporting relationships with the bureaus. Rent reporting through a service like Credit Genius, for example, has a clear and consistent reporting relationship with Experian. The payments you are submitting are verified and the credit impact is predictable. That is a different situation from the still-evolving and inconsistent world of Buy Now Pay Later credit reporting. The bottom line Buy Now Pay Later is no longer credit-neutral. As bureau reporting becomes more widespread across providers, the same payment discipline that matters for credit cards and loans is increasingly relevant for installment plans at checkout. Pay on time. Track what you owe. Know whether your provider reports to bureaus. And if you are actively building credit, do not rely on Buy Now Pay